Lamb Weston Q3 FY2026: Strategic Shifts Amidst Market Pressure

Lamb Weston Holdings, Inc. (NYSE: LW) released its third-quarter fiscal 2026 results on April 1, 2026, revealing a complex financial landscape. Despite successfully raising the midpoints of Fiscal Year 2026 net sales outlook, the quarter was marked by significant bottom-line contraction and mounting international headwinds.

Financial Performance and Operational Challenges

For the third quarter, Lamb Weston reported net sales of $1,564.8 million, a 3% increase year-over-year. However, this growth was largely supported by favorable foreign currency impacts; at constant currency, sales remained essentially flat. Volume grew by 7%, driven by strong performance and customer wins in North America, but this was entirely offset by a 7% decline in price/mix, reflecting continued price and trade support for customers and consumer shifts toward value-oriented channels and brands.

Gross profit declined $90.9 million versus the prior year quarter to $331.6 million, with gross margin declining sharply from 27.8% to 21.2%, driven by unfavorable global price/mix and inflationary pressures across key inputs. A notable contributor was a $32.5 million write-off of excess raw potatoes in the International segment, which highlights the mismatch between supply and softer-than-expected demand. In addition, underutilized production capacity, particularly in international markets, led to higher fixed cost absorption, further pressuring margins.

Operating income fell 49% to $126.6 million compared to the prior year quarter, while net income declined 63% year over year to $54 million. Adjusted EBITDA dropped 27% year over year to $271.7 million.

Segment Divergence: North America vs. International

North America continues to provide relative stability, with revenue increasing 5% and volumes rising 12%, supported by customer contract wins, share gains and growth. Even so, profitability in this segment declined as pricing pressure and a shift toward lower-margin channels offset operational efficiencies and cost savings.

The International segment, by contrast, remains a significant drag on overall performance. Sales declined 1% on a reported basis and 9% in constant currency, while adjusted EBITDA dropped sharply to $18.5 million. To improve utilization and respond to the challenging operating environment in the International segment, the company closed its Munro, Argentina plant during the third quarter and consolidated Latin America production into its new, modern facility in Mar del Plata, Argentina.

Cash flow and Capital Allocation

Cash flow performance improved, with operating cash flow rising to $595.6 million for the first three quarters of fiscal 2026. This increase was primarily driven by favorable working capital movements rather than stronger profitability. Capital expenditures declined significantly to $256.6 million, reflecting the completion of major growth initiatives and a strategic shift toward reducing capital intensity.

The company continues to return capital to shareholders, distributing $204.7 million year-to-date through dividends and share repurchases. In the third quarter of fiscal 2026, the company returned $51.4 million to shareholders through cash dividends. On March 31, 2026, a quarterly dividend of $0.38 per share was declared, payable on June 5, 2026.

As of February 22, 2026, the company had $57.5 million of cash and cash equivalents, with $3.91 billion of total debt.

Fiscal 2026 Guidance Update

Management modestly updated its full-year outlook by raising the midpoint of net sales guidance to a range of $6.45 billion to $6.55 billion, while tightening adjusted EBITDA guidance at the high end to between $1.08 billion and $1.14 billion. Capital expenditures are expected to be reduced to approximately $400 million. Cost-saving initiatives remain a central focus; management now expects to exceed the cost reduction target of at least $250 million by fiscal year-end 2028.

