Deere & Company Stock Analysis: Analyzing Resilience as the Ag Cycle Bottoms

Deere & Company (DE) just released its financial results for the fourth quarter and full fiscal year ended November 2, 2025, painting a complex picture of a company navigating a severe cyclical downturn with strong operational efficiency. While full-year earnings saw a significant contraction, management’s forward guidance is strategically positioning 2026 as the bottom of the current large agricultural (ag) cycle.

The Financial Results: Resilience and the Bottoming Cycle

For the fourth quarter ended November 2, 2025, Deere posted net income of $1.065 billion, down 14% year over year from $1.245 billion. Fully diluted EPS declined to $3.93 from $4.55 a year earlier.

On a full-year basis, fiscal 2025 net income dropped 29% to $5.027 billion, compared with $7.1 billion in fiscal 2024, reflecting the market's difficult conditions.

Despite lower profits, quarterly revenue showed resilience. Worldwide net sales and revenues rose 11% to $12.394 billion in Q4, indicating effective price realization and volume management despite headwinds.

The core message from CEO John May is clear: 2026 is the year the cycle turns. The company forecasts fiscal 2026 net income to be in the range of $4.00 billion to $4.75 billion. This guidance, which suggests a further contraction, reinforces management’s expectation that 2026 will "mark the bottom of the large ag cycle," setting the stage for potential future recovery.

Q4 2025 Segment Performance

The segment results clearly show Deere’s diversification at work:

Construction & Forestry (CF)—The Growth Engine: This segment was the standout performer. Revenue surged 27%, while operating profit increased 6% to $348 million, driven by shipment volumes and favorable product mix.

Production & Precision Agriculture (PPA)—Cost Pressure: Revenue rose 10% to $4.74 billion, but operating profit fell 8%. This contraction highlights the pressure from "higher production costs, higher tariffs, and special items," impacting margins despite higher shipment volumes.

Small Agriculture & Turf (SAT)—Margin Squeeze: Revenue grew 7% to $2.46 billion, but operating profit collapsed 89%, driven by high tariffs, warranty expenses, and production costs, pushing the operating margin down to a thin 1.0%.

Financial Services (FS)—Steady Support: Net income from Financial Services was up a significant 69% to $293 million for the quarter, largely due to favorable financing spreads and lower credit loss provisions.

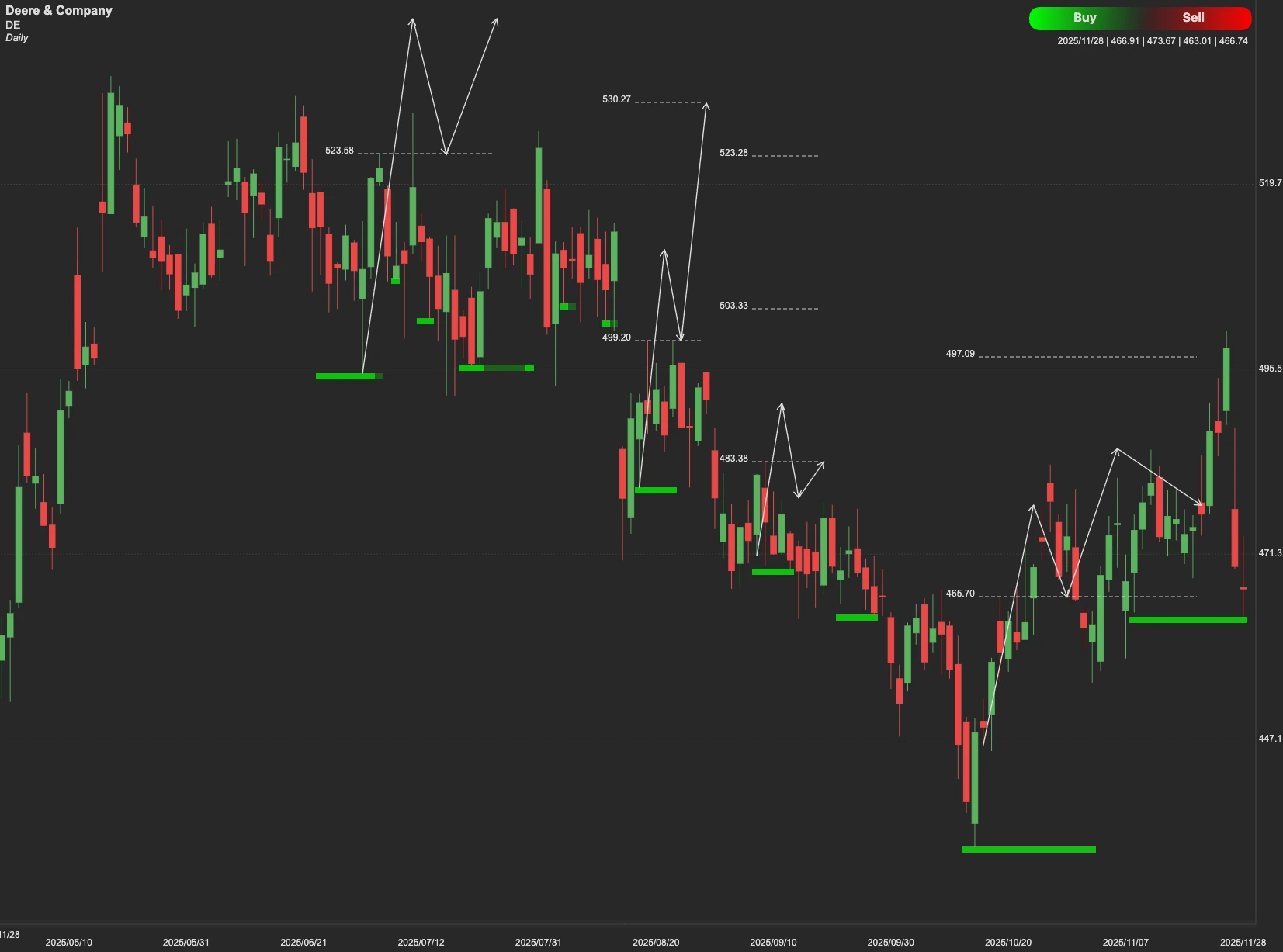

Technical Outlook

From a technical perspective, the stock is currently confronting a pivotal decision point. The $500 level acts as the immediate and crucial resistance. If DE stock can firmly hold above the $500 resistance, the next technical target is identified at $527.

Should the stock fail to overcome $500, it may fall back to seek support. The immediate support level is $432. A breach of $432 would signal deeper technical weakness, potentially leading the stock toward its further support at $381.