Disney Stock Analysis: AI Innovation and Earnings Growth

The Walt Disney Company (NYSE: DIS) delivered a markedly improved financial performance in fiscal 2025, underscored by strong earnings growth, expanding operating income, and renewed capital return commitments, although near-term segment results showed some mixed dynamics. Following a robust Fiscal 2025 performance, Disney announced a landmark three-year agreement with OpenAI on December 11, 2025.

Fundamental Performance Overview

Disney delivered a mixed but constructive fourth quarter. Revenue in Q4 of $22,464 million, down $110 million compared to $22,574 million in Q4 fiscal 2024. Income before income taxes for Q4 increased to $2.0 billion from $0.9 billion in Q4 fiscal 2024, as the company significantly reduced its restructuring and impairment charges. For Q4, these charges dropped to $382 million, down from $1,543 million in Q4 fiscal 2024. Total segment operating income decreased 5% for Q4 to $3.5 billion from $3.7 billion in Q4 fiscal 2024. Diluted earnings per share (EPS) for Q4 increased to $0.73 from $0.25 in Q4 fiscal 2024. Adjusted EPS decreased 3% for Q4 to $1.11 from $1.14 in Q4 fiscal 2024.

Full-year results underscored a meaningful recovery in earnings power. Fiscal 2025 revenue increased 3% year over year to $94.4 billion, from $91.4 billion in the prior year. Income before taxes surged 59% to $12.0 billion, reflecting operating leverage and significantly lower restructuring charges. For the full year, restructuring and impairment charges dropped to $819 million, down from $3.60 billion in fiscal 2024. Total segment operating income increased 12% for the year to $17.6 billion from $15.6 billion in the prior year. For the year, diluted EPS increased to $6.85 from $2.72 in fiscal 2024, and adjusted EPS increased 19% to $5.93 from $4.97 in fiscal 2024.

Segment Analysis

Entertainment: Full-year operating income climbed 19% to $4.7 billion, while Q4 operating income declined $376 million to $691 million compared to the prior-year quarter, driven by theatrical slate comparisons. Disney’s Direct-to-Consumer business posted a meaningful milestone with $352 million in Q4 operating income and nearly 196 million combined Disney+ and Hulu subscriptions.

Sports: Sports segment operating income grew 20% for the full year, with revenue of $17,672 million, up $53 million from $17,619 million in fiscal 2024. Q4 operating income was modestly lower year over year due to higher marketing and programming and production costs at ESPN. Advertising trends remained favorable, with domestic advertising revenue up 8% in Q4 2025.

Experiences: Experiences remained Disney’s primary earnings engine, generating a record $10.0 billion in operating income for the year. Both domestic and international parks delivered solid growth, reinforcing the segment’s pricing power and demand resilience. For Q4: International Parks & Experiences operating income grew 25% to $375 million; Domestic Parks & Experiences operating income grew 9% to $920 million.

Capital Allocation and Outlook

Disney ended fiscal 2025 with $18.1 billion in operating cash flow and announced a materially more shareholder-friendly capital return strategy. The company plans to double its share repurchase target to $7 billion, invest $24 billion in content across Entertainment and Sports, and pay a $1.50 per share cash dividend over fiscal 2026. Management also reaffirmed double-digit adjusted EPS growth targets for fiscal 2026 and fiscal 2027, signaling confidence in earnings durability.

Strategic Optionality: AI Partnership with OpenAI

Disney’s newly announced three-year licensing and strategic partnership with OpenAI adds a long-term optional growth lever. The agreement enables the use of Disney IP across Sora and ChatGPT Images, while positioning Disney as a major enterprise customer of OpenAI’s technology. The $1 billion equity investment in OpenAI underscores Disney’s intent to integrate generative AI into content creation, fan engagement, and Disney+ experiences.

