Dell Stock Analysis: AI Server Surge Powers Record Results

Dell Technologies (NYSE: DELL) continues its transformation into a major AI infrastructure player, as evidenced by its record-breaking financial results for the third quarter of fiscal 2026. The report, which highlighted robust earnings and raised forward guidance, provides a strong fundamental backdrop.

The Foundation: Record Earnings and AI Catalyst

Dell's Q3 FY26 performance was overwhelmingly strong, driven by the massive demand for its AI server.

Record Revenue and Earnings: Dell posted record third-quarter revenue of $27.0 billion (up 11% year-over-year) and non-GAAP diluted EPS of $2.59 (up 17% year-over-year). The company generated $1.2 billion in operating cash flow in Q3 and has produced $6.5 billion year-to-date. Adjusted free cash flow more than doubled versus last year.

Infrastructure Surge: The Infrastructure Solutions Group (ISG) saw record revenue of $14.1 billion, surging 24% year-over-year. The core Servers and Networking revenue was particularly strong, up 37% to $10.1 billion. Storage revenue was down 1% to $4.0 billion.

AI Backlog & Guidance Raise: The most compelling data point is the accelerating AI momentum. Dell booked $12.3 billion in AI server orders in Q3 alone, bringing the year-to-date total to an unprecedented $30 billion. AI shipments of $5.6 billion leading to $15.6 billion of shipments year-to-date. This massive demand has resulted in an exiting Q3 AI backlog of $18.4 billion. Management is confidently raising its full-year FY26 AI server shipment guidance to roughly $25 billion (up over 150% year-over-year). The total full-year revenue guidance was also raised to between $111.2 billion and $112.2 billion, up 17% year over year at the midpoint of $111.7 billion.

Client Solutions Group (CSG): The Client Solutions Group also showed stability, with total revenue up 3% to $12.5 billion, primarily driven by the Commercial segment (up 5%), partially offset by continued weakness in consumer demand (down 7%).

Capital Returns and Balance Sheet Pressure

Shareholder returns remain aggressive. The company returned $1.6 billion in Q3 alone via buybacks and dividends, bringing year-to-date capital returns to $5.3 billion, including the repurchase of more than 39 million shares. Total liabilities exceed assets, and net debt remains elevated.

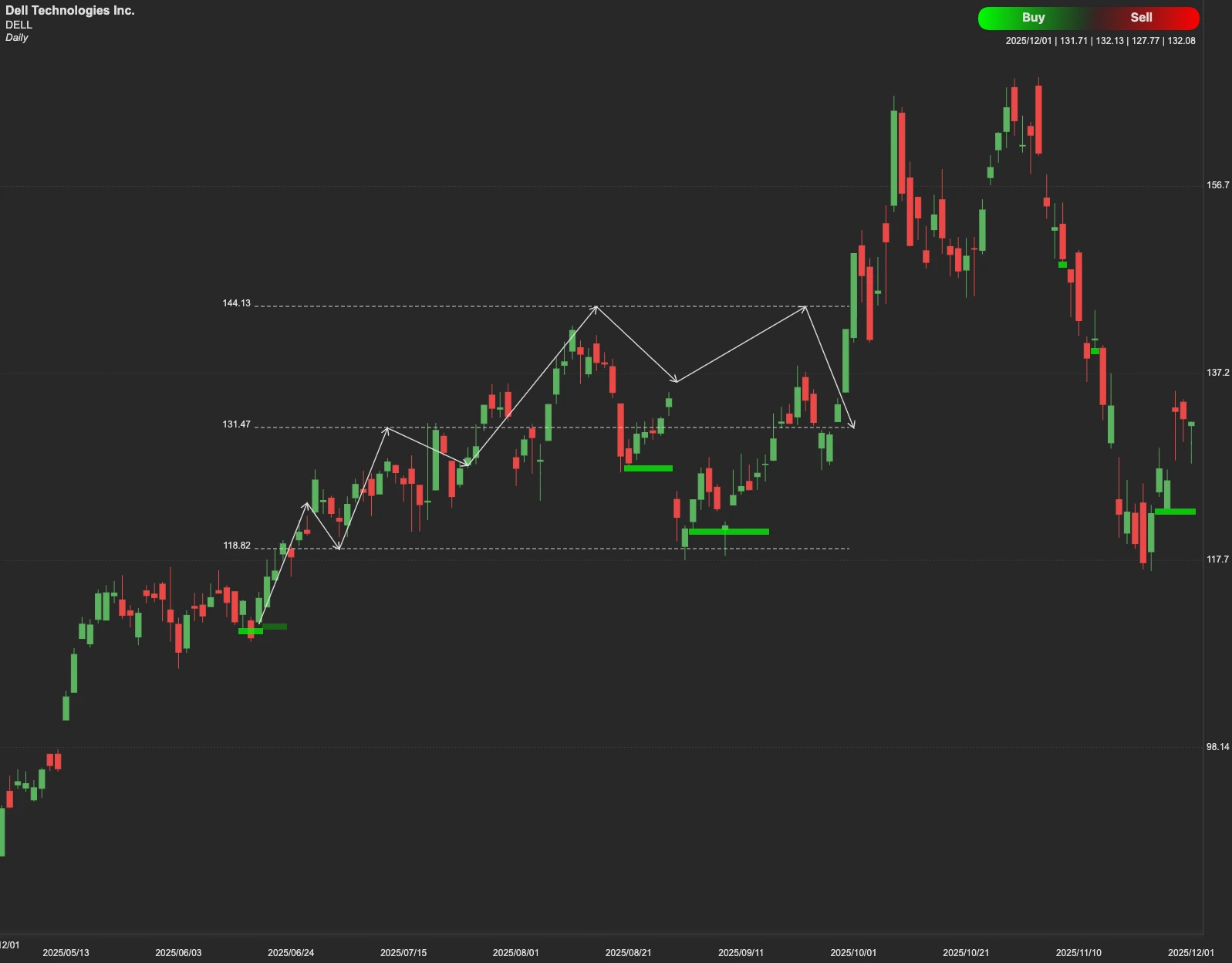

Technical Outlook

Despite the strong fundamentals, the stock has experienced volatility, retreating from its prior highs. Currently, for bulls, the immediate challenge is breaking the $150 resistance level. If the stock holds above $150, the next upside target is $168, a level that could be reached quickly if AI momentum continues and market sentiment remains favorable.

On the other hand, a rejection near $150 could trigger a pullback toward initial support at $116. A decisive break below the $116 support could indicate a deeper correction, potentially leading the stock to seek the $101 level.