JPMorgan Chase Stock Analysis: Resilient Growth Meets Global Uncertainty

JPMorgan Chase (NYSE: JPM) delivered a robust first-quarter 2026 performance, reinforcing its position as the industry leader across consumer banking, investment banking, and asset management. Net income rose to $16.5 billion, with EPS of $5.94, reflecting strong operating leverage and diversified revenue streams.

First-Quarter 2026 Fundamental Highlights

Revenue growth remained well-balanced. Total managed revenue increased 10% year-over-year to $50.5 billion. Net interest income excluding Markets rose 3% to $23.3 billion, supported by higher deposit balances, although partially offset by lower interest rates. Meanwhile, noninterest revenue excluding Markets increased 14% to $15.7 billion, driven by higher asset management fees, higher investment banking fees, higher auto operating lease income, and higher Payments fees. Notably, Markets revenue hit a record $11.6 billion, up 20%.

Noninterest Expenses rose 14% year-over-year to $26.9 billion, largely due to higher compensation and business investment.

From a profitability standpoint, the bank continues to operate at elite levels, with return on common equity (ROE) at 19% and return on tangible common equity (ROTCE) at 23%. Segment performance was particularly notable in Consumer & Community Banking (CCB) and Asset & Wealth Management (AWM), where ROEs reached 32% and 44%, respectively.

On the balance sheet side, JPMorgan remains exceptionally strong. CET1 capital stands at $291 billion, with standardized CET1 capital ratio of 14.3% and advanced CET1 capital ratio of 14.1%. The firm also holds $1.5 trillion in cash and marketable securities and $572 billion in total loss-absorbing capacity, underscoring its “fortress balance sheet” positioning. Book value per share was $128.38, up 8% year-over-year; tangible book value per share was $108.87, up 8%. Average loans grew 11% year-over-year to $1.5 trillion and average deposits up 7% to $2.6 trillion.

Credit quality appears stable. The provision for credit losses was $2.5 billion. Net charge-offs were $2.3 billion, essentially flat year-over-year, while net reserve builds remain modest.

The bank continues to generate significant shareholder returns, including $8.1 billion in buybacks and $4.1 billion in dividends during the quarter.

Segment performance

Segment performance was particularly impressive. The Commercial & Investment Bank remained a standout, delivering 30% net income growth and a 21% ROE, fueled by a sharp rebound in investment banking fees and robust Markets revenue. Asset & Wealth Management also showed strength, with assets under management rising 16% year over year to $4.8 trillion and client assets up 18% to $7.1 trillion. Consumer & Community Banking maintained stability, with net income rising 12% year over year to $5.0 billion, supported by a 7% increase in active mobile customers and robust card sales volume (up 9%), although credit costs remain an area to monitor, especially with card services net charge-off rate at 3.47%.

FY2026 Outlook

CEO Jamie Dimon emphasized that the U.S. economy remains resilient in the quarter, supported by continued consumer spending and healthy business activity. At the same time, the risks such as geopolitical tensions, energy price volatility, trade uncertainty, elevated asset prices, and large global fiscal deficits persist.

Management expects full-year 2026 net interest income of approximately $103 billion, or about $95 billion excluding Markets, both market dependent. Adjusted expenses are projected to reach around $105 billion, market dependent. Card Services NCO rate is expected to be around 3.4%.

