Mastercard (NYSE: MA) Defies Macro Headwinds with 15% Revenue Surge

Mastercard Incorporated (NYSE: MA) reinforced its leadership in global payments and digital commerce with a robust Third Quarter 2025 earnings report, announced on October 30, 2025. The results demonstrated sustained consumer and business resilience, particularly in cross-border activity.

The Q3 2025 Fundamental

Mastercard delivered exceptional top and bottom-line growth, comfortably exceeding prior-year figures:

Net Revenue: $8.6 billion, marking a powerful 17% year-over-year increase (15% on a currency-neutral basis).

Diluted EPS: $4.34, translating to a 23% jump from Q3 2024.

Adjusted Diluted EPS: $4.38, up 13% from the prior year.

CEO Michael Miebach highlighted the primary drivers of this success: “healthy consumer and business spending and continued robust performance of our differentiated services.”

The Engines of Growth

The growth of net revenue includes a 1 percentage point increase from acquisitions. The remaining increase was attributable to organic growth in the payment network and the value-added services and solutions.

-

Gross Dollar Volume: Gross dollar volume growth of 9%, on a local currency basis, to $2.7 trillion.

-

Cross-Border Volume: This segment, crucial for Mastercard's profitability, soared 15% on a local currency basis, reflecting continued strength in international travel and commerce.

-

Switched Transactions: Network activity remained high, with switched transactions increasing by 10%.

-

Value-Added Services: The company's strategy to diversify beyond pure transaction processing is paying off. Net revenue from value-added services and solutions surged 25% (22% on a currency-neutral basis), driven by offerings in security, digital and authentication, and business and market insights, including the recent launch of the Mastercard Commerce Media network.

Financial and Tax Headwinds

While growth was strong, the report also detailed the increased operating expenses and tax rate.

Operating Expenses: Adjusted operating expenses increased 15% year-over-year. While this included a 4 percentage point lift from acquisitions, the remaining increase was primarily attributed to higher general and administrative expenses.

Tax Impact: A significant headwind was the increase in the effective tax rate, which jumped from 15.6% to 21.5%. This was primarily due to the 15% global minimum tax (Pillar 2 Rules) that took effect in 2025 in Singapore and various other jurisdictions as well as a change in the geographic mix of earnings.

Despite these factors, Mastercard continued its commitment to shareholder return, repurchasing $3.3 billion worth of shares during the quarter and paying $687 million in dividends.

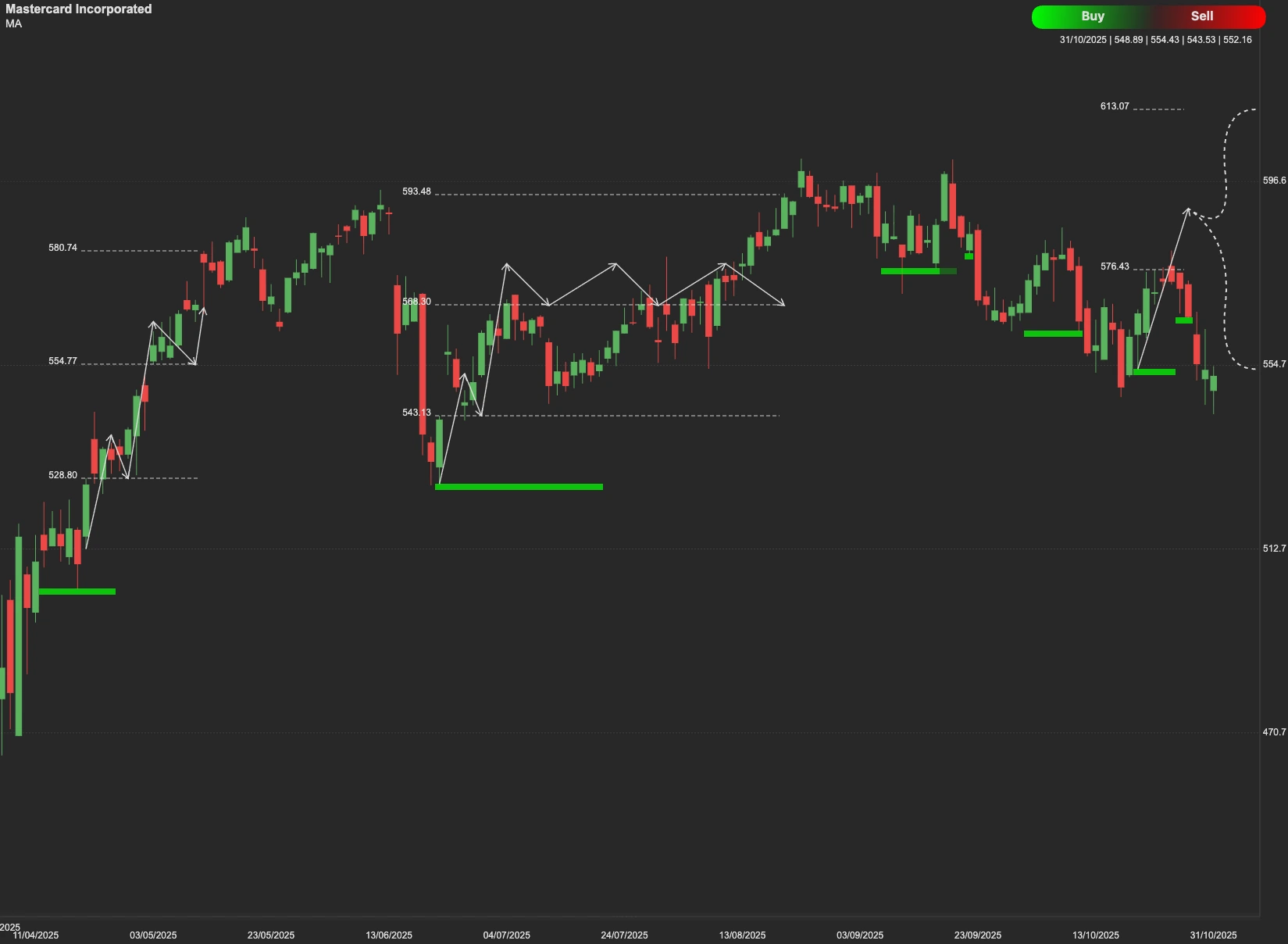

Technical Outlook

The immediate technical resistance level for MA stock is $578. A decisive breakout and sustained trading above $578 could signal strong investor confidence in the fundamental growth story. If this resistance is successfully converted to support, the stock's next technical objective is likely to be $602.

On the other hand, if the stock fails to push past the $578 resistance, the price would likely fall back to seek support. Investors should watch the initial support level at $521. A failure to hold $521 could lead to a deeper retracement toward the next major support zone, which lies between $503 and $489.