Airbnb Stock Analysis: Growth Accelerates but Margins Tighten

Airbnb (NASDAQ: ABNB) closed out 2025 with a significant performance boost, reporting double-digit growth in its key metrics for the fourth quarter. Despite this operational momentum, the stock finds itself in a complex technical position, struggling to establish a definitive upward trajectory.

Revenue and Booking Growth

In the fourth quarter of 2025, revenue reached $2.8 billion, representing 12% year-over-year growth, or 11% excluding foreign exchange impact, driven by strong growth in nights stayed and a moderate increase in ADR. Gross Booking Value climbed to $20.4 billion, up 16% year-over-year, or 13% ex FX, marking the company’s strongest GBV growth quarter in more than two years. Nights and Seats Booked increased 10% year-over-year to 121.9 million, reflecting sequential acceleration from the third quarter. ADR rose to $168, increasing 6% year-over-year, or 3% excluding FX.

For the full year 2025, Airbnb generated $12.2 billion in revenue, up 10% compared to 2024. Gross Booking Value reached $91.3 billion, up 12% year-over-year, or 10% excluding FX. Total Nights and Seats Booked rose 8% to 533 million, demonstrating steady global demand despite macroeconomic uncertainties.

Profitability Moderates as Investment Spending Increases

Income from operations in Q4 declined to $269 million from $430 million a year earlier. Net income totaled $341 million, compared to $461 million in Q4 2024, resulting in a net income margin of 12% versus 19% in the prior year, reflecting increased investments in new growth and policy initiatives, as well as approximately $90 million of non-income tax matters. Diluted earnings per share came in at $0.56, down from $0.73 last year. Adjusted EBITDA reached $786 million, up 3% year-over-year, with a margin of 28% compared to 31% in Q4 2024.

For the full year, net income reached $2.51 billion compared to $2.65 billion in 2024. Diluted EPS was $4.03 versus $4.11 last year. Adjusted EBITDA totaled $4.3 billion, representing a 35% margin.

Cash Flow Strength and Capital Allocation

Operating cash flow remained robust. In Q4 Airbnb generated $526 million in net cash provided by operating activities and $521 million in free cash flow, underscoring the strength of the company's cash-generating business model. As of December 31, 2025, Airbnb held $11 billion in cash, cash equivalents, and short-term investments, along with $7 billion of funds held on behalf of guests, providing substantial financial flexibility.

During Q4 alone, the company repurchased $1.1 billion in stock, with $5.6 billion remaining under its authorization. The repurchase program continues to be executed as part of the company's broader capital allocation strategy, which prioritizes investments in organic growth, strategic acquisitions or partnerships, and return of capital to shareholders, in that order.

Geographic Performance

Geographically, performance remained broad-based. North America delivered mid-single digit growth of Nights and Seats Booked during Q4 2025 compared to Q4 2024, with ADR rising 5%. EMEA saw high-single digit growth in Nights and Seats Booked during Q4 2025 compared to Q4 2024, with ADR up 12%, largely due to FX. Latin America posted high-teens growth in Nights and Seats Booked during Q4 2025 compared to Q4 2024, led by Brazil. While Asia Pacific achieved mid-teens growth in Nights and Seats Booked during Q4 2025 compared to Q4 2024, with India emerging as one of the fastest growing origin markets.

2026 Outlook Points to Continued Acceleration

Looking ahead to Q1 2026, Airbnb expects revenue between $2.59 billion and $2.63 billion, representing 14% to 16% year-over-year growth, including an FX tailwind. The company anticipates low teens GBV growth, driven by high-single-digit booking growth and moderate ADR increases. Adjusted EBITDA margin is expected to remain approximately flat year-over-year.

For the full year 2026, management expects revenue growth to accelerate to at least low double digits, while maintaining a stable adjusted EBITDA margin as top-line efficiencies are reinvested into growth initiatives.

