Apple Delivers Record Q1 Results as iPhone Demand and Services Momentum

Apple (NASDAQ: AAPL) opened fiscal 2026 with a record-setting first quarter, reinforcing its position as one of the most resilient and profitable large-cap technology companies globally. The company reported all-time highs in total revenue and earnings per share, driven by exceptional iPhone demand and sustained growth in Services.

For the quarter ended December 27, 2025, Apple generated revenue of $143.8 billion, representing 16% year over year growth, while diluted EPS rose 19% year over year to $2.84, setting a new company record. Gross margin percentage reached 48.2%, translating into $69.2 billion in gross profit.

iPhone and Services Lead Growth

The standout performance came from iPhone, where revenue surged 23% year over year to $85.3 billion, fueled by unprecedented demand for the iPhone 17 lineup. Management noted record iPhone performance across every geographic region, highlighting robust global demand.

Services revenue reached a new all-time high of $30.0 billion, up 13.9% year over year, continuing to provide margin stability and recurring cash flow. Services now account for over 20% of total company revenue, reinforcing Apple’s transition toward a more diversified earnings base.

Other product categories were more mixed. Mac revenue declined 6.7% year over year, while Wearables, Home and Accessories fell 2% year over year. iPad revenue increased 6.2% year over year to $8.6 billion.

Geographic Strength, Led by Greater China

Regionally, Apple delivered broad-based growth, with particularly strong momentum in Greater China, where revenue surged 38% year over year to $25.5 billion. The Americas grew 11%, Europe increased nearly 13%, and Rest of Asia Pacific surged 18%, while Japan posted mid-single-digit growth.

The geographic breadth of Apple’s expansion underscores the incredible customer satisfaction for its products and services and the expanding installed base, which now exceeds 2.5 billion active devices worldwide.

Cash Flow and Capital Returns Remain Compelling

Operating income in Q1 FY26 rose to $50.9 billion, while net income increased to $42.1 billion. Apple generated nearly $54 billion in operating cash flow during the quarter and returned approximately $32 billion to shareholders, underscoring the company’s unmatched capital-return capacity. The board declared a $0.26 per share dividend, payable in February 2026. Research and development spending increased to $10.9 billion in Q1 FY26.

Outlook: Growth Continues, but Supply Tight

For fiscal Q2 2026, Apple expects total revenue to grow 13% to 16% year over year, with Services maintaining a similar growth pace to the December quarter. Gross margin is guided between 48% and 49%, and operating expenses are expected to be between $18.4 billion and $18.7 billion, driven by higher R&D.

CEO Tim Cook noted during Apple's earnings call that iPhone demand significantly exceeded expectations, exiting the December quarter with lean channel inventory and placing the company in “supply chase mode” to meet the very high levels of customer demand. He also said, "From a memory point of view, memory had a minimal impact on the Q1. We do expect it to be a bit more of an impact to the Q2. We don’t obviously provide outlooks beyond the current quarter, but we do continue to see market pricing for memory increasing significantly; as always, we’ll look at a range of options to deal with that.”

Strategic AI Partnership with Google

In January 2026, Apple announced a multi-year collaboration with Google to leverage Gemini models and cloud infrastructure as the foundation for next-generation Apple Foundation Models. This partnership is expected to power future Apple Intelligence features, including a more personalized Siri, while maintaining Apple’s on-device processing and privacy standards.

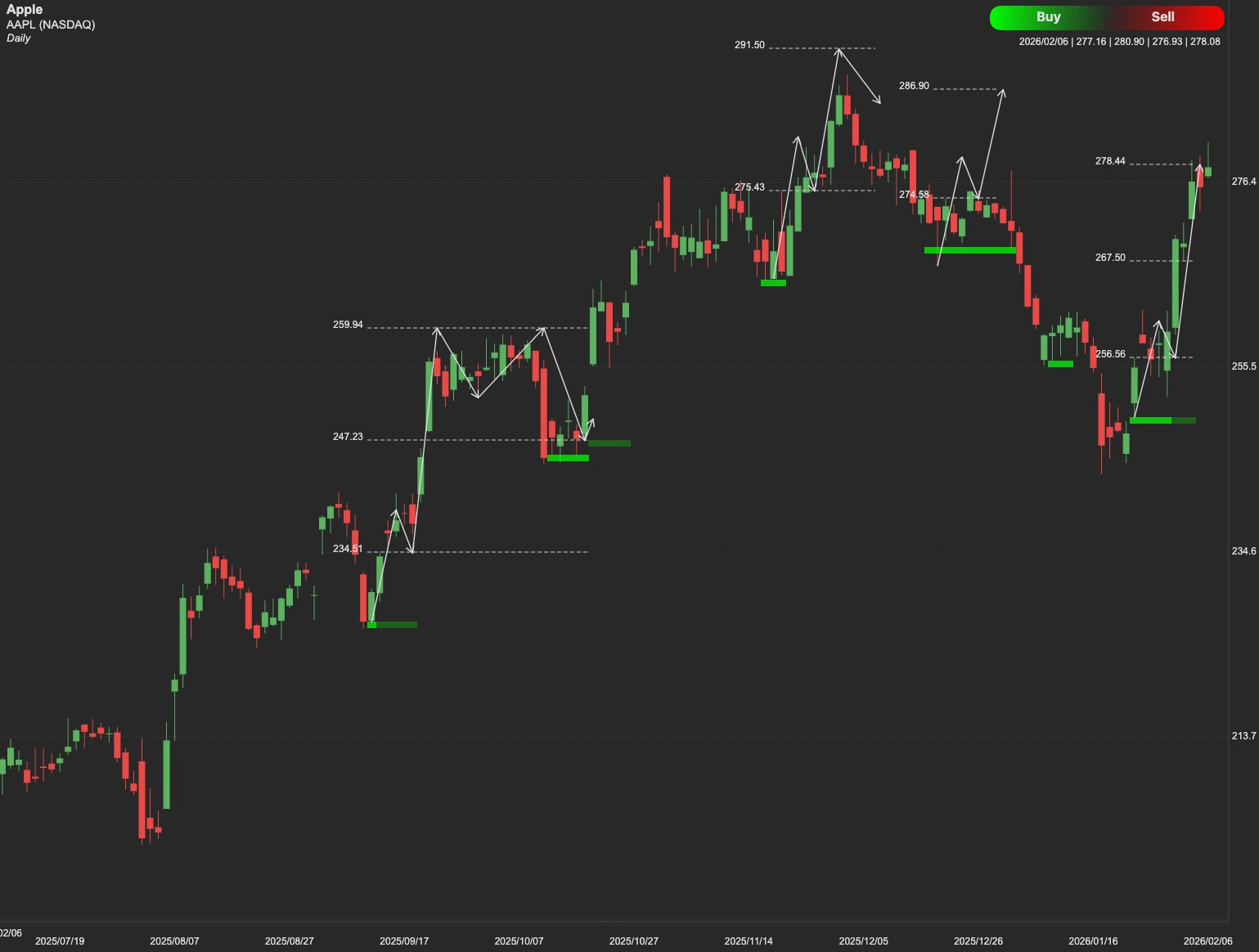

AAPL Stock Outlook

From a technical perspective, the $278 level is a critical near-term resistance. A sustained move and consolidation above this level could open the path toward the $296 upside target.

Conversely, failure to hold above resistance may lead to a pullback toward initial support near $236, with a deeper downside support zone around $223. These levels remain important reference points for risk management amid broader market volatility.