Dollar Tree: Multi-Price Strategy Drives Q3 Outperformance and Boosted Outlook

Dollar Tree, Inc. (NASDAQ: DLTR) delivered a powerful third-quarter fiscal 2025 performance, confirming that its strategic shift toward a multi-price point model is fundamentally transforming its profitability and market appeal.

Q3 2025: A Deep Dive into Operating Strength

The financial results for the quarter ended November 1, 2025 (reflecting continuing operations after the Family Dollar divestiture) were exceptionally strong:

Net Sales Growth: Net sales increased by a robust 9.4% to $4.7 billion.

EPS Beat: Adjusted diluted earnings per share (EPS) from continuing operations was $1.21, marking a significant 12.0% increase year-over-year.

Comps Driven by Ticket: Same-store net sales grew 4.2%, fueled entirely by a 4.5% increase in the average ticket. While traffic saw a slight 0.3% decline, the ability to successfully capture greater share-of-wallet from existing and new customers demonstrates pricing power.

Gross Margin Expansion: Gross profit increased 10.8% to $1.7 billion, expanding the gross margin by 40 basis points to 35.8%. This expansion was primarily driven by improved mark-on from pricing initiatives, lower freight costs, and favorable sales mix, partially offset by higher tariff costs, markdowns, and shrink.

Operating Margin Contraction: Despite gross margin improvement, the overall operating margin compressed. Operating income increased 3.8% to $343.3 million, but the operating margin decreased 40 basis points to 7.2%. On an adjusted basis, adjusted operating income increased 4.1% to $345.3 million, but the adjusted operating margin still decreased 30 basis points to 7.3%. The primary driver of operating margin contraction was elevated Selling, General and Administrative (SG&A) expenses. SG&A increased 140 basis points to 29.2% of total revenue.

The Multi-Price Driver

CEO Mike Creedon credited the "multi-price strategy" and the "Dollar Tree 3.0" format for the strong performance, including an "all-time record Halloween season." The conversion of approximately 646 stores to the 3.0 multi-price format during the quarter highlights the rapid deployment of this winning strategy.

The success lies in balancing the retailer's core value proposition (85% of assortment priced at $2 or less) with the introduction of high-quality, higher-priced goods. This approach successfully broadens the customer base, attracting not just value-focused households but also higher-income shoppers looking for convenience and discovery.

Outlook and Capital Return

Full-Year Raise: The full-year fiscal 2025 adjusted EPS from continuing operations was raised to a range of $5.60 to $5.80. Net sales guidance was also revised upwards to the range of $19.35 billion to $19.45 billion.

Strong Q4 Guidance: For the critical holiday quarter, the company expects net sales between $5.4 billion and $5.5 billion, with adjusted diluted EPS projected between $2.40 and $2.60.

Capital Return: Dollar Tree has completed $1.5 billion in share repurchases year-to-date, with $2.0 billion remaining under its current authorization.

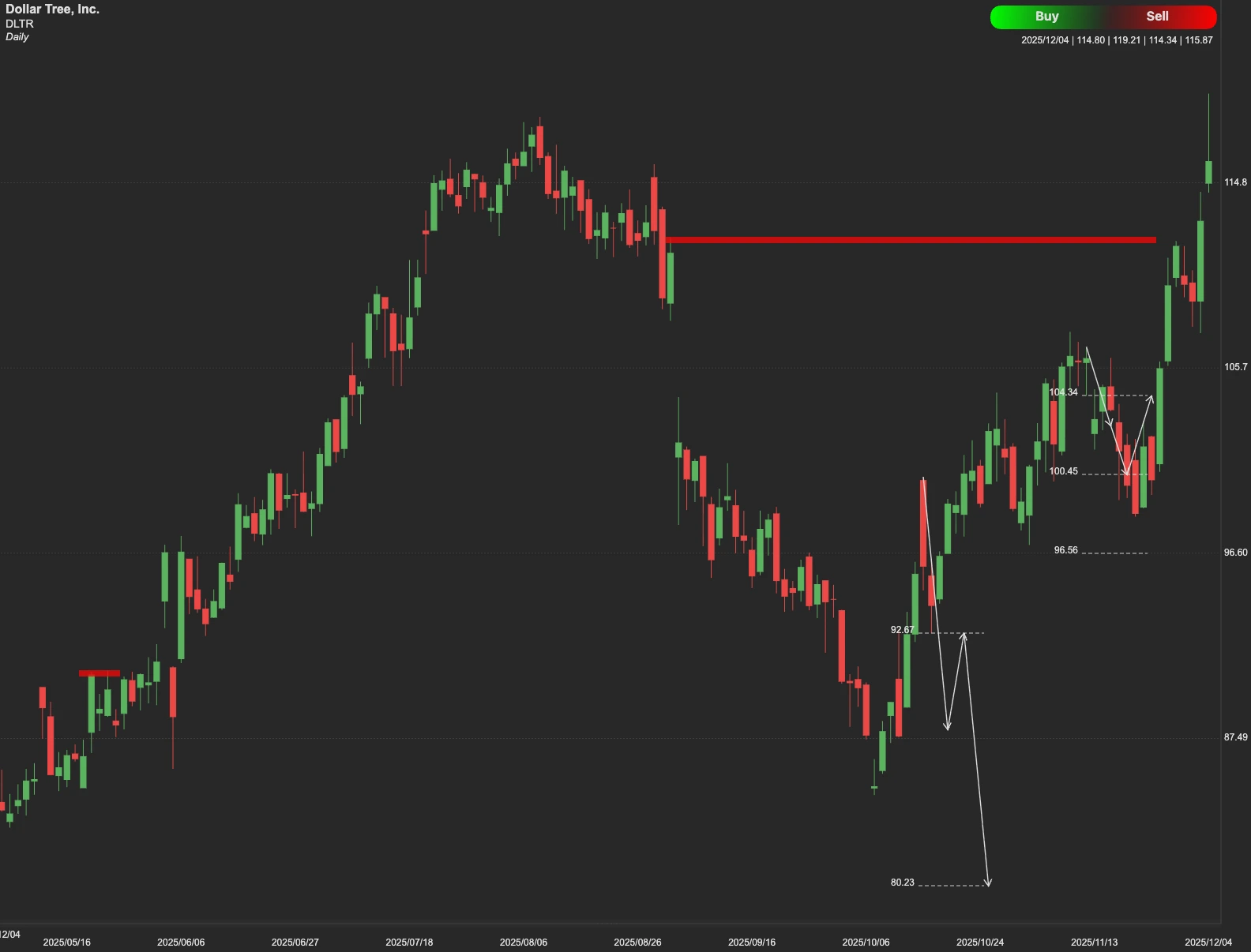

DLTR Stock Technical Analysis

While the fundamentals are clearly bullish, the stock must navigate key technical thresholds to continue its ascent.

The most immediate hurdle is the technical resistance level at $126. A sustained move and close above the $126 resistance would indicate strong buying momentum and potentially clear the path for the stock to test its next target of $138.

On the other hand, if the stock fails to break $126, the price is likely to seek the nearest major support level at $91. A break below $91 could see the price drop further to test the deeper technical support at $81.