UnitedHealth Stock Plunges Nearly 20% as 2025 Results Reveal Margin Collapse and Revenue Decline Ahead

UnitedHealth Group (NYSE: UNH) suffered a sharp selloff after reporting fourth-quarter and full-year 2025 financial results, with shares plunging 19.6% as investors digested collapsing profitability, restructuring fallout, and a rare revenue decline outlook for 2026.

Performance Overview

For full-year 2025, UnitedHealth generated $447.6 billion in revenue, up 12% year-over-year. However, earnings from operations collapsed 41% to $19.0 billion, while net earnings attributable to shareholders fell 16.7% to $12.0 billion. Net margin compressed sharply to just 2.7%, down from 3.6% in 2024.

The deterioration was even more dramatic in the fourth quarter. Revenue rose 12% year-over-year to $113.2 billion, but operating earnings plunged 95% to only $380 million. Net income essentially evaporated, coming in at just $10 million, or one cent per share, compared with $5.6 billion, or $5.98 per share, a year earlier. A major driver of the collapse was a $1.6 billion after-tax charge in Q4 related to cyberattack response costs and restructuring. While excluding those items, adjusted diluted earnings per share for Q4 was $2.11.

Medical Costs Surge as Margins Crumble

UnitedHealth’s medical care ratio—a key profitability metric—jumped to an adjusted 88.9% in 2025 (the reported medical care ratio of 89.1% included a 20 basis point negative impact from lost contracts) from 85.5% in 2024, reflecting accelerating medical cost trends, CMS’s Medicare funding cuts, and Inflation Reduction Act impacts. Higher medical costs directly eroded margins across UnitedHealthcare and Optum Health.

UnitedHealthcare, which serves nearly 50 million people, grew full-year 2025 revenue 16% year-over-year to $344.9 billion but saw operating earnings fall 40% to $9.4 billion, with operating margins sinking to just 2.7%, compared to 5.2% in 2024.

The pressure was even worse at Optum Health. Full-year 2025 revenue slipped 3% year-over-year to $102.0 billion, while the segment swung to an operating loss of $278 million, down from $7.8 billion in profit the prior year. Adjusted earnings from operations were $2.3 billion in 2025 compared to $7.9 billion in 2024. The year-over-year decline was driven by continued reimbursement pressure due to Medicare funding reductions and elevated medical cost trends.

Optum Rx stood out as a bright spot, with full-year 2025 revenue rising 16% year-over-year to $154.7 billion and operating earnings climbing to $7.2 billion, compared to $5.8 billion in 2024, driven by growth in pharmacy services and volume growth from new and existing clients.

Optum Insight’s full-year 2025 revenues of $19.4 billion were up 4%, or $660 million, year-over-year, but operating earnings declined 16% to $2.6 billion, impacted by costs related to new product launches and continued investments to support future growth.

2026 Outlook Signals Revenue Decline

UnitedHealth forecasts 2026 revenue of more than $439 billion—implying a roughly 2% year-over-year decline, reflecting planned right-sizing across the enterprise. Management points out that overall U.S. membership will decline by more than 3 million in 2026.

Despite the lower revenue base, UnitedHealth is targeting earnings from operations above $24 billion and adjusted EPS above $17.75, banking on aggressive cost controls, repricing efforts, and margin recovery across its segments.

The company expects the medical care ratio to improve modestly to around 88.8% in 2026. Operating cost ratio is expected to be 12.8%, signaling a heavy focus on discipline after a turbulent year.

