Airbnb Delivers Strong Q1 2026 Growth

Airbnb, Inc. (NASDAQ: ABNB) delivered an impressive start to 2026, combining accelerating revenue growth, strong international demand, and aggressive shareholder returns. The company’s first-quarter results reinforced the idea that Airbnb is evolving beyond a simple home-sharing platform into a broader global travel ecosystem powered by AI, experiences, services, and flexible accommodations.

Revenue Growth and Booking Strength Continue to Accelerate

Revenue climbed 18% year-over-year to $2.7 billion in Q1 2026, primarily driven by strong growth in nights stayed and a meaningful increase in Gross Booking Value per Night and Seats Booked (ADR), aided by an FX tailwind.

Gross Booking Value surged 19% to $29.2 billion, while Nights and Seats Booked increased more than 9%, demonstrating that demand remains resilient despite increased cancellations from the Middle East conflict.

Income from operations more than doubled, climbing to $86 million from $38 million in Q1 2025. However, interest income softened slightly to $155 million (down from $173 million in the prior quarter), leading to an income before income taxes of $281 million. Provision for income taxes was $121 million, compared to $19 million in Q1 2025.

Net income of $160 million increased slightly compared to $154 million a year earlier, while the net income margin sat at 6% compared to 7% in Q1 2025. Diluted net income per share was $0.26, up from $0.24.

Adjusted EBITDA rose 24% to $519 million, lifting adjusted EBITDA margin to 19%, compared to 18% in Q1 2025.

Balance Sheet, Cash Flow and Capital Allocation

As of March 31, 2026, Airbnb held $12.1 billion in cash, cash equivalents, short-term investments, and restricted cash, as well as $10.6 billion of funds held on behalf of guests.

For the three months ended March 31, 2026, Airbnb generated $1.7 billion in operating cash flow and free cash flow, underscoring the platform’s highly cash-generative business model. While free cash flow declined slightly year-over-year, management made clear that this was primarily due to working capital timing related to the expansion of Reserve Now, Pay Later.

The company’s financial credibility also improved meaningfully during the quarter after receiving inaugural investment grade ratings of A- from S&P Global Ratings and Baa1 from Moody’s. Following these upgrades, Airbnb successfully completed a $2.5 billion senior unsecured debt offering, using part of the proceeds to fully repay the $2.0 billion convertible senior notes that matured in March 2026.

Airbnb remains highly active in returning capital to shareholders. During Q1 alone, the company repurchased $1.1 billion of Class A stock, with $4.5 billion remaining under its current authorization as of March 31. Airbnb has reduced its fully diluted share count by approximately 9% since launching buybacks in Q3 2022.

Strategic Growth Engines

What stood out most was the strength of Airbnb’s global expansion strategy. India origin nights booked grew approximately 50% year-over-year, while Brazil continued posting more than 20% growth for the third consecutive quarter. First-time booker growth accelerated to 10%, the highest level since early 2022, with particularly strong acceleration in Brazil, Japan, and India, three of the key expansion markets.

The company is also seeing meaningful traction from its app ecosystem. Nights booked through the Airbnb app rose 22% year-over-year and now account for 63% of total nights booked, up from 58% a year ago. That shift matters because app users typically demonstrate higher retention, stronger engagement, and lower acquisition costs over time.

Another key driver is Reserve Now, Pay Later, which represented roughly 20% of global GBV during the quarter. It’s one of the clearest examples of a change that is good for guests and good for the business: guests tend to book more when they have the flexibility to pay later.

Management also continues expanding Airbnb beyond traditional lodging. Experiences and services are increasingly becoming strategic growth engines. Early data is encouraging: Nearly a quarter of guests who are new to Airbnb and book an experience go on to book a stay or a service—and roughly one in three experience bookers book a stay within 90 days.

AI adoption is becoming another competitive advantage. Management revealed that nearly 60% of the code is now co-authored with AI, helping teams iterate faster and reduce operational costs. Customer support automation is already producing measurable financial benefits, with more than 40% of AI-assisted support issues resolved without human agents. This helped reduce cost-per-booking by approximately 10% year-over-year.

Business Outlook

Looking ahead to the second quarter of 2026, Airbnb expects revenue between $3.54 billion and $3.60 billion, representing a year-over-year growth of 14% to 16%. While the company anticipates Nights and Seats booked growth to slightly decelerate, relative to Q1 2026, assuming an estimated roughly 100bps headwind related to the conflict in the Middle East.

Management expects GBV to increase in the low double digits year-over-year in Q2 2026. Adjusted EBITDA and margins are projected to trend upward year-over-year for the Q2 period.

