Micron Technology (MU) Stock Analysis: Record Earnings and $250B AI Expansion

Micron Technology, Inc. (NASDAQ: MU) delivered another exceptional quarter, posting record financial results that highlight the strength of the AI-driven memory cycle. The company reported its fifth consecutive quarterly revenue record, while management also introduced transformational Strategic Customer Agreements (SCAs) designed to improve long-term revenue visibility and strengthen future cash flows.

With its record-breaking third quarter of fiscal 2026 and a massive acceleration of its U.S. manufacturing footprint, investors are now watching whether MU can extend its rally through several important technical resistance levels.

Micron Reports Record Fiscal Q3 2026 Results

Micron reported fiscal third-quarter revenue of $41.46 billion, representing a 74% increase from the previous quarter and a remarkable 346% increase compared with the same period last year. The results marked Micron's fifth consecutive quarterly revenue record and the largest sequential revenue increase in company history.

DRAM continued to dominate Micron's business, generating a record $31.3 billion in revenue and accounting for 76% of total company revenue.

DRAM revenue increased 67% sequentially as average selling prices rose in the low-60% range due to tight industry supply conditions and favorable product mix. Management noted that DRAM inventories remain very tight and below 120 days.

NAND also delivered record performance with revenue of $9.9 billion, representing 24% of total revenue and nearly doubling from the previous quarter. NAND average selling prices increased in the mid-80% range as industry supply remained constrained.

Record Profitability Across the Business

Micron generated an extraordinary non-GAAP gross margin of 84.9% during the quarter, up from 74.9% in the previous quarter and more than double the level achieved one year ago.

GAAP operating income reached $33.32 billion, representing an operating margin of 80.4%, while non-GAAP operating income surged to $33.68 billion, representing an operating margin of 81.2%.

GAAP net income climbed to $28.24 billion, or $24.67 per diluted share, while non-GAAP diluted earnings per share in fiscal Q3 was $25.11, up 106% sequentially.

Cash Flow and Balance Sheet

Operating cash flow rose to $25.39 billion, more than doubling from the previous quarter. while free cash flow surged to a company record of $18.3 billion after capital expenditures of $7.1 billion.

The balance sheet strengthened significantly during the quarter as Micron finished with cash and investments of $30.2 billion and $5.7 billion of debt. Net cash increased to $24.4 billion, leaving the company in its strongest financial position in history.

Micron also announced a quarterly dividend of $0.15 per share, payable on July 21, 2026.

Strategic Customer Agreements (SCAs)

The company has already signed 16 SCAs, representing approximately $100 billion of remaining performance obligations based on minimum committed volumes and pricing. Management expects actual revenue generated from these agreements to exceed the disclosed commitments.

These agreements are set to bring in $22 billion in customer deposits and financial commitments (approximately $18 billion in cash deposits), which will strengthen the balance sheet starting in FQ4 2026. This cash will be returned to customers over time, towards the latter half of the agreement term.

The agreements provide greater visibility into long-term demand while reducing uncertainty around future capacity investments.

Massive Manufacturing Expansion Supports Future Growth

Micron continues investing aggressively to meet growing AI memory demand.

- Accelerated construction at its New York semiconductor facility

- Continued expansion of Idaho DRAM fabs

- Expanded advanced packaging capacity in Singapore

- Increased EUV investments through a new multi-year agreement with ASML

On July 9, 2026, the company announced it is accelerating its planned U.S. fab and technology investments and increasing its expected spend to more than $250 billion through 2035, reflecting management's confidence in long-term AI-driven memory demand. Micron expects these investments to support its goal of producing 40% of its DRAM output in the U.S. over the long term.

Outlook Remains Exceptionally Strong

Management provided another record outlook for fiscal fourth quarter 2026.

Micron expects revenue of $50 billion, plus or minus $1 billion, with gross margins near 86% and non-GAAP diluted earnings per share of approximately $31.00. Management expects pricing increases to moderate compared with the explosive gains seen in fiscal Q3.

In fiscal Q4, Micron projects capex of around $10 billion, bringing full-year fiscal 2026 capital spending to approximately $27 billion. The company expects quarterly capex in fiscal 2027 to be above fiscal Q4 levels, with more than half the increase year over year in fiscal 2027 from construction capex.

The company also expects fiscal 2027 operating expenses to rise by approximately $1 billion as it increases research and development spending to capitalize on what management describes as an unprecedented opportunity in memory and storage technologies.

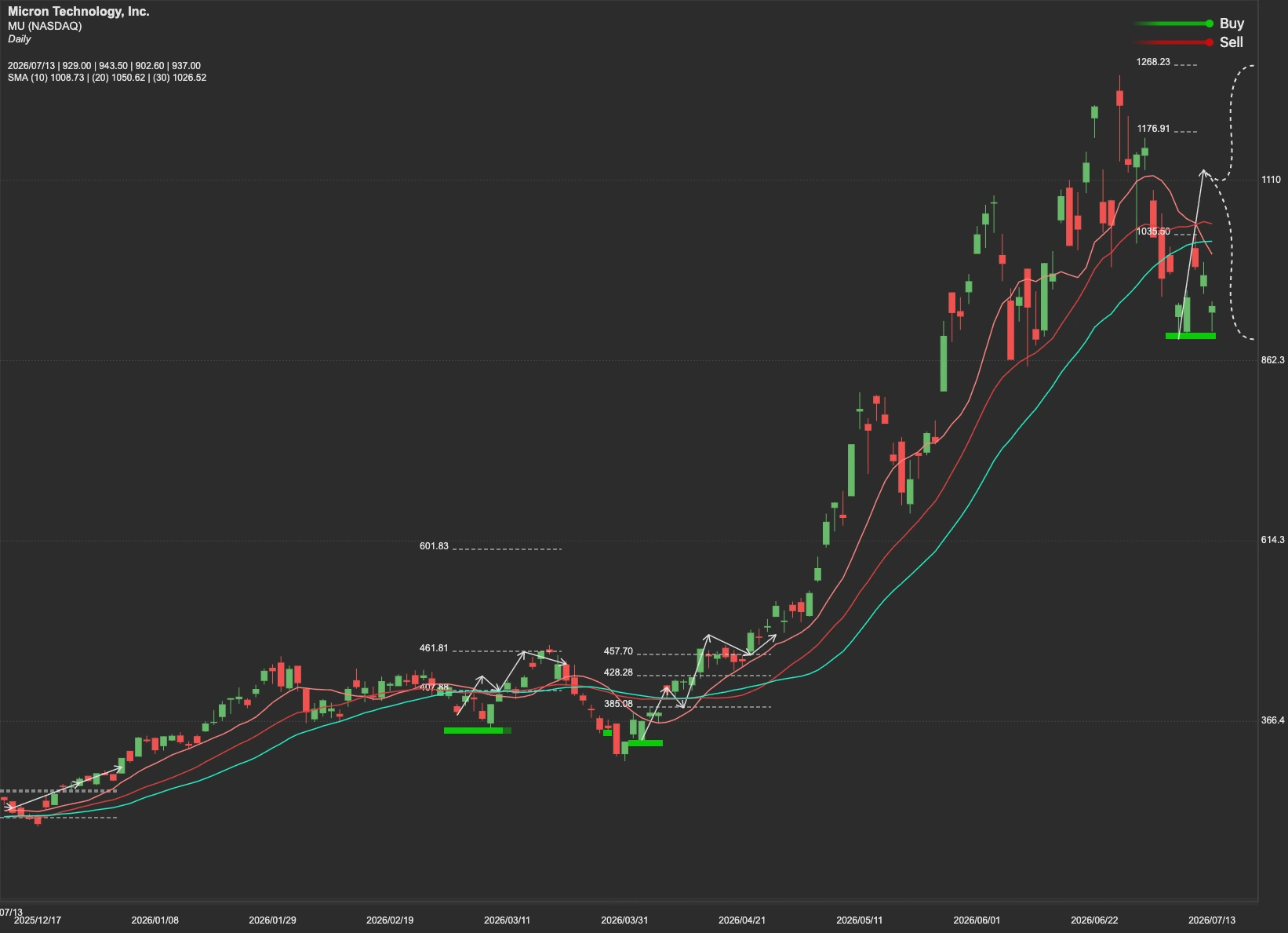

MU Stock Technical Analysis

Micron stock remains in a strong long-term uptrend supported by record profitability, rapidly expanding free cash flow, and favorable AI industry fundamentals.

The immediate resistance level is located near $996. A successful breakout and sustained move above this level would likely open the door for the next upside target near $1058. If bullish momentum continues and MU successfully establishes support above $1058, the next major technical objective would be $1156.

However, failure to break above resistance may trigger profit-taking and a retest of the first important support level at $884. If selling pressure intensifies, investors should closely monitor the stronger support zone near $858.