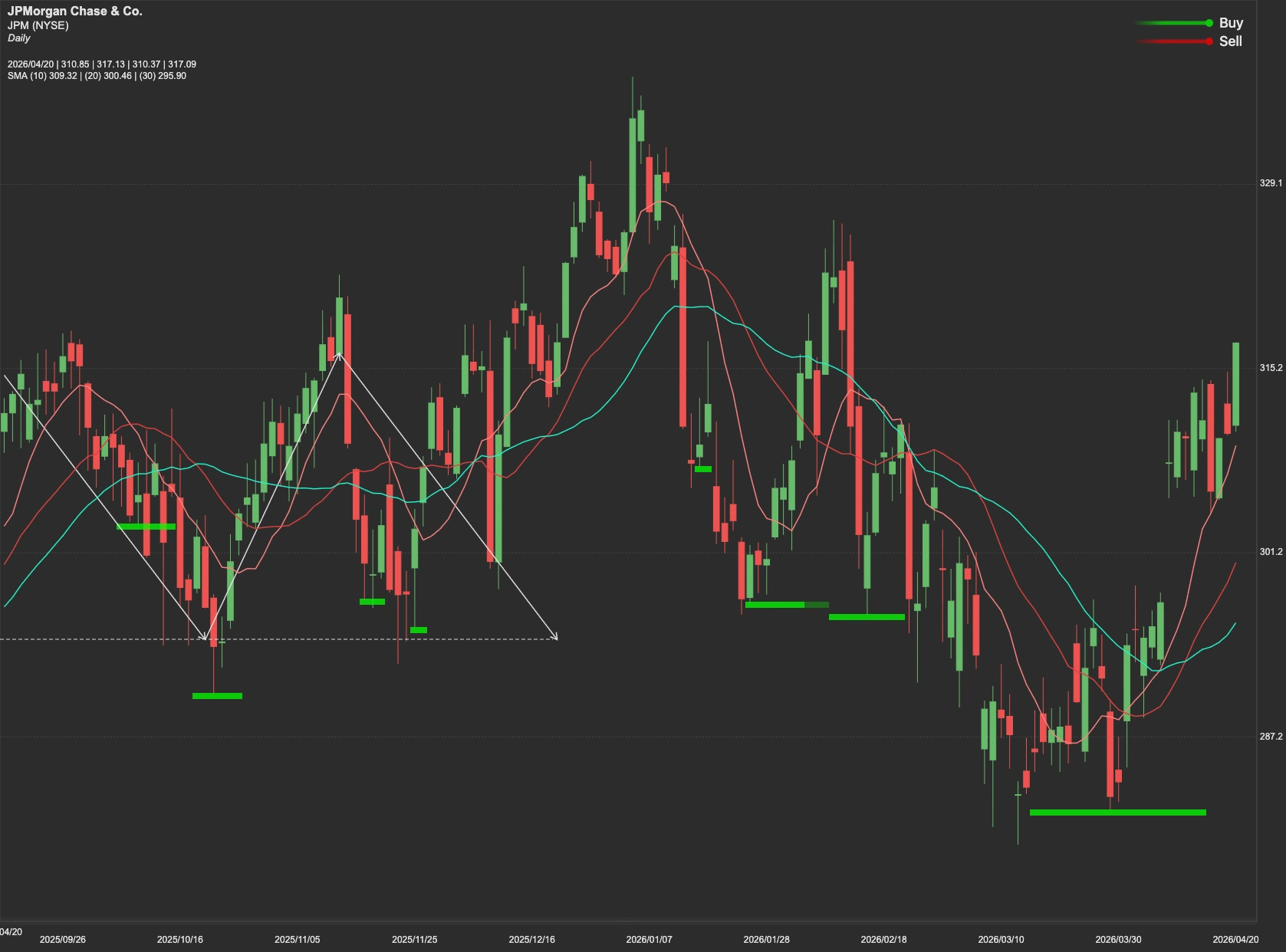

Technical Analysis

JPMorgan’s fundamentals remain best-in-class, characterized by strong profitability, diversified revenue streams, and a fortress balance sheet. Near-term stock direction will likely hinge on technical levels and external factors such as interest rate trends, capital regulation, and global economic conditions.

From a technical perspective, the immediate ceiling for JPM stock sits at $337. A sustained breakout above $337 could open the path toward the next target at $359, signaling continued bullish momentum supported by strong fundamentals and capital return policies, including dividends and share buybacks.

Conversely, failure to break resistance could trigger a pullback toward the $287 support level. A breakdown below this level would potentially drag the price down to the "deep value" support zone at $261.