Darden Restaurants Stock Analysis: Strong Earnings, Expanded margin, and Rising Shareholder Returns

Darden Restaurants, Inc. (NYSE: DRI) delivered a strong finish to fiscal 2026, reporting better-than-industry sales growth, expanding margins, robust free cash flow, and a shareholder-friendly capital allocation strategy.

Strong Fourth Quarter Driven by Sales Growth and Margin Expansion

For the fiscal fourth quarter ended May 31, 2026, Darden generated revenue of $3.72 billion, up 13.7% year over year. The increase was supported by an additional week of operations, 4.6% blended same-restaurant sales growth, and contributions from 43 net new restaurant openings.

Performance remained broad-based across the company's brands. Olive Garden posted 2.4% same-restaurant sales growth, while LongHorn Steakhouse continued to outperform with an impressive 9.5% increase. Fine Dining and Other Business segments also reported positive same-restaurant sales growth.

Operating leverage was another highlight. Operating income climbed to $516.8 million, up from $382.8 million a year ago, while operating margin expanded to 13.9% from 11.7%.

Earnings from continuing operations increased to $407.8 million, compared with $304.0 million in the prior year. Reported diluted EPS from continuing operations reached $3.54, while adjusted EPS from continuing operations, excluding primarily restaurant closure costs and Chuy's integration expenses, rose 22.8% year over year to $3.66. Management noted that the extra operating week contributed approximately $0.25 to both reported and adjusted diluted EPS.

Capital allocation remains one of Darden's key strengths. Alongside the quarterly dividend increase to $1.62 per share, management introduced a new $1.5 billion share repurchase authorization with no expiration date. During the fourth quarter, the company repurchased approximately $138 million of common stock.

Fiscal 2026 Demonstrates Consistent Execution

For the full fiscal year, Darden generated $13.21 billion in revenue, representing 9.4% growth from fiscal 2025. Revenue growth was fueled by 4.5% blended same-restaurant sales growth, contributions from new restaurants, and the additional operating week.

Annual same-restaurant sales remained healthy across the portfolio:

- Olive Garden: +4.0%

- LongHorn Steakhouse: +7.2%

- Fine Dining: +1.2%

- Other Business: +3.9%

Reported diluted EPS from continuing operations reached $10.44, while adjusted EPS from continuing operations increased 11.4% to $10.64.

Cash Flow and Balance Sheet

Darden continued to produce significant cash generation during fiscal 2026. Net cash provided by operating activities reached $1.85 billion, while capital expenditures totaled $734 million, resulting in free cash flow of approximately $1.12 billion. Management emphasized that consistent cash flow generation continues to comfortably fund restaurant expansion, dividend growth, and ongoing share repurchases.

At fiscal year-end, Darden held $219.5 million in cash and cash equivalents. Total debt stood at $2.38 billion.

Fiscal 2027 Outlook Signals Continued Growth

Looking ahead, Darden expects another year of steady expansion. Fiscal 2027 guidance calls for total sales between $13.60 billion and $13.75 billion, same-restaurant sales growth of 2.5% to 3.5%, EBITDA of $2.26 to $2.29 billion, and diluted earnings per share from continuing operations between $11.10 and $11.35. Target of 75 to 80 new restaurant openings, backed by approximately $875 million in total capital spending.

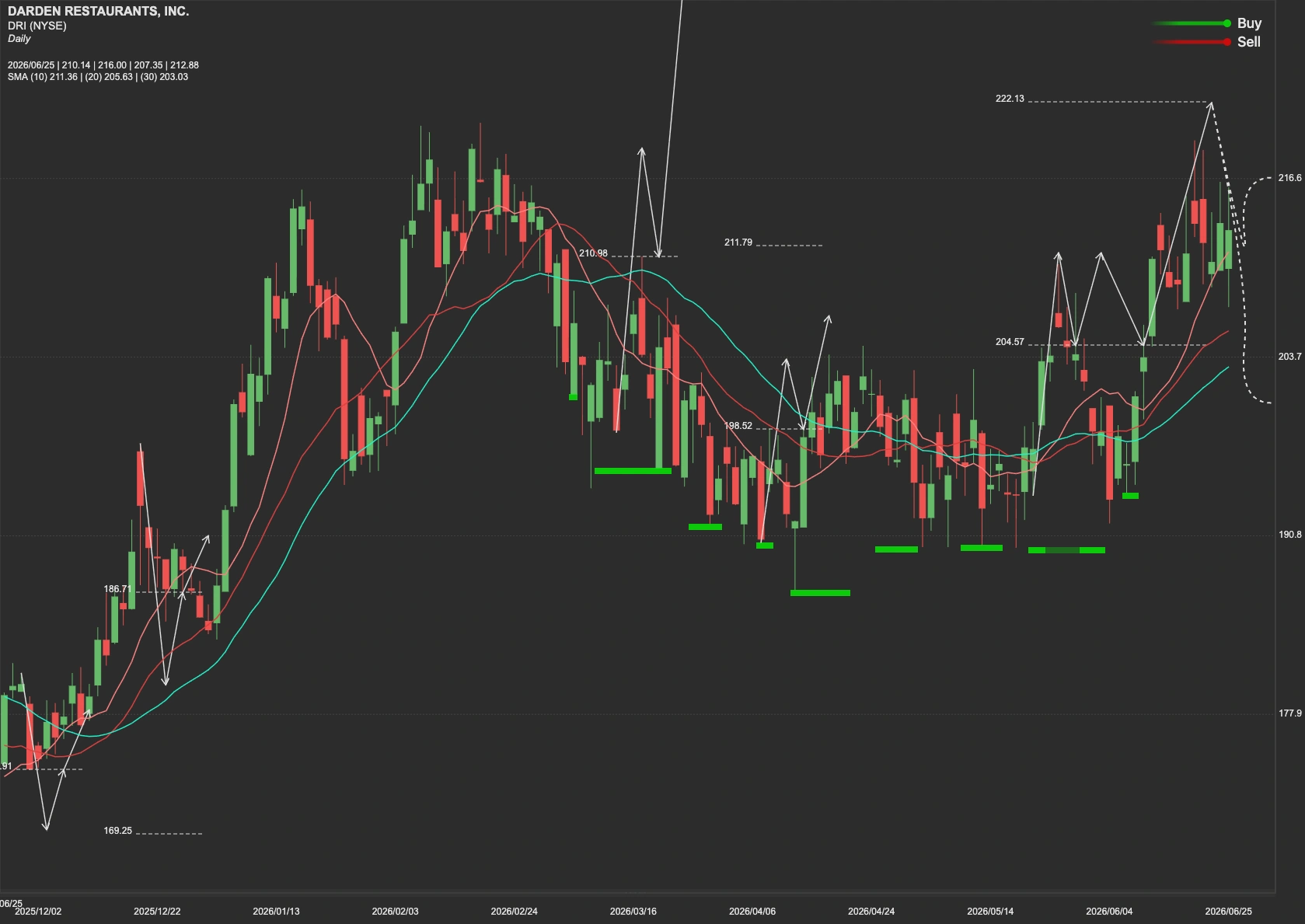

DRI Stock Technical Analysis

From a technical perspective, the key resistance level sits at $232 for DRI stock. A decisive breakout and sustained move above this level could open the door for the next upside target near $249.

However, if the stock is unable to overcome the $232 resistance, investors should watch for a potential pullback toward the first major support level around $188. Should selling pressure intensify, the next significant support lies near $162.