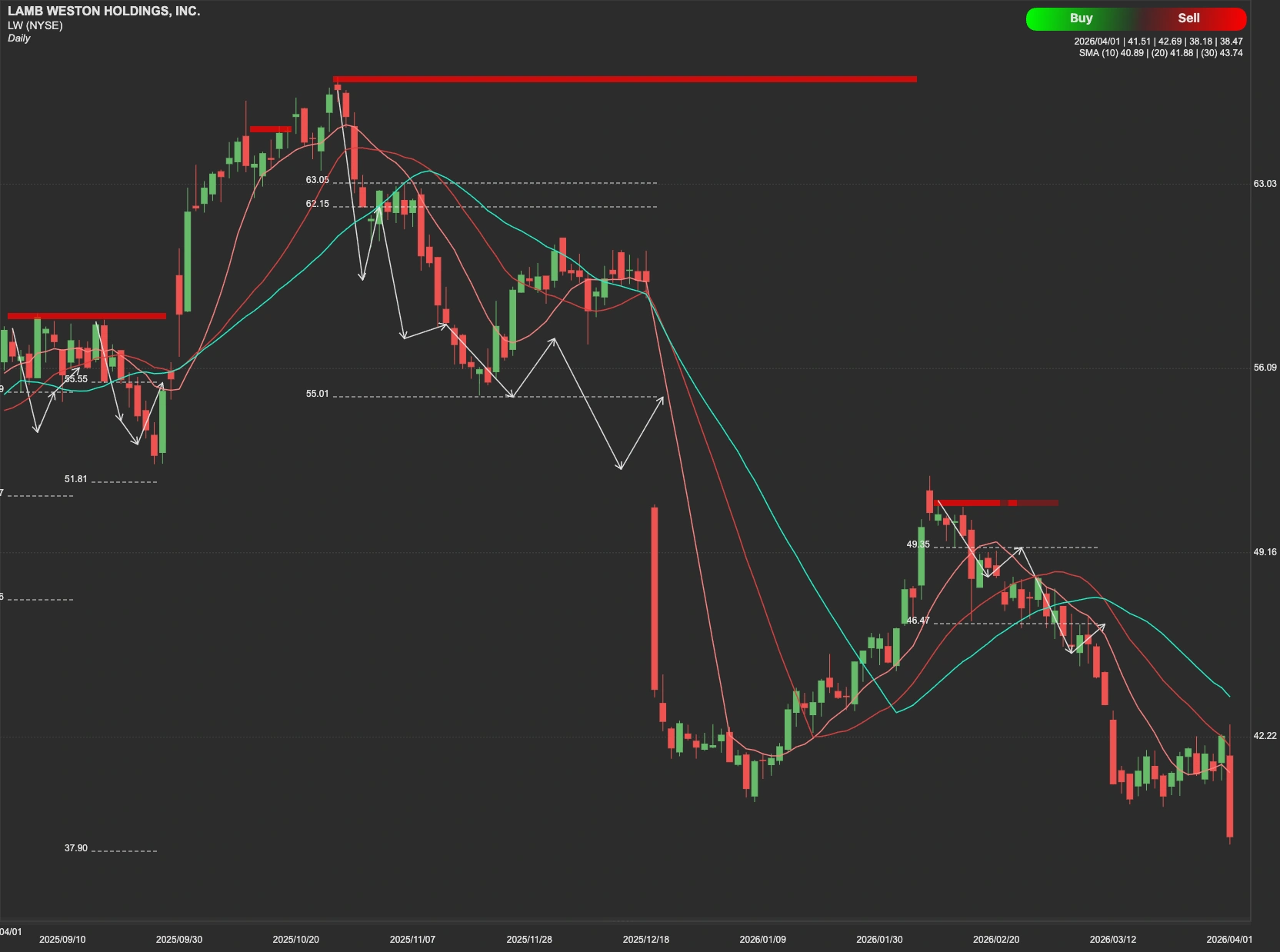

Technical Outlook: Proceed with Caution

From a market perspective, LW stock currently faces an unclear future as the company navigates global competitive dynamics and inflationary pressures.

Short-Term Resistance and Support:

Immediate Resistance: The stock faces a key hurdle at $49.

Secondary Resistance: Should it break and hold above $49, the next significant technical ceiling sits at $62.

Support Level: If the stock fails to find footing, it is likely to seek support at the $28 mark.

Long-Term Outlook:

For long-term investors, the major resistance level to watch is $72. Until the stock can clear these hurdles and show a reversal of its current downward momentum, a cautious stance is warranted.