Danaher Corporation (DHR) Reports Third-Quarter Results Exceeding Expectations

Danaher Corporation (NYSE: DHR), the global life sciences and diagnostics innovator, announced better-than-anticipated results for the third quarter of 2025. The performance, driven by core business strength and operational excellence, set the stage for a key technology showdown on the stock chart.

Overview of Third Quarter 2025 Financial Performance

Adjusted Earnings Beat: Net earnings reached $908 million ($1.27 per diluted share), up from $818 million a year earlier. On a non-GAAP basis, adjusted diluted net earnings per common share were $1.89, surpassing prior expectations and showing strong growth from the prior year's $1.71.

Revenue Growth: Revenues increased by 4.5% year-over-year to $6.1 billion. Non-GAAP core revenue growth was a healthy 3.0%.

Cash Flow Generation: Operating cash flow was $1.7 billion, and non-GAAP free cash flow came in at $1.4 billion, underscoring Danaher’s solid liquidity position.

CEO Rainer M. Blair specifically credited the Danaher Business System (DBS)-driven execution, coupled with continued momentum in the high-growth bioprocessing business and better-than-anticipated respiratory revenue from Cepheid, for the strong outcome.

Segment Performance and Future Guidance

Biotechnology was the clear leader, delivering 9.0% GAAP sales growth to $1,798 million and 6.5% core sales growth. Diagnostics also showed strength with 4.0% GAAP sales growth to $2,463 million and 3.5% core sales growth. Life Sciences remained the soft spot, experiencing just 0.5% GAAP sales growth and a 1.0% decline in core revenue.

Looking forward, Danaher maintained its full-year 2025 adjusted diluted net earnings per common share guidance range of $7.70 to $7.80. The company also expects non-GAAP core revenue to grow in the low-single digits for the full year, suggesting a cautious but stable outlook.

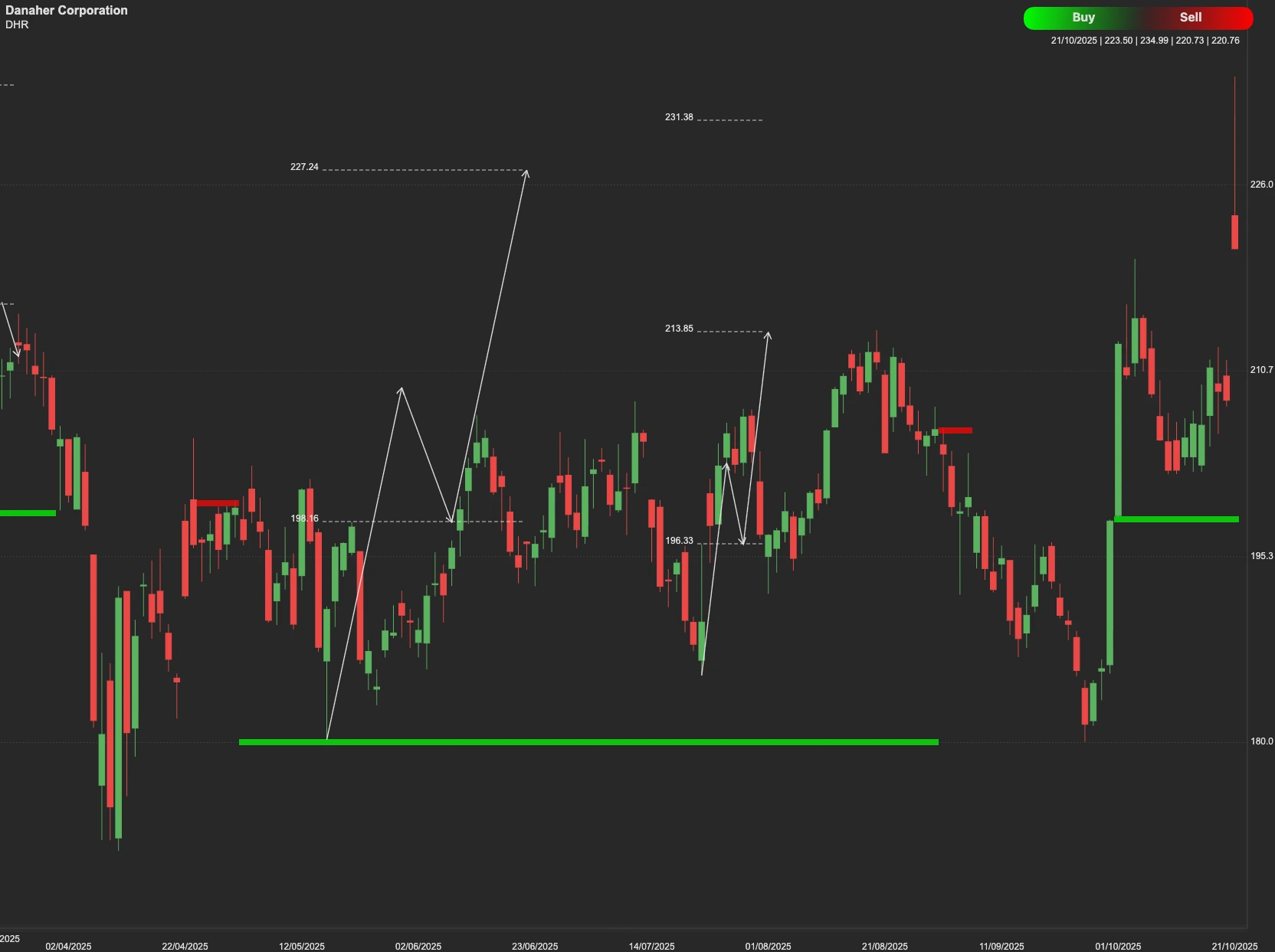

Technical Analysis

From a technical standpoint, DHR stock is testing resistance near $253. If the stock sustains levels above this threshold, the next upside target is around $281. Should the stock fail to break and hold above $253, it would likely face profit-taking and technical rejection. In this case, the stock could retreat to test the primary support level at $200. A break below the $200 support would potentially lead to a test of the further critical support located at $179.