Home Depot Stock Analysis: Resilient Results with Guidance Headwinds

The Home Depot (NYSE: HD) reported third-quarter fiscal 2025 results that underline both its resilience and the mounting pressures facing the U.S. home improvement market. While sales growth remained positive and market share continued to expand, the company missed expectations and subsequently lowered its full-year guidance.

Q3 Results: Modest Growth, Margin Pressure

For the third quarter of fiscal 2025, Home Depot reported total sales of $41.4 billion, a respectable 2.8% increase year-over-year. However, the core business showed signs of strain: comparable sales growth was a meager 0.2% overall, and just 0.1% in the critical U.S. market.

Net earnings for the quarter were $3.6 billion, resulting in a diluted EPS of $3.62, a slight decline from $3.67 in the same period last year, demonstrating that revenue growth was insufficient to outpace rising costs, particularly in selling, general, and administrative expenses (SG&A), which increased by 5.9% year-over-year.

CEO Ted Decker explicitly attributed the missed expectations to "the lack of storms in the third quarter," which resulted in greater than expected pressure in certain categories, and "consumer uncertainty and continued pressure in housing are disproportionately impacting home improvement demand."

The critical bright spot in the financials is the impact of the GMS Inc. acquisition, which contributed approximately $900 million in sales during the quarter.

Balance Sheet: Home Depot ended the quarter with $106.3 billion in total assets and $12.1 billion in shareholder equity, reflecting balance-sheet expansion driven by acquisitions. Total debt remains elevated, with short-term debt more than doubled, jumping from $1.34 billion to $3.2 billion, and current installments of long-term debt also increased from $3.2 billion to $6.5 billion.

Updated Fiscal 2025 Guidance: Growth Supported by GMS, EPS Under Pressure

Home Depot revised its full-year outlook to reflect ongoing demand challenges and the inclusion of GMS:

-

Total sales growth: ~3.0%

-

Comparable sales: slightly positive (52-week basis)

-

Adjusted operating margin: ~13.0%

-

Adjusted diluted EPS decline: ~5% year over year

Notably, much of the top-line growth depends on the $2.0 billion incremental contribution from GMS, while core organic growth remains muted. Management also pointed out continued fourth-quarter pressure due to the lack of storm activity, ongoing consumer uncertainty and housing pressure.

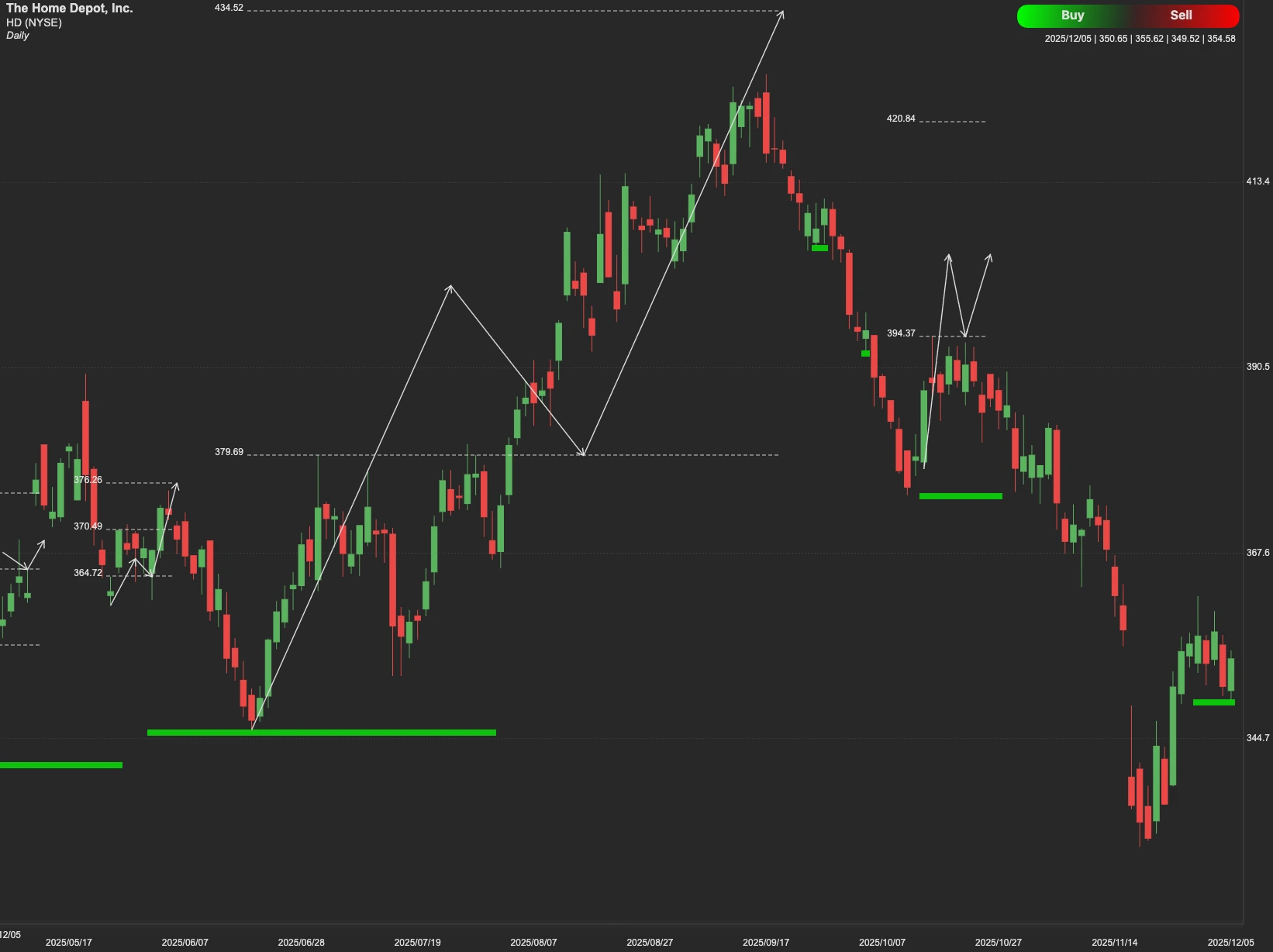

Technical Analysis

From a technical perspective, HD stock is currently facing stiff resistance at the $386 mark. If HD can hold above $386, momentum could build toward the next upside target near $406.

If the stock fails to break $386 and macroeconomic pressures continue to erode investor confidence in the revised guidance, HD may retreat to seek immediate support at $334. A sustained breakdown below $334 indicates serious selling pressure and could lead the stock to test the deeper, more critical support range between $300 and $280.