JPMorgan Chase Post-Earnings Analysis: Apple Card Integration and Resilient Growth

JPMorgan Chase & Co. (NYSE: JPM) closed out 2025 with a complex but fundamentally strong fourth-quarter performance. While headline net income dipped modestly year over year, the underlying earnings power, balance sheet strength, and diversified revenue streams continue to support a constructive long-term outlook for the stock.

Financial Performance: Resilient Earnings Despite One-Off Headwinds

For the fourth quarter of 2025, JPMorgan reported net income of $13.0 billion ($4.63 per share), showing a 7% decline compared to the previous year. The dip was largely tied to a strategic maneuver: the establishment of a $2.2 billion credit reserve for the upcoming acquisition of the Apple credit card portfolio. Excluding this significant item, adjusted net income reached $14.7 billion, or $5.23 per share, underscoring the firm's continued earnings power.

Full-year 2025 net income totaled $57.0 billion, down 2% year over year, with ROE of 17% and ROTCE of 20%, metrics that remain best-in-class among global banks. Revenue grew 3% year over year to $185.6 billion, supported by strong Markets performance, resilient net interest income, and accelerating asset management fees.

Segment Highlights: Broad-Based Strength Across the Franchise in Q4

Consumer & Community Banking (CCB): Despite a 19% drop in net income (largely due to the Apple Card reserve), consumer engagement remains high with active mobile customers up 7% year over year and debit and credit card sales volume up 7% year over year. Net revenue rose 6% to $19.4 billion, driven by customer growth, rising card volumes, and expanding wealth management relationships. Card Services net charge-off rate remained manageable at 3.14%.

Commercial & Investment Bank (CIB) posted a 4Q25 ROE of 19%, with net income up 10% year over year to $7.3 billion. Net revenue was $19.4 billion, up 10%, with payments revenue reaching a record $5.1 billion due to ongoing deposit and fee growth. Markets continued to benefit from demand for financing and robust client activity.

Asset & Wealth Management (AWM) continued to shine, generating a 44% ROE in 4Q25 and 40% for FY25. Revenue rose 13% in the quarter to a record $6.5 billion. Assets under management climbed to $4.8 trillion, up 18% year over year, and client assets were $7.1 trillion, fueled by strong net inflows and higher market levels.

Balance Sheet and Capital Return

The firm ended the quarter with a CET1 Capital Ratio of 14.5% (Standardized), $1.5 trillion in cash and marketable securities, and $564 billion in total loss-absorbing capacity. Book value per share rose 9% year over year to $126.99, while tangible book value per share increased 11% to $107.56.

The firm returned significant value to shareholders, repurchasing $7.9 billion in stock in Q4 alone and maintaining a solid dividend.

Strategic Outlook: The Apple Card Move

CEO Jamie Dimon highlighted the Apple Card partnership as a "patient and thoughtful deployment of excess capital." While the $2.2 billion reserve build pressured short-term EPS by $0.60, the move positions JPM to absorb a massive, digitally-native consumer base. This expansion comes as the U.S. consumer remains "resilient," even as the bank prepares for potential "sticky inflation" and geopolitical hazards in 2026.

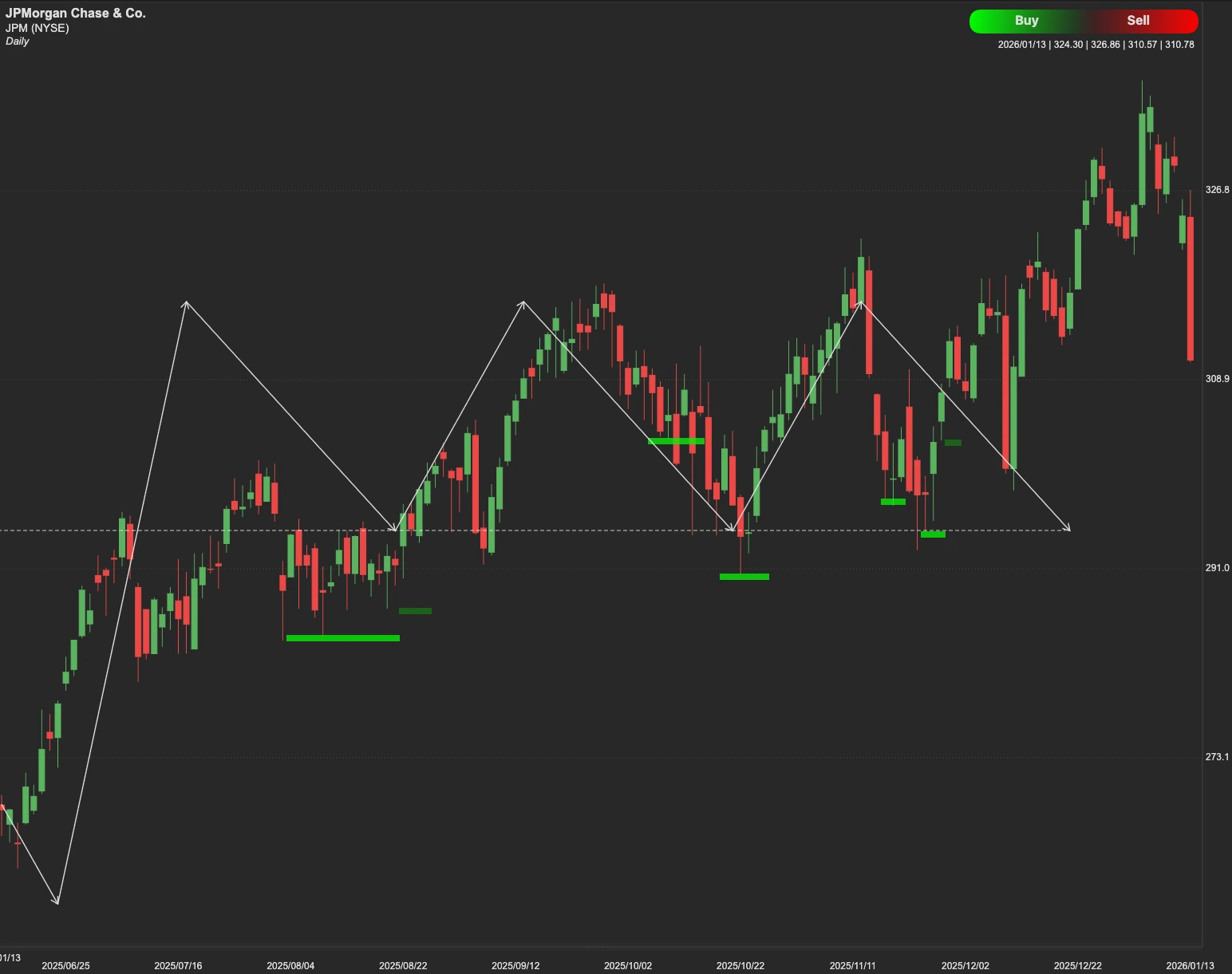

Technical Outlook

From a technical perspective, JPM stock faces a decisive resistance level at $334. This zone has acted as a ceiling in recent price action and represents a key psychological and technical hurdle.

A sustained move above $334 would signal strong buying conviction, opening a clear path toward the next major resistance and price target at $357. Conversely, failure to hold above $334 could lead to a pullback. In this case, the stock would likely seek support at $285, with a further potential decline to $262 if selling pressure intensifies.