CMC Delivers Record Q1 2026 Results: Strategic Growth and Technical Outlook

Commercial Metals Company (NYSE: CMC) kicked off fiscal 2026 with a powerful performance, reporting first-quarter financial results that far exceeded the prior year's levels. Bolstered by the successful launch of the Transform, Advance, and Grow (“TAG”) program and significant expansion in the precast concrete market, the company’s strategic shift is beginning to reflect clearly in its financial profile.

Q1 Fiscal 2026: Financial Highlights

CMC reported first-quarter net earnings of $177.3 million, or $1.58 per diluted share, compared with a net loss in the prior year period that was weighed down by litigation charges. On an adjusted basis, first quarter earnings were $206.2 million, or $1.84 per diluted share, more than doubling year over year.

Net sales rose to $2.1 billion, supported by stable demand and expanding margins across North America Steel Group and Construction Solutions Group. Most notably, consolidated core EBITDA surged 52% year over year to $316.9 million, pushing the core EBITDA margin to 14.9%.

North America Drives the Upside

The North America Steel Group remained the primary earnings engine. Adjusted EBITDA climbed nearly 58% year over year to $293.9 million, with the adjusted EBITDA margin expanding to 17.7%, driven by higher margins over scrap costs on steel products as well as positive contributions from CMC’s TAG program. Steel product metal margins reached their strongest point in almost three years, supported by favorable market dynamics.

CMC’s enhanced commercial discipline—prioritizing margin quality over volume—has started to pay off, with downstream backlog pricing trending higher for two consecutive quarters.

Construction Solutions Adds a New Growth Layer

The newly renamed Construction Solutions Group (CSG) delivered its best first-quarter performance on record. Adjusted EBITDA jumped 74.7% year over year to $39.6 million, with an adjusted EBITDA margin of 20%. Strength at Tensar, combined with improving efficiency across construction services, highlights the segment’s growing profitability.

Looking ahead, the acquisitions of CP&P and Foley, closed in December, establish a sizable precast concrete platform. Management expects these businesses to contribute $165–$175 million in EBITDA during fiscal 2026, reinforcing CMC’s longer-term growth profile.

Europe Remains the Weak Spot

The Europe Steel Group faced softer pricing and margin pressure from imports and a lower CO₂ credit. While adjusted EBITDA declined year over year, underlying operating performance improved when excluding energy rebate timing effects. Management sees margin recovery potential later in fiscal 2026 as Carbon Border Adjustment Mechanism (CBAM) regulations take full effect.

Balance Sheet Strength Supports the Strategy

CMC ended the quarter with $3.0 billion in cash, cash equivalents and restricted cash, providing flexibility to fund acquisitions, dividends, and share repurchases. The company bought back nearly $39 million of stock during the quarter and extended its dividend streak to 245 consecutive quarterly payments, underscoring shareholder-return discipline.

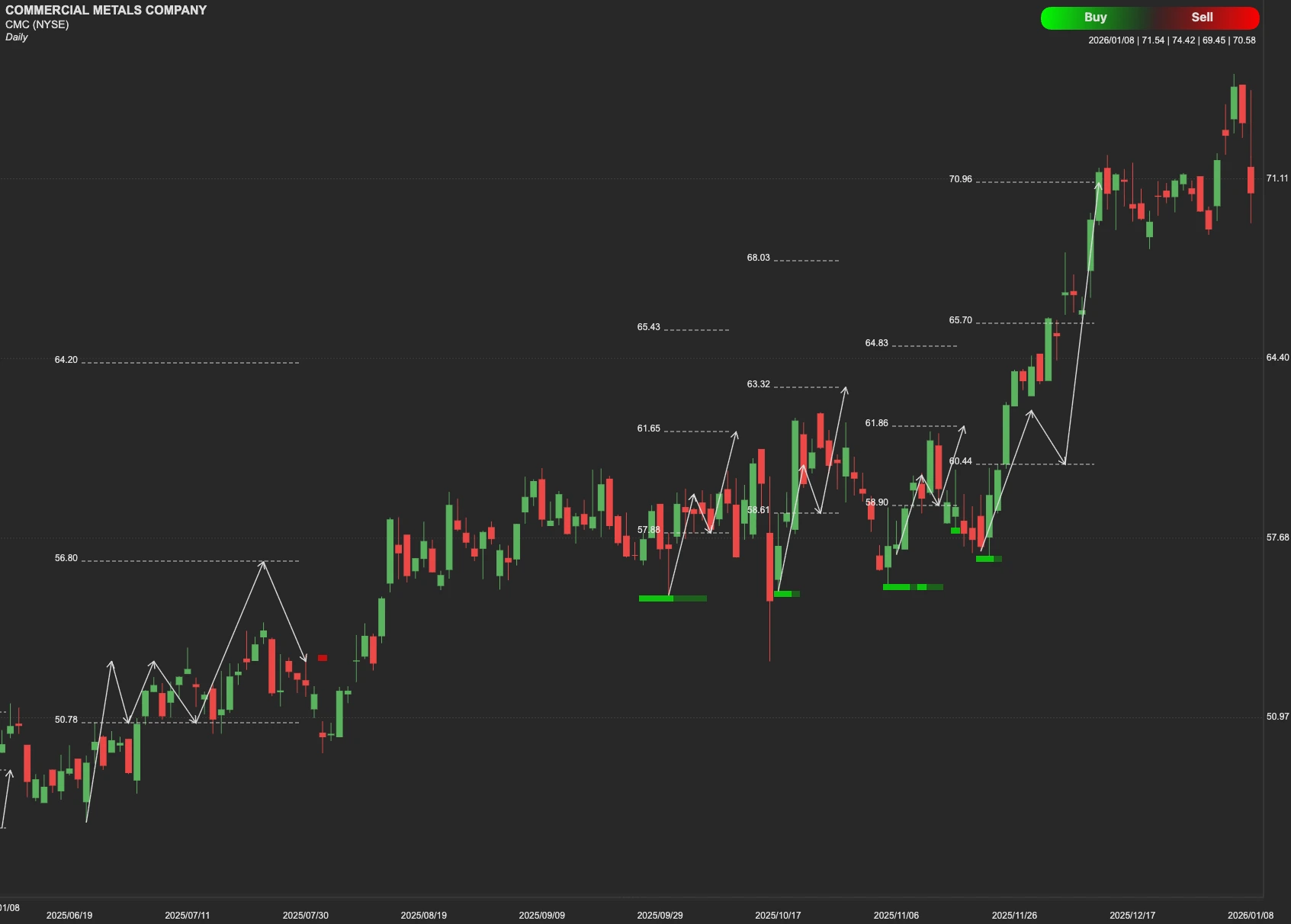

Technical Outlook

From a technical perspective, $79 is the key resistance level for CMC stock. If the stock holds above $79, momentum could carry shares toward the next upside target near $88.

Should the stock fail to overcome $79, a retracement is likely. The primary support zone to watch is $59. If selling pressure intensifies and breaks this floor, the stock may seek deeper support in the $53 - $44 range.