McDonald's (MCD) Stock Analysis: Sustainable Growth In A Challenging Environment

McDonald's Corporation (MCD) released its third quarter 2025 results on November 5, 2025, demonstrating remarkable resilience and broad-based growth globally. Despite a challenging macro environment, the fast-food giant posted solid top-line figures, driven by strategic focus on value, menu innovation, and its growing loyalty program.

Q3 Financial Highlights: Resilience and Global Momentum

The most significant news in the Q3 report is the impressive recovery in comparable sales across all major segments, reversing declines seen in the prior year:

Comparable Sales: Total Company comparable sales increased 3.6%, a significant turnaround from the 1.5% decline in Q3 2024. International markets were the star performers, with International Developmental Licensed Markets soaring by 4.7% (led by Japan), and International Operated Markets increasing 4.3% (led by Germany and Australia). The highly competitive U.S. market also delivered a solid 2.4% gain, primarily through positive check growth.

Systemwide Sales: Global Systemwide sales grew 8% (or 6% in constant currencies), exceeding $36 billion for the quarter. Systemwide sales include sales at all restaurants, whether owned and operated by the Company or by franchisees. While franchised sales are not recorded as revenues by the Company, the Company's revenues consist of sales by Company-owned and operated restaurants and fees from franchised restaurants operated by conventional franchisees, developmental licensees and affiliates.

Franchise Strength: The key driver continues to be McDonald’s high-margin franchise model. Revenues from franchised restaurants increased 7% to $4.36 billion, offsetting modest declines in Company-owned and operated restaurants sales.

Digital Marketing: The momentum of the MyMcDonald’s Rewards loyalty program is evident, with systemwide sales to loyalty members across 60 markets reaching over $9 billion for the quarter.

Profit Headwinds

However, profitability showed slower growth. Consolidated revenues grew 3% to $7 billion, and GAAP diluted earnings per share (EPS) saw a 2% increase (flat in constant currencies) to $3.18. After adjusting for current and prior-year restructuring charges related to the "Accelerating the Organization" effort, Non-GAAP diluted EPS was flat at $3.22 (a 1% decrease in constant currencies).

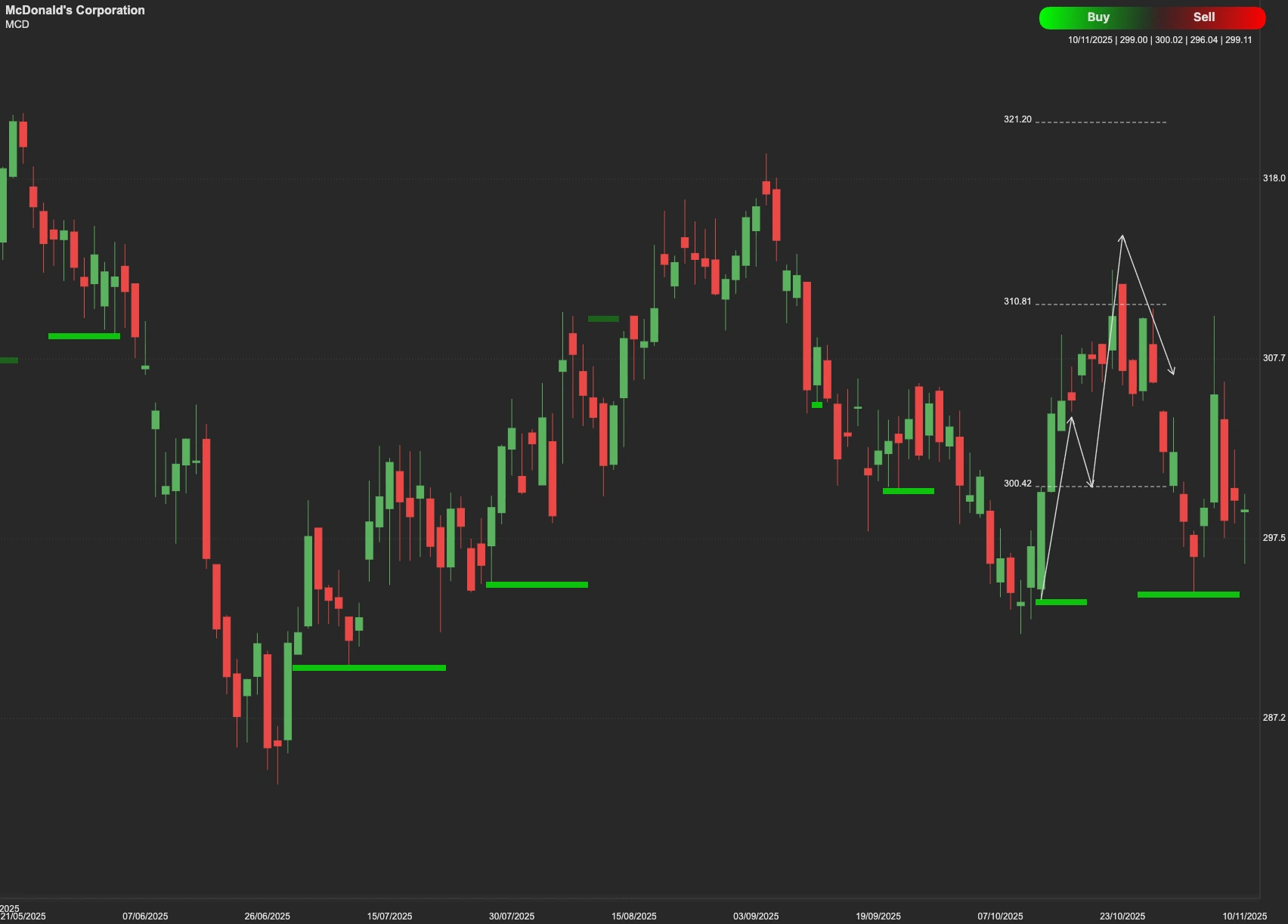

Technical Outlook

From a technical perspective, the immediate and primary challenge for MCD bulls is the resistance level at $314. A convincing breakthrough and sustained trade above this price point is necessary to confirm positive momentum. If the stock breaks and holds above $314, the next projected target for the stock would be the $328 level.

Conversely, a failure to surpass $314 resistance could lead to a retracement as profit-taking occurs or broader market conditions weaken. In this event, the stock is likely to test the first key support level at $278. If selling pressure intensifies and the $278 support level fails, the stock could seek the further support level at $264.