Accenture Stock Analysis: AI-Driven Strength Meets Cautious Outlook

Accenture (NYSE: ACN), a global leader across the industry analyst community, has managed to sail through its fiscal 2025, ending in a strong fourth quarter that surpassed the company’s internal projections. The success of its early and concentrated investments in the field of Generative AI is clearly described in the financial statements released on September 25, 2025, a strategic move that is beginning to pay significant dividends and shape its future trajectory.

Financial Performance

For the fourth quarter, revenues reached $17.6 billion, up 7% year over year, while adjusted EPS climbed 9% to $3.03. Full-year revenues came in at $69.7 billion, a 7% increase, with adjusted EPS up 8% to $12.93. Free cash flow also strengthened, totaling $10.9 billion for the year.

The real story, however, lies in the company’s ability to capture demand in high-growth areas. Total new bookings for the year were a robust $80.6 billion, and more importantly, Generative AI new bookings alone amounted to $5.9 billion for the full fiscal year, including $1.8 billion in the fourth quarter. CEO Julie Sweet highlighted that these strong results stem from the company's "unique ability to deliver for our clients as they seek our help to reinvent and lead with AI."

Despite this strong growth, investors should note the impact of the proactive Business Optimization program initiated in Q4, which resulted in a $615 million charge. This strategic initiative—focused on upskilling, talent exiting where reskilling is not viable, and driving operational efficiencies—is expected to incur a total charge of approximately $865 million over the six-month period. While this contributed to a decrease in GAAP operating margin for the quarter (down 270 basis points to 11.6%), the adjusted operating margin showed stability and slight growth, which is a good signal of underlying health.

Outlook and Commitment to Shareholder Value

Looking ahead to fiscal year 2026, the company projects continued growth, with full-year revenue expansion expected to be between 2% and 5% in local currency (or 3% to 6% when excluding a 1% to 1.5% impact from its U.S. federal business). This is coupled with a positive outlook for earnings, as adjusted EPS is forecasted to rise to between $13.52 and $13.90, representing a 5% to 8% increase.

Accenture’s commitment to shareholder returns remains unwavering. The company returned $8.3 billion to shareholders in fiscal 2025, including $4.6 billion in share repurchases and $3.7 billion in cash dividends, and has committed to returning at least $9.3 billion in fiscal 2026. This confidence is further exemplified by the declaration of a new quarterly cash dividend of $1.63 per share, a 10% increase over the previous quarterly dividend.

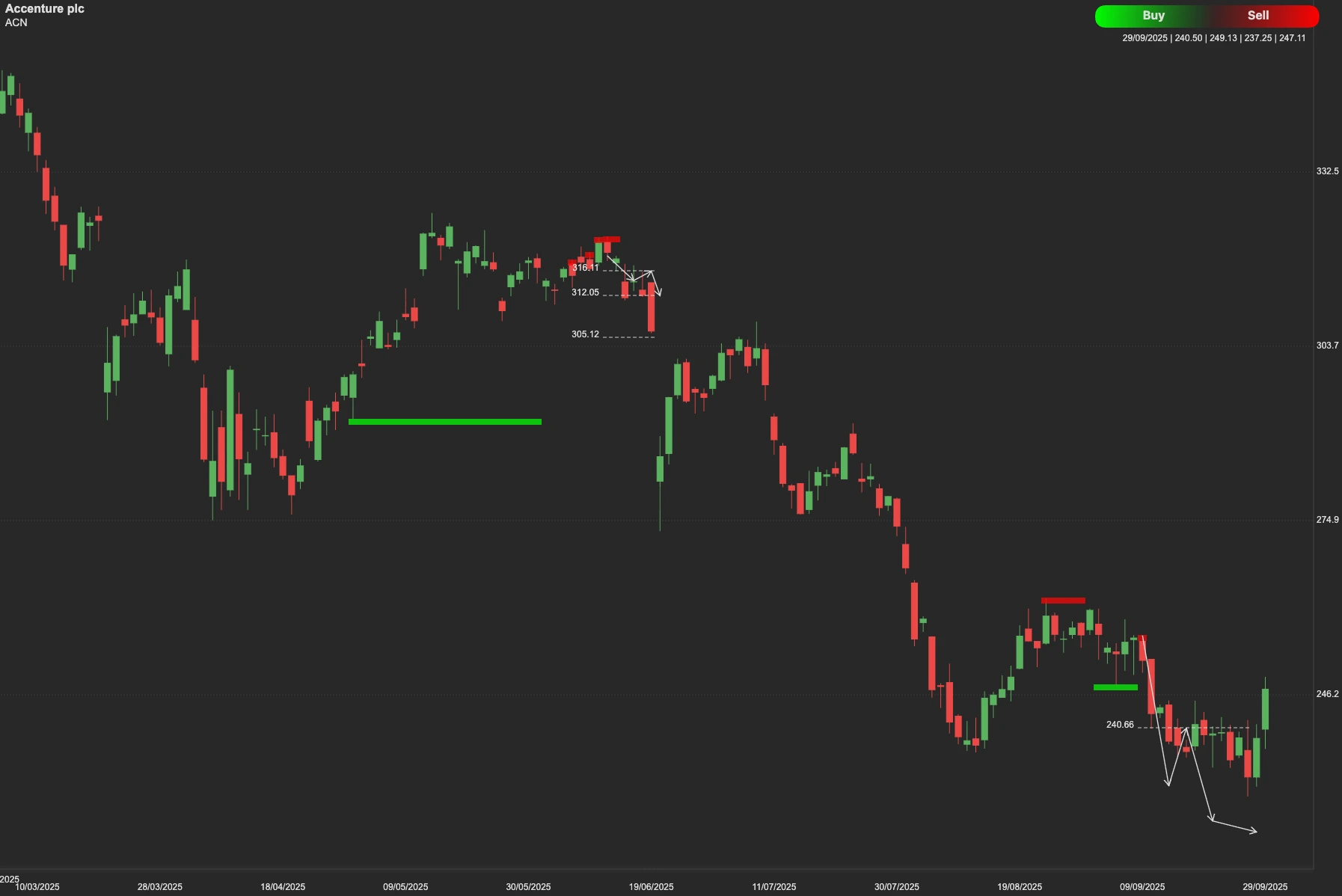

Technical Price Analysis: Key Levels for ACN

For the near-term outlook, investors should closely monitor the current resistance point at $265. Should ACN stock sustain a move and hold convincingly above this threshold, it would open the path for the next price objective at $280. Conversely, if the stock fails to hold and pulls back, it will find initial support at the $231 level. A deeper correction could see the stock test a more significant support area around $215.

Looking longer term, investors should note that ACN faces a significant resistance zone at $323. A decisive move above that level would be needed to open the door for a more extended bullish trend. Until then, the stock remains in a watchful range, balancing its growth story with the market’s technical signals.