TSLA Stock Analysis: Margin Pressure vs. AI-Driven Growth

Tesla’s third-quarter 2025 financial results paint a complex, yet strategically clear, picture for investors. While the company delivered record vehicle volumes and achieved an unprecedented nearly $4.0 billion in free cash flow, demonstrating operational excellence and liquidity. Its GAAP operating margin contracted significantly to 5.8% from 10.8% year-over-year, reflecting that the company is at a critical juncture in its transformation from a pure auto manufacturer to an AI and energy powerhouse.

Financial Performance in Q3 2025

The company achieved record vehicle deliveries (497,099 units) and its highest-ever energy storage deployments (12.5 Gwh). Total revenue increased 12% year-over-year to $28.1 billion. However, the company’s operating income saw a 40% year-over-year decrease to $1.6 billion. Management attributed this margin contraction primarily to a substantial increase in operating expenses, specifically mentioning higher spending on SG&A, AI projects, and other R&D projects. Furthermore, lower regulatory credit revenue and a higher average cost per vehicle (due to sales mix and tariffs) also weighed on the bottom line.

While the Automotive segment's revenue growth was a modest 6% year-over-year to $21.2 billion, the true bright spots lie in Tesla's non-vehicle businesses: Energy Generation and Storage segment surged, with revenue increasing by 44% year-over-year to $3.4 billion and generating a record $1.1 billion in gross profit. Services and Other revenue grew 25% YoY to $3.5 billion.

The Engine for Future Growth

Tesla also achieved several milestones during the quarter.

The unveiling of the Megablock—a next-generation industrial storage product, a pre-engineered medium voltage battery system integrating four Megapack 3s—signals a major step toward simplifying utility-scale deployment, and new solar + Powerwall lease offerings are expected to boost demand for the residential energy products.

Key developments include the launch of the Robotaxi ride-hailing service in the Bay Area and the general availability of the Robotaxi iOS app, building crucial real-world data to refine its autonomy model. The deployment of FSD v14 brings a large portion of the Robotaxi FSD model to consumers plus improved handling of several complex scenarios such as avoiding road debris, yielding for emergency vehicles and adding arrival options to indicate where FSD should park.

The company explicitly stated its outlook: "we expect our hardware-related profits to be accompanied by an acceleration of AI, software and fleet-based profits."

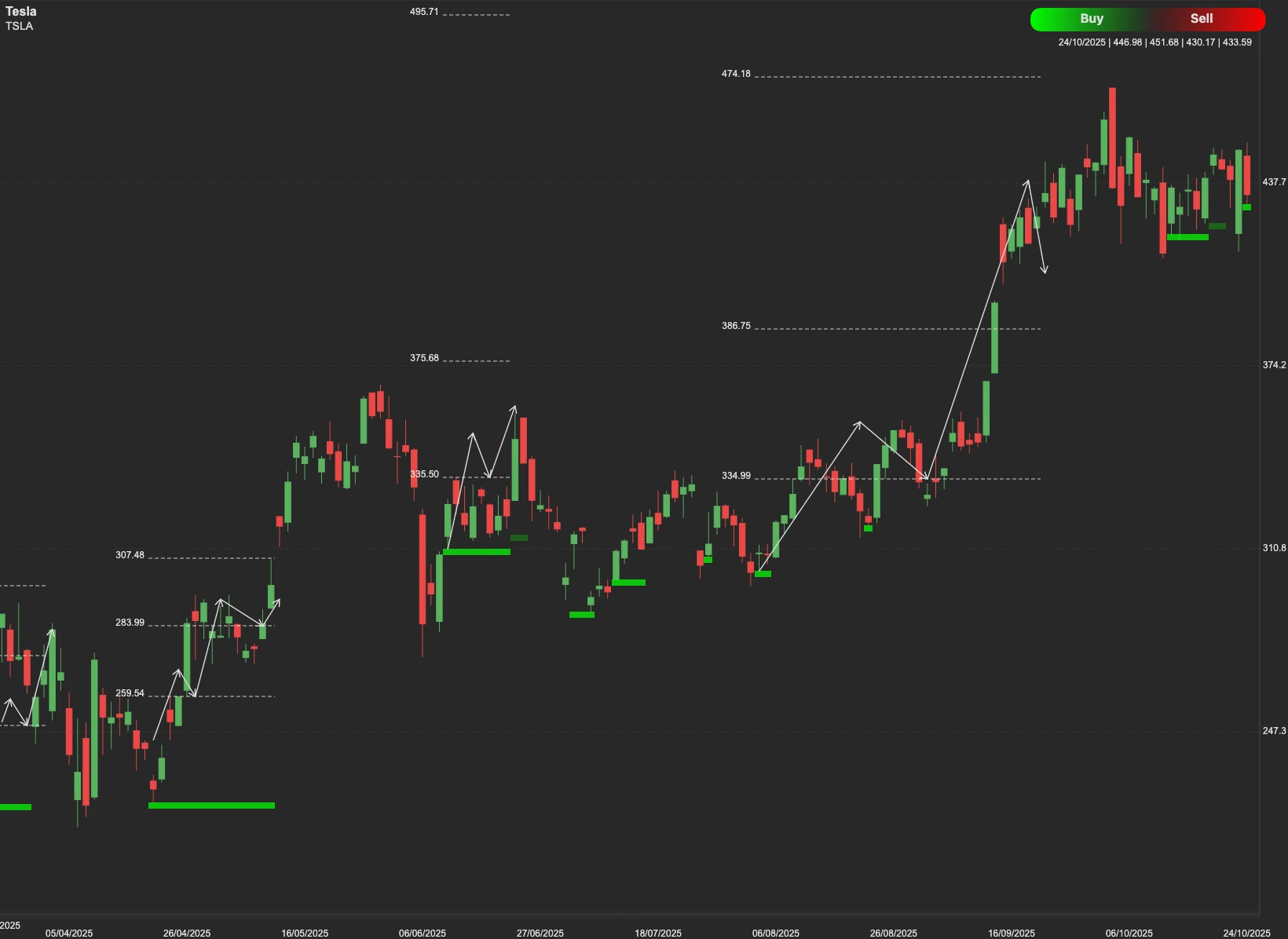

Technical Analysis

The initial resistance level for TSLA is set at $453. A successful close above this point suggests strong market confidence in the long-term AI/Energy vision outweighing the near-term margin compression. If sustained buying pressure pushes the stock past the next major resistance at $471, the path opens for a bullish continuation toward the near-term price goal of $500.

However, if the stock fails to maintain its current momentum, the first key support level to watch is $414. A further retracement could lead the stock to seek stronger support within the range of $381 to $359.