Philip Morris Lifts Earnings Outlook on Strong Smoke-Free Growth

Philip Morris International (NYSE: PM) posted robust third-quarter 2025 results, raising its full-year earnings guidance as its smoke-free portfolio continues to drive growth. Reported diluted EPS rose 13.2% year-over-year to $2.23, while adjusted diluted EPS climbed 17.3% to $2.24. Net revenues increased 9.4% to $10.8 billion, fueled by accelerating adoption of its smoke-free products.

The Smoke-Free Engine: A Fundamental Powerhouse

The Q3 report cemented the Smoke-Free Business (SFB) as the primary engine of PMI’s growth. The SFB now accounts for 41% of total net revenues and over 42% of total gross profit, demonstrating substantial margin expansion. SFB shipment volumes surged by 16.6%, driving reported net revenues growth of 17.7% to $4.4 billion and reported gross profit growth of 19.5% to $3.1 billion. The company's smoke-free products (SFP) are now available in 100 markets, nearly half of which have at least two of the three flagship brands (IQOS, ZYN and VEEV) available for sale.

Key Growth Drivers:

IQOS (Inhalable smoke-free products): IQOS continues to gain steam globally, increasing its combined cigarette and HTU industry share by 0.9pp to 9.1%, reinforcing PMI’s 76% volume share of the global heat-not-burn category. HTU adjusted in-market sales (IMS) volumes grew by 9.0%, showing strength across Europe, Japan, and other key cities globally.

ZYN (Oral SFP): ZYN delivered impressive performance in the U.S., with an estimated offtake acceleration to 39% in the quarter, also driving category growth to over 40%. The growth of ZYN was supported by a wide range of commercial activities to further enhance the strength and presence of the brand, and ensure competitive price positioning following several quarters of reduced activity due to supply constraints. The international expansion of ZYN (now in 46 markets) further diversifies this high-growth segment.

Combustibles Resilience

Despite Cigarettes total shipment volume declining by 3.2%, reported net revenues for Combustibles grew 4.3% (up 1.0% organically), largely due to effective high single-digit pricing power, partly offset by negative mix dynamics. This drove another quarter of robust gross profit growth of 7.7% (4.8% organically).

Upgraded 2025 Guidance and Dividend Increase

Philip Morris raised its 2025 adjusted diluted EPS forecast to a range of $7.46–$7.56, up about 13.5%–15.1% from 2024. The company also increased its quarterly dividend by 8.9% to $1.47 per share, continuing its strong shareholder return record.

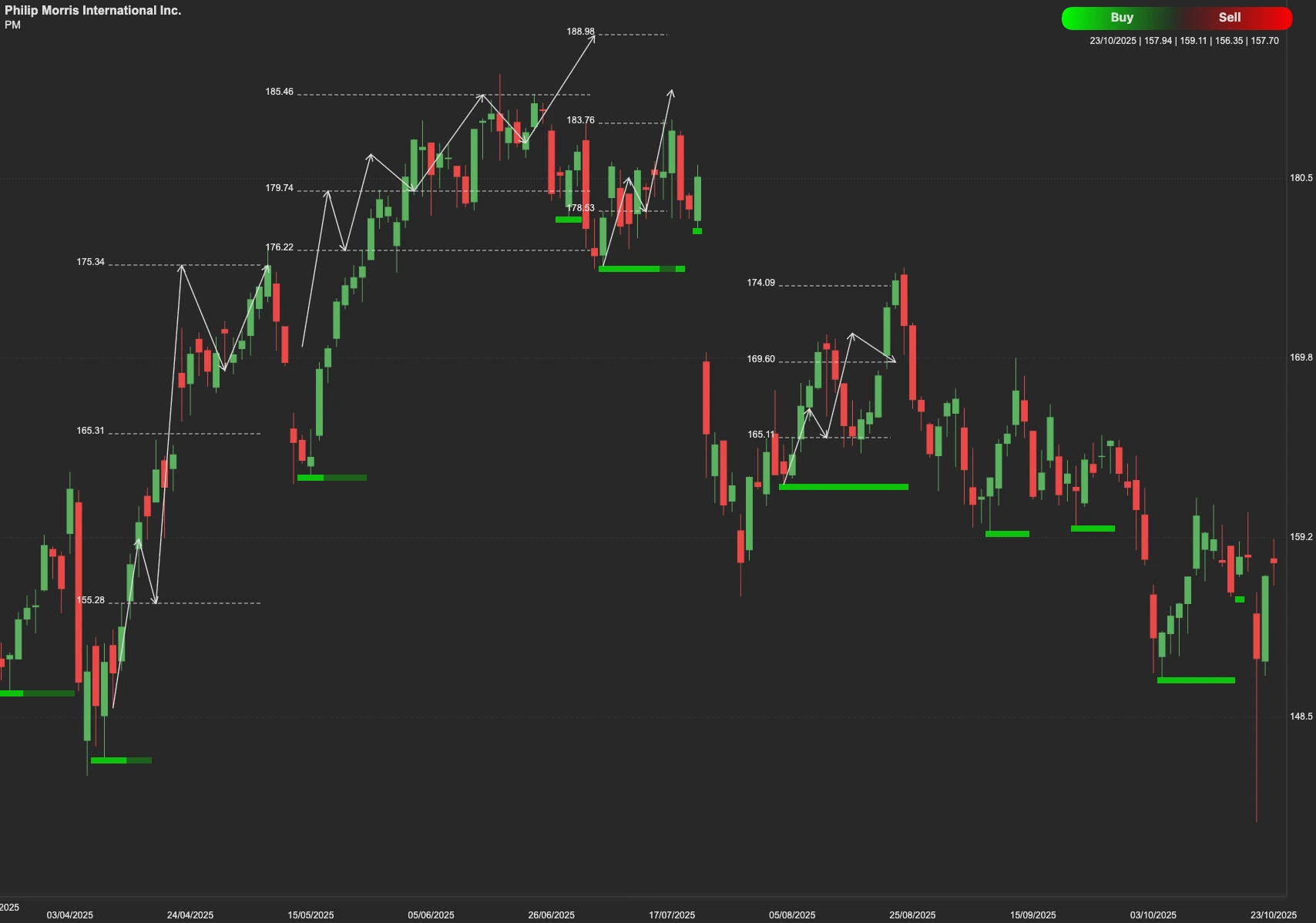

Technical Outlook

Technically, PM stock faces resistance at $169. If the price breaks and holds above this level, the next target could be around $183. However, failure to sustain above resistance may see the stock retesting support at $136, or deeper support near $119.