IBM Stock Analysis: Strong Q3 Results Overshadowed by Cloud Slowdown

International Business Machines Corporation (NYSE: IBM) announced stronger-than-expected third-quarter 2025 results on October 22, 2025, beating revenue and profit estimates and prompting management to raise its full-year guidance for both revenue growth and free cash flow. But a slowdown in its key cloud software business overshadowed the upbeat earnings and raised investor concerns. Shares fell about 6% in extended trading.

Third-Quarter Highlights

Revenue Beat: Total revenue reached $16.3 billion, up 9% year-over-year (or 7% at constant currency), exceeding expectations.

Profit Acceleration: Operating (Non-GAAP) diluted EPS hit $2.65, a 15% increase year-over-year. On Non-GAAP basis, operating gross profit margin expanded by 1.2 points to 58.7%.

Cash Flow Power: Year-to-date, net cash from operating activities is $9.2 billion, and free cash flow is $7.2 billion, providing ample "fuel for investments and ability to return value to shareholders," as noted by CFO James Kavanaugh. The company also approved a quarterly dividend of $1.68 per share, to stockholders of record on November 10, 2025. With payment of the December 10, 2025 dividend, IBM will have paid consecutive quarterly dividends every year since 1916.

Raised Guidance: CEO Arvind Krishna’s declaration that the company’s AI book of business now stands at over $9.5 billion. Given the strength of business, the company raised its full-year revenue growth forecast to more than 5% at constant currency, and reaffirmed its free cash flow guidance of about $14 billion for the full year.

Segment Performance

Infrastructure Dominance: This segment was the standout performer, growing 17% (15% at constant currency) to $3.6 billion. This was primarily driven by the Hybrid Infrastructure sub-segment (up 28%), which saw a massive 61% surge in IBM Z revenue. The new mainframe, which is powered by chips specialized for AI applications, is being widely used by the financial industry, allowing for the maintenance of strict data residency and encryption rules as they work on adopting AI tech, CFO James Kavanaugh told Reuters.

Software Disappointment: Software revenue grew 10% (9% at constant currency) to $7.2 billion. However, the critical Hybrid Cloud/Red Hat growth decelerated to 14%, down from 16% in the prior quarter.

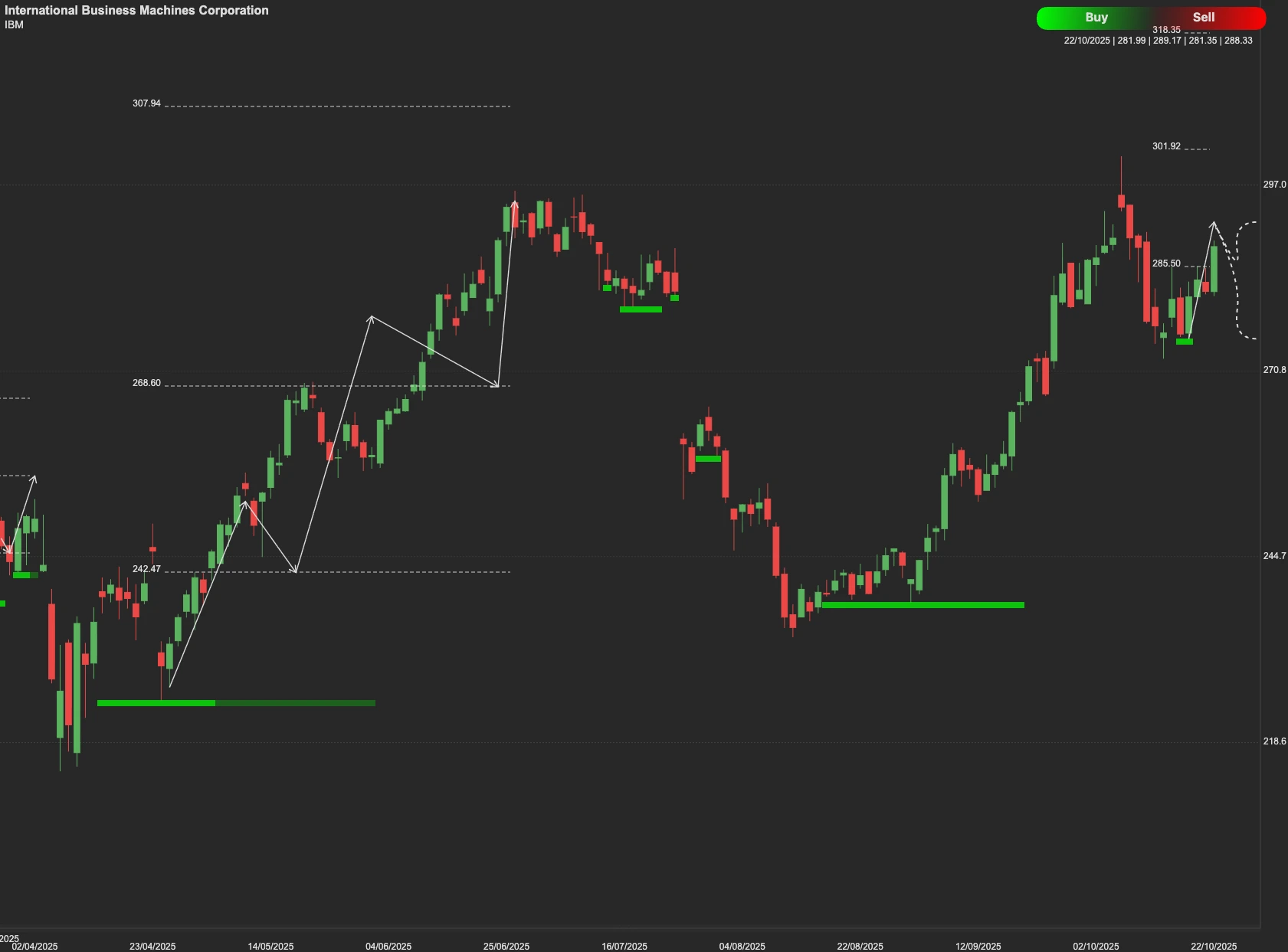

Technical Outlook

Despite the fundamental beat, the stock's immediate reaction was a technical retreat, reflecting the disappointment over cloud growth.

If the initial negative sentiment fades and the fundamental strength reasserts itself, a decisive push to close and stabilize above the prior key resistance level of $291 could open the way toward the next price objective at $306.

Given the 6% extended trading drop, the stock is currently seeking a new equilibrium. It may enter a period of consolidation, testing the immediate key support level at $250. If the selling pressure is sustained, a breach of this level could signal further profit-taking, leading the stock to test the more significant support level at $238.