American Express Company Reaffirms 2026 Outlook Amid Strong Demand and Strategic Expansion

American Express Company (NYSE: AXP) delivered a robust start to 2026 with a strong performance that highlights the resilience of its premium membership model. Following the earnings release on April 23, the company demonstrated that its "growth engine" is firing on all cylinders, combining strong top-line revenue growth with double-digit bottom-line expansion.

Fundamental Strength: The Premium Advantage

From a fundamental perspective, AXP’s performance was notably strong. Total revenues net of interest expense reached $18.9 billion, marking an 11% year-over-year increase (10% FX-adjusted), supported by broad-based growth across Card Member spending, card balances, and fee-based income. Card Member spending accelerated to 10% growth (9% FX-adjusted), the fastest pace in three years, driven by strong demand and engagement with AXP's premium products. Total Billed business was $428 billion, up 10%, or 9% FX-adjusted.

Revenue composition further validates the quality of growth. Discount revenue increased 9% year-over-year to $9.5 billion, driven by higher billed business, while net card fees surged 18% to $2.8 billion, benefiting from expansion in premium card portfolios. Service fees and other revenue expanded 13% to $2.0 billion. Net interest income grew 13% to $4.7 billion, supported by higher revolving loan balances.

On the cost side, total expenses increased 11% year-over-year to $13.9 billion, driven primarily by higher variable customer engagement costs, the U.S. Platinum Card refresh, and usage of travel- and lifestyle-related benefits, as well as higher operating expenses. Notably, Card Member services expense surged 49%, primarily due to higher usage of Card Member benefits and the new U.S. Platinum benefits.

Profitability metrics were equally compelling. Net income rose 15% to $3.0 billion, while earnings per share climbed 18% to $4.28.

Credit quality remains stable. The net write-off rate improved slightly to 2.0% from 2.1% a year ago. Provisions for credit losses rose modestly to $1.3 billion, compared with $1.2 billion a year ago.

From a capital perspective, the company remains highly efficient. It returned $2.3 billion to shareholders during the quarter and maintained strong profitability metrics, with return on average equity at 35.2% and return on average common equity at 36.6%. GET1 ratio was 10.5% for Q1 2026. Book value per common share was $47.50.

Strategic Expansion & Innovation

Strategically, American Express continues to deepen its ecosystem. Partnerships with major sports leagues like the NFL and NBA and expansion of its card portfolio reflect a long-term focus on engagement and differentiation. The launch of new Graphite Business Cash Unlimited Card marks the beginning of the largest commercial product expansion in the company's history. Ongoing AI innovation, including the announcement of the Amex Agentic Commerce Experiences developer kit and industry-first Agent Purchase Protection.

Management also reaffirmed full-year guidance, expecting 9%–10% revenue growth and EPS between $17.30 and $17.90, while increasing investment in marketing and technology.

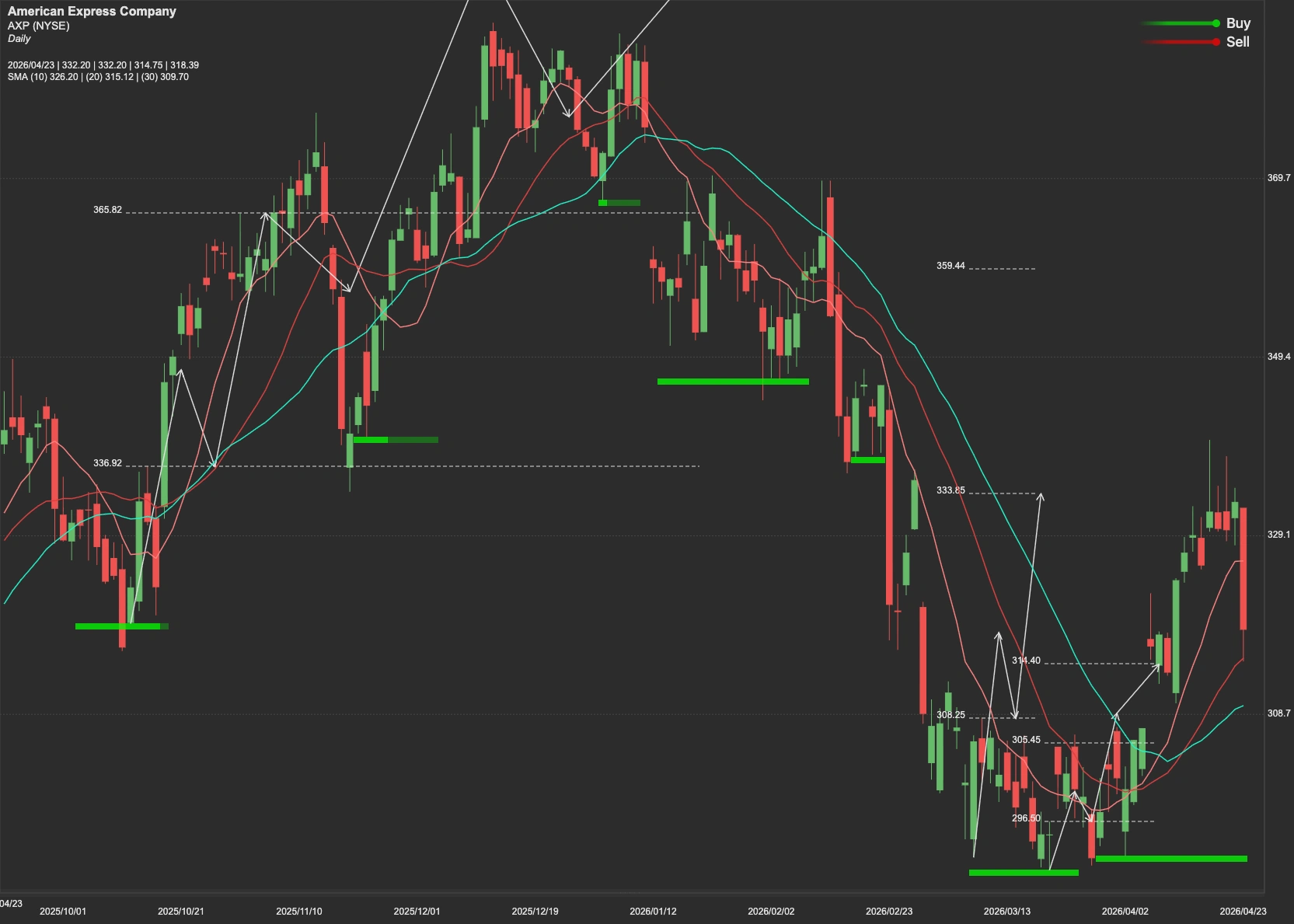

Technical Analysis

From a technical standpoint, AXP stock is currently approaching a critical resistance level around $340. A sustained breakout above this level could open the path toward the next target at $369, signaling continued bullish momentum. Should the stock fail to consolidate above $340, a retracement is possible. Initial support is found at $297. In a more bearish scenario or a broader market correction, the further floor sits at $265.