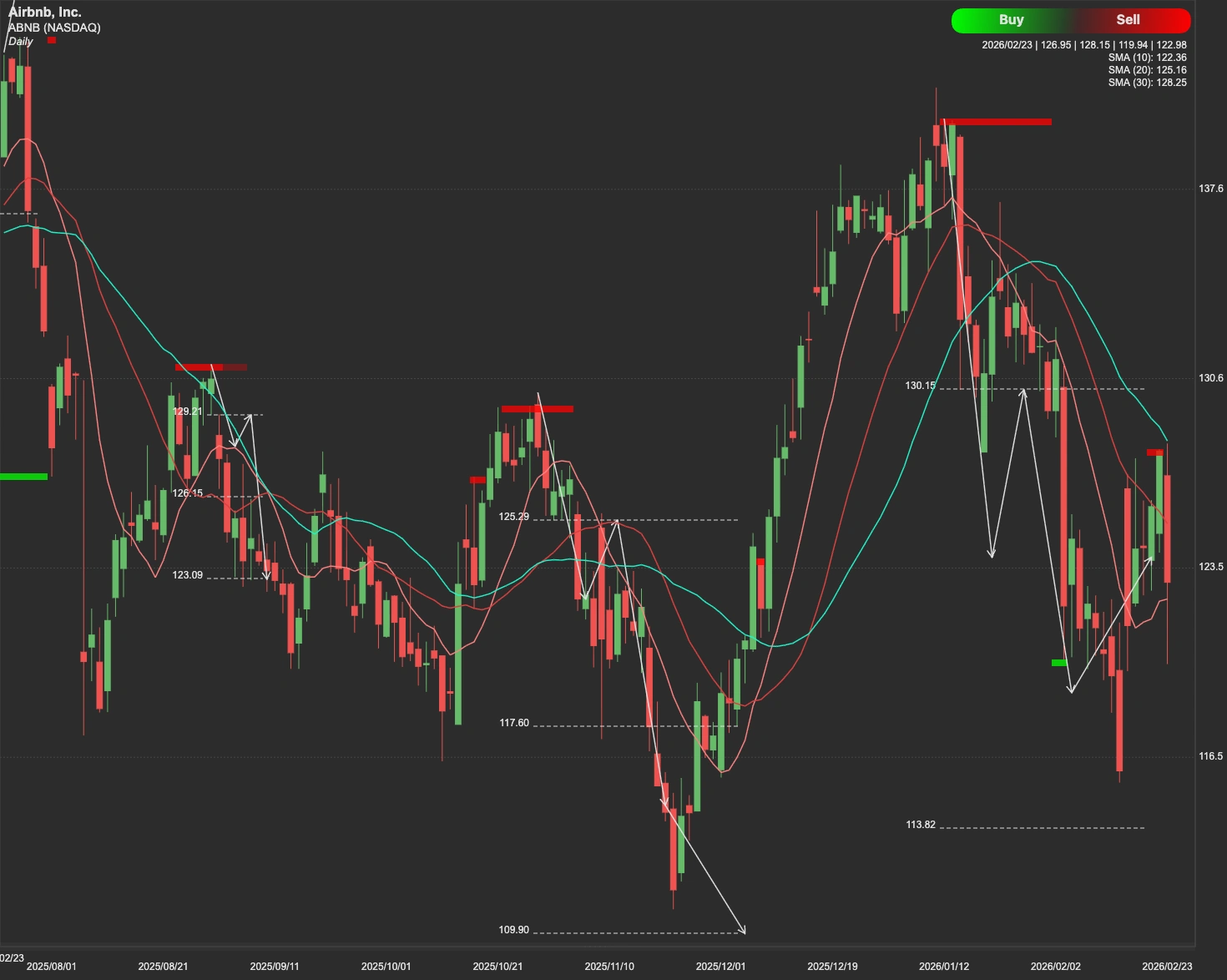

The Technical Landscape

Despite these strong fundamentals, ABNB stock is currently navigating a period of indecision. The equity is facing immediate resistance at the $134 level. For bulls to regain control, the stock must decisively break through this barrier. A successful breach of $134 would set the stage for a test of much stronger resistance at $143.

However, if the stock fails to break or sustain levels above $134, selling pressure may increase. In such a scenario, the stock may retreat to seek support at $111. If that level fails to hold, a deeper correction toward the secondary support zone at $103 could be on the horizon.