Netflix Stock Analysis: Strong Fundamentals Tested by Warner Bros. Acquisition

Netflix, Inc. (NASDAQ: NFLX) delivered a solid operational performance in the fourth quarter of 2025, meeting or exceeding all of its full-year financial objectives. However, despite robust earnings growth, expanding margins, and accelerating free cash flow, the company’s stock has declined approximately 15% since December 5, 2025, when Netflix announced its agreement to acquire Warner Bros. for a total enterprise value of $82.7 billion.

The recent pullback highlights a growing disconnect between Netflix’s underlying business momentum and investor concerns around balance sheet risk and execution complexity tied to the Warner Bros. acquisition.

Strong Q4 and Full-Year 2025 Financial Performance

Netflix closed 2025 with revenue of $45.2 billion, up 16% year over year (17% on an FX-neutral basis), while operating margin expanded to 29.5%, a 300-basis-point improvement from 2024. Fourth-quarter revenue rose 18% year over year to $12.1 billion, supported by continued paid membership growth, pricing actions, and rapidly scaling advertising revenue.

Operating income in Q4 increased 30% year over year to approximately $3.0 billion, while diluted EPS rose 31% to $0.56, slightly above internal guidance. Netflix also crossed a major milestone during the quarter, surpassing 325 million paid memberships globally.

Free cash flow generation remained a key strength. Netflix produced $10.1 billion in operating net cash and $9.5 billion in free cash flow for full-year 2025, well ahead of prior-year levels, reinforcing the durability of its operating model and content monetization strategy.

Advertising, Engagement, and Content Momentum

Advertising continues to emerge as a meaningful growth lever. In just its third year of ad sales, Netflix reported ad revenue exceeding $1.5 billion in 2025, representing more than 2.5x growth year over year, with management projecting a rough doubling again in 2026.

Engagement metrics also remained healthy. Members watched 96 billion hours on Netflix in the second half of 2025, up 2% year over year, driven by a 9% increase in viewing of Netflix-branded originals. Flagship titles such as Stranger Things, Bridgerton, and Guillermo del Toro’s Frankenstein reinforced Netflix’s ability to generate global fandom, a key driver of retention and long-term pricing power. However, the overall engagement growth in the second half of 2025 was partially offset by a year-over-year decline in viewing of non-branded view hours. This decrease primarily reflected a lower volume of licensed, second-run content across most regions following an elevated period of licensing during 2023-2024 as a result of the WGA strike, which temