AMD Stock Analysis: Record 2025 Results Reinforce AI-Led Growth

AMD (NASDAQ: AMD) closed 2025 with a standout financial performance, underscoring its transformation into a scaled, high-margin computing and AI platform company. As AMD Chair and CEO Dr. Lisa Su noted, entering 2026, the company is carrying solid momentum across its business, supported by accelerating adoption of EPYC and Ryzen CPUs and the rapid scaling of its data center AI franchise.

Fundamental Strength: A Record-Breaking Year

For full-year 2025, AMD delivered record revenue of $34.6 billion, up 34% year over year. GAAP gross margin was 50%, up 1 ppt year over year, and non-GAAP gross margin was 52%, down 1 ppt. Profitability expanded sharply, with GAAP net income reaching $4.3 billion, up 164% year over year, and non-GAAP net income climbing to a record $6.8 billion, up 26%. Non-GAAP diluted earnings per share was a record $4.17. Operating leverage was evident as non-GAAP operating income surged to a record $7.8 billion, reflecting AMD’s ability to scale efficiently even while increasing strategic investment.

The fourth quarter was particularly strong. Revenue reached $10.3 billion, up 34% year over year. GAAP operating income more than doubled year over year. On a non-GAAP basis, the company achieved record operating income of $2.9 billion and record net income of $2.5 billion ($1.53 per share). Data Center segment revenue hit a quarterly record of $5.4 billion, driven by strong demand for AMD EPYC™ processors and the continued ramp of AMD Instinct GPU shipments.

From a margin perspective, AMD’s Q4 non-GAAP gross margin reached 57%. The quarter benefited from $390 million in MI308 revenue to China and a $360 million release of previously reserved inventory. Excluding those factors, margins remained healthy at approximately 55%.

Segment Momentum Tells a Clear Story

AMD’s growth in 2025 was broad-based but clearly led by Data Center and Client:

Data Center segment delivered $16.6 billion in annual revenue, up 32% year over year, reflecting sustained enterprise and hyperscaler demand.

For the full year 2025, Client and Gaming segment revenue surged 51% year over year to $14.6 billion, driven by Ryzen market share gains and a richer product mix.

Embedded segment softened slightly for the year due to earlier inventory adjustments, down 3% year over year to $3.5 billion, but showed signs of stabilization in Q4.

Strategic partnerships, the Helios rack-scale platform, and deep ecosystem integration announced at CES 2026 further reinforce AMD’s long-term growth narrative going into 2026.

2026 Outlook Signals Continued AI-Led Growth with Stable Profitability

Looking ahead, AMD guided Q1 2026 revenue to approximately $9.8 billion, implying 32% year over year growth despite a modest sequential decline. Non-GAAP gross margin is expected to remain around 55%.

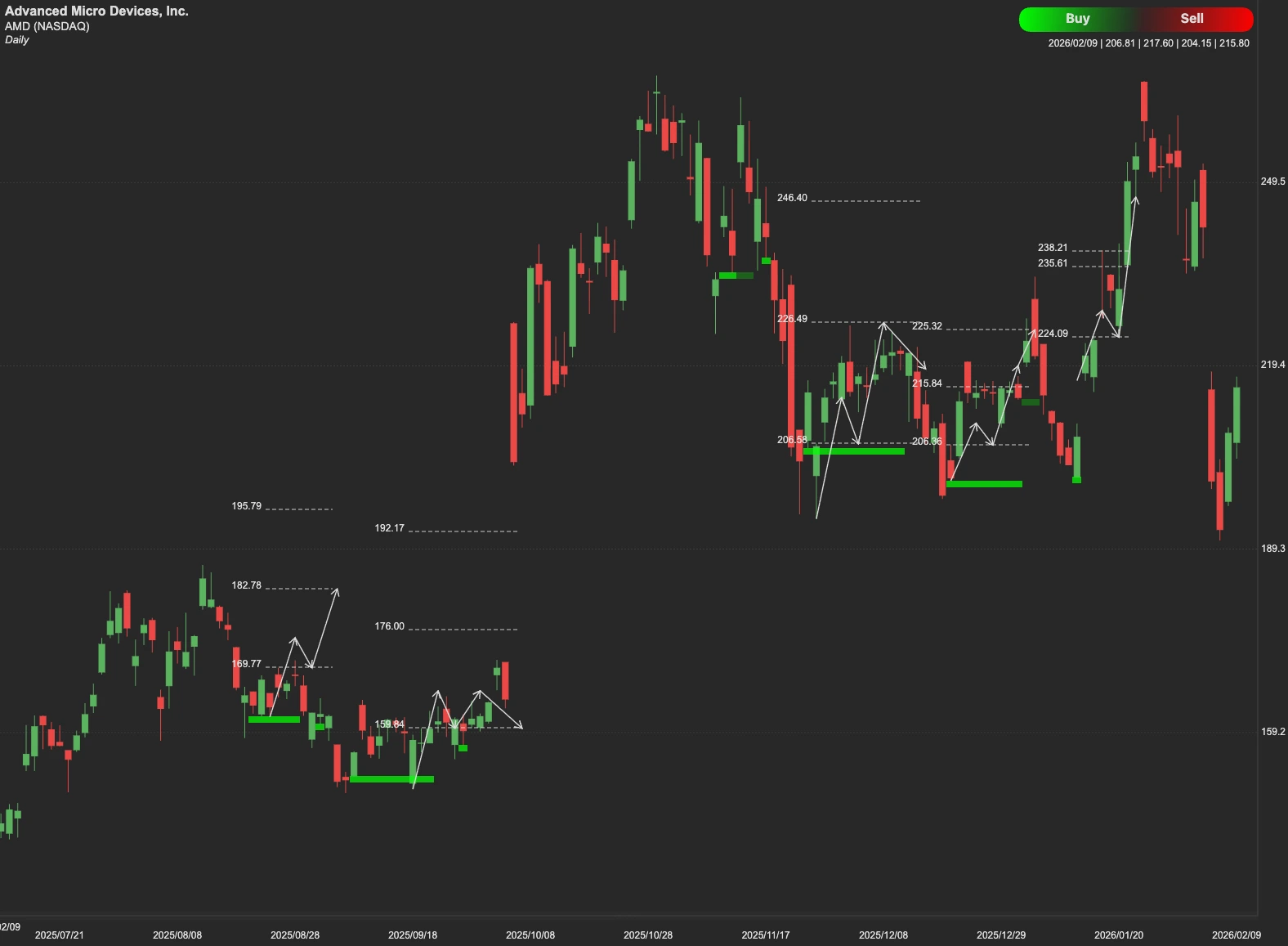

Technical Analysis

From a technical standpoint, $236 represents a critical resistance level for AMD shares. A sustained break and hold above this level would likely confirm bullish momentum, opening the path toward the next upside target near $271.

However, if AMD can't remain above $236 could trigger profit-taking. In that scenario, the stock may seek initial support around $196. If broader market pressure or sentiment deterioration emerges, a deeper retracement toward $166 would represent the next major support zone.