Cintas Corporation Stock Analysis: Strong Fundamentals, but Technical Pressure Persists

Cintas Corporation (Nasdaq: CTAS) recently reported its fiscal 2026 third-quarter results, showcasing a business that continues to execute at an elite level. Despite record revenues and all-time high gross margin, the stock has declined approximately 16.5% since the March 11 announcement of its acquisition of UniFirst Corporation. Investors are currently weighing record-breaking internal metrics against a shifting technical landscape and a massive pending acquisition.

Financial Performance Highlights

Cintas delivered a strong quarter, with revenue rising to $2.84 billion, up 8.9% year-over-year, supported by 8.2% organic revenue growth. Profitability remained robust, as net income increased 8.4% to $502.5 million and diluted earnings per share climbed 9.7% to $1.24. Gross margin reached a record 51.0%, compared to 50.6% in last year's third quarter, an increase of 40 basis points.

Operating income also showed solid growth, increasing 8.2% to $659.9 million compared to $609.9 million in the same quarter last year. However, operating margin slightly declined to 23.2% from 23.4% a year ago. This modest contraction is partly explained by the prior-year period benefiting from a $15.0 million gain related to the sale of property and equipment, which was recorded within selling and administrative expenses.

Free cash flow generation also remained robust at $1.27 billion for the first nine months of fiscal 2026, enabling significant shareholder returns totaling $1.45 billion through dividends and buybacks. Cash and cash equivalents totaled $183 million at the end of February 28, 2026.

CEO Todd M. Schneider pointed to investments in technology, capacity and talent as the primary drivers. Management reinforced confidence by raising full-year guidance, now expecting revenue between $11.21 billion and $11.24 billion and adjusted diluted EPS of $4.86 to $4.90. The adjusted EPS guide does not include the impact of non-recurring transaction expenses related to the UniFirst acquisition. Transaction costs related to the UniFirst acquisition incurred during fiscal year 2026 are estimated to have an impact on diluted EPS in a range of $0.03 to $0.04.

The UniFirst Acquisition: A $5.5 Billion Move

Cintas has agreed to acquire UniFirst in a transaction valued at approximately $5.5 billion in enterprise value, structured as a mix of cash and stock. The cash portion of the deal will be funded through: Existing cash reserves, Committed credit facilities, and fully underwritten bridge financing from major banks. The deal is expected to expand Cintas’ scale, route networks, and service capabilities across North America.

Management projects approximately $375 million in operating cost synergies within four years, with the transaction becoming accretive to Cintas’ earnings per share by the end of the second full year after closing. The combined entity will serve roughly 1.5 million business customers, strengthening its competitive position in a large, growing industry.

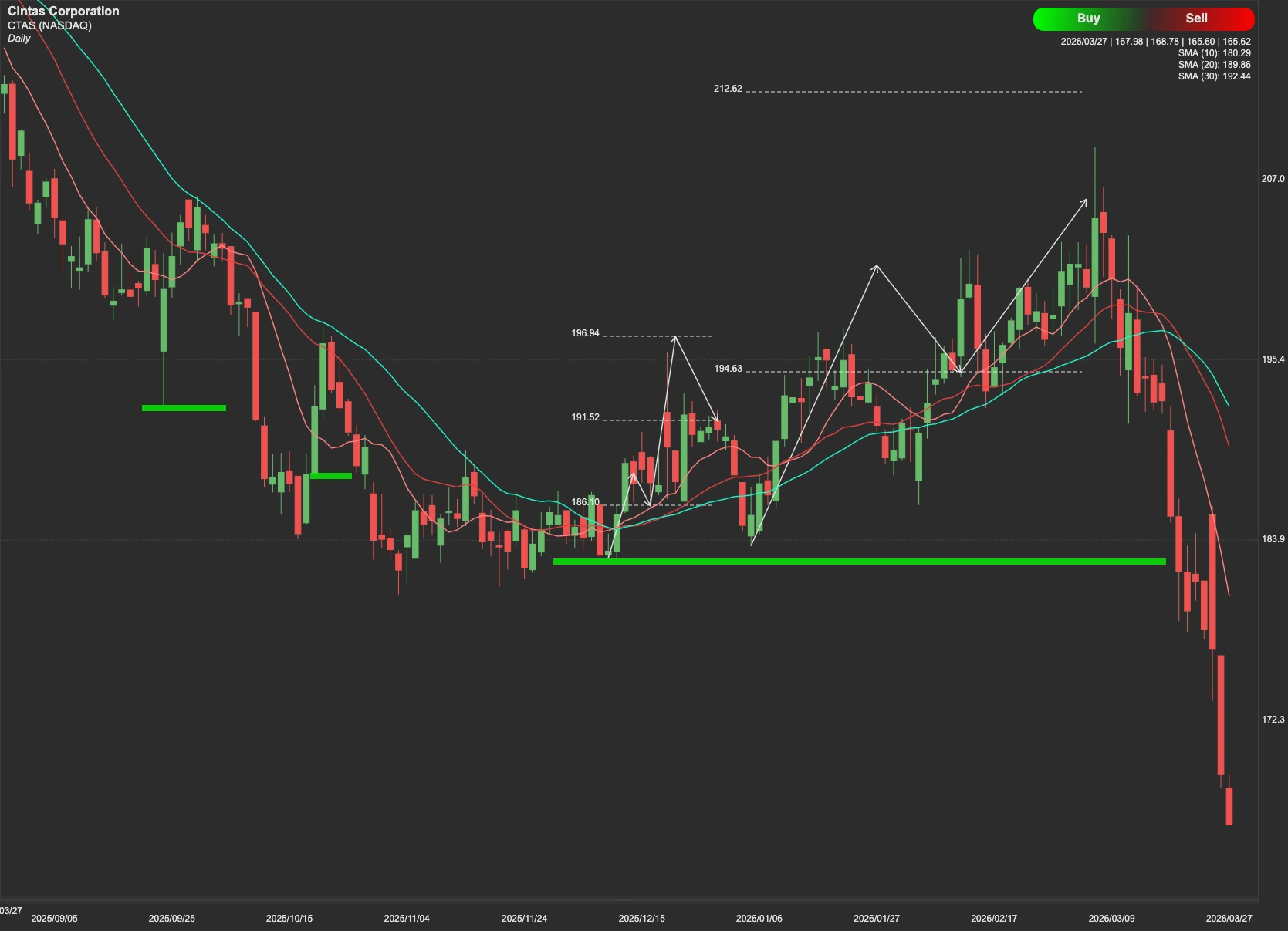

Technical Analysis: Key Levels to Watch

The CTAS stock has declined significantly since the acquisition announcement. To reverse the current bearish sentiment, the stock must overcome key resistance levels to confirm a sustained upward trend.

Key Resistance ($189): This is the immediate and most critical hurdle.

Secondary Resistance ($212): If the stock reclaims and holds above the $189 resistance level, it will face the next major upside barrier at $212.

Conversely, if the stock fails to breach the $189 resistance, it may continue to seek lower liquidity zones to find buyers.

Initial Support ($141): A failure at resistance could lead the stock to test the $141 floor.

Deep Support ($120-$108): In a more severe bearish scenario, the stock may retreat to the $120-$108 range to establish a long-term base.