Airbnb Stock Analysis: Q3 Strength Can’t Lift ABNB as Shares Struggle at Key Resistance Levels

Airbnb (NASDAQ: ABNB) delivered another solid quarter in Q3 2025, posting revenue of $4.1 billion, up 10% year-over-year, landing at the high end of its guidance range.

Q3 Financial Strength and Key Growth Drivers

The quarter was marked by solid underlying business health. Gross Booking Value (GBV) rose 14% year-over-year to $22.9 billion, driven by an acceleration in Nights and Seats Booked, which grew 9% to 133.6 million. Net income remained stable at $1.4 billion, with a net income margin of 34%, compared to 37% in Q3 2024. Adjusted EBITDA increased 5% year-over-year to $2.1 billion, with an adjusted EBITDA margin of 50%, compared to 52% in Q3 2024.

Management attributed this success to a focus on four key areas: improving the core service, international expansion, product expansion (Services and Experiences), and AI integration.

Highlights driving growth include:

Reserve Now, Pay Later: Launched in the U.S., this flexible payment option helped drive the acceleration of Nights and Seats Booked in Q3, offering guests $0 upfront for eligible stays.

International Strength: The average growth rate of nights booked in expansion markets, particularly Japan (first-time bookers increased over 20%) and India (first-time bookers increased nearly 50%), continued to grow at twice the rate of core markets, confirming the multi-year international strategy is paying off.

AI Integration: The new AI assistant has already proven efficient, reducing the need for guests to contact a human agent by roughly 15% in the U.S. and cutting resolution times from hours to seconds.

Outlook and Investment Trade-Offs

For the fourth quarter, Airbnb anticipates revenue between $2.66 billion and $2.72 billion, representing 7% to 10% year-over-year growth. However, management signaled continued investment in new growth and policy initiatives, particularly the $200 million allocated towards Services and Experiences in 2025. This focus on long-term growth is expected to cause Q4 2025 Adjusted EBITDA to be flat-to-down slightly year-over-year, with the Adjusted EBITDA Margin expected to decline.

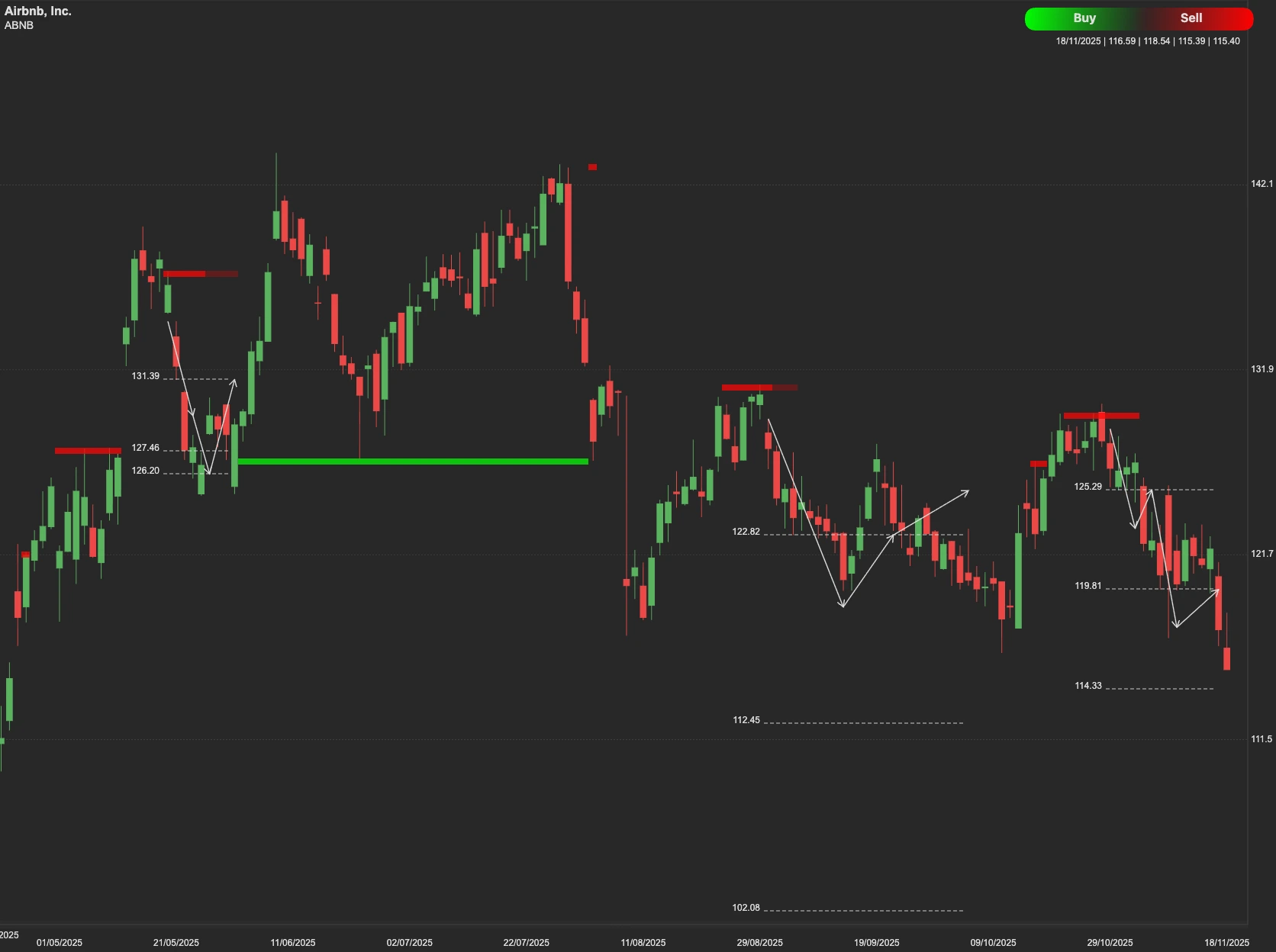

Technical View

Despite the solid fundamental backdrop and a positive outlook for Q4 revenue, ABNB stock is struggling to reflect this optimism in its price action.

From a technical perspective, ABNB is currently facing an immediate resistance level at $128. Should the stock so far clear this level, it is expected to encounter increased resisting force at the level of $138. The stock’s next move will likely hinge on whether it can clear the $128 and $138 resistance levels.

Conversely, if the stock fails to break resistances as investors are weighing the company's investments in new growth initiatives, the slight dip in Q3 net income margin, and the upcoming $2.0 billion debt maturity against its current valuation, it may seek support. The immediate support level is identified at $105. A breakdown below $105 could trigger further declines, leading the stock to test the stronger support cluster in the $99–$94 range.