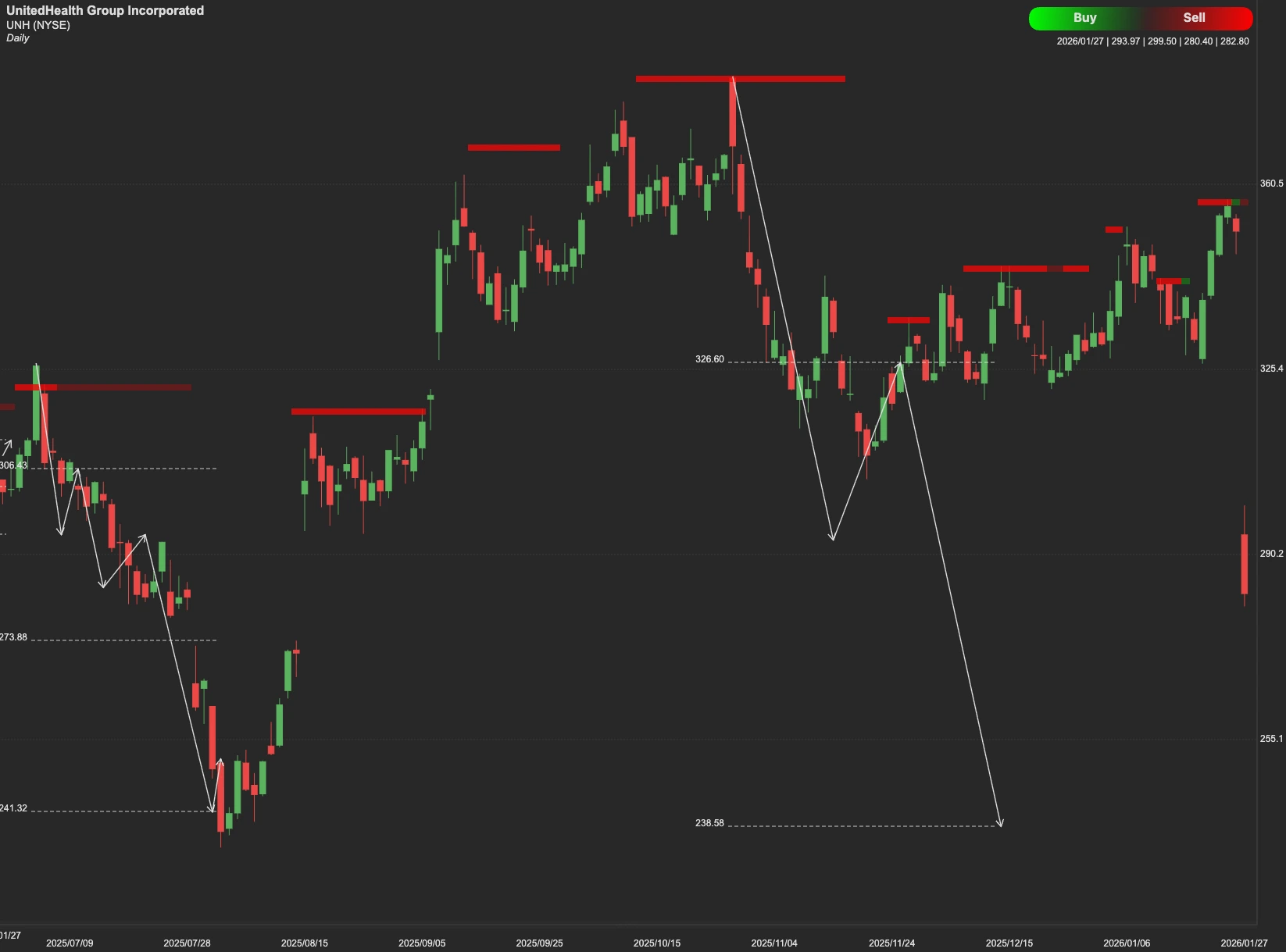

Technical Outlook

Following the nearly 20% plunge, the immediate challenge for UNH is the $337 level. If the stock can regain momentum and consolidate above this mark, the path opens for a recovery toward the next key resistance at $354. A sustained break above $354 would signal a potential trend reversal, with a target goal of $371.

Conversely, if the stock fails to gain traction, it may drift lower to seek support at $260. If macro or regulatory pressure intensifies, a further support floor exists at $235.