Management raised full-year guidance and now expects year-over-year revenue growth in the low-to-mid teens for 2026, alongside an Adjusted EBITDA margin of at least 35%.

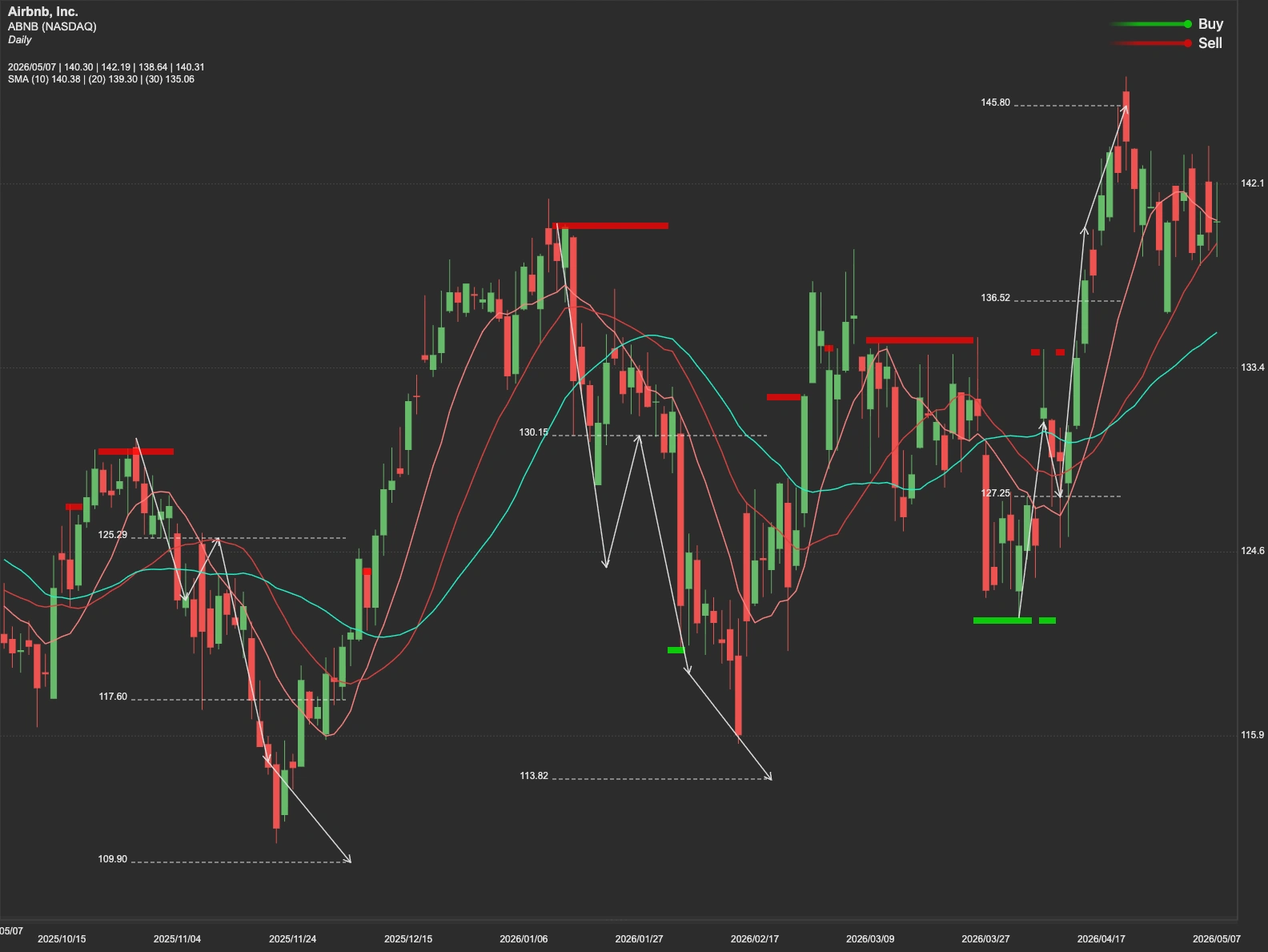

Technical Analysis

From a technical perspective, ABNB stock is currently facing stiff resistance at $155. If the stock can achieve a sustained close above this level, it clears the path for a technical breakout toward the next primary target of $167.

However, failure to break and hold above $155 could trigger near-term consolidation or downside pressure. In that scenario, traders will likely watch the $130 support zone as the first major test. If broader market weakness or macro uncertainty intensifies, the stock could potentially test the deeper support area around $115.