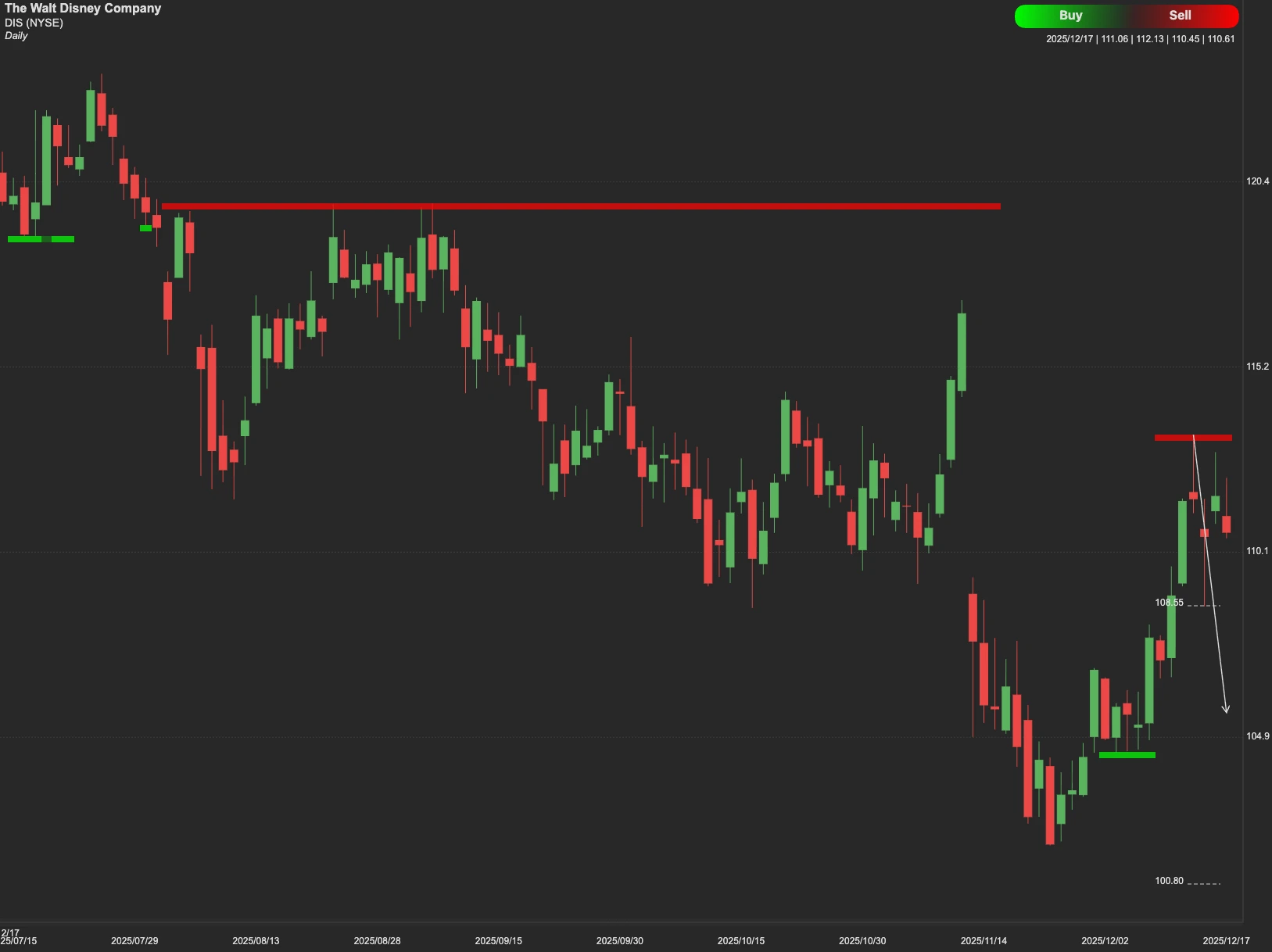

Technical Outlook for DIS Stock

From a technical perspective, $125 represents a critical resistance level for DIS shares. A sustained breakout and hold above $125 would signal improving market confidence and open the path toward the next upside target near $136.

Conversely, failure to maintain strength above $125 could result in renewed downside pressure. Initial downside support is located around $100, a psychologically and technically significant level. Should $100 fail to hold, the stock could seek its long-term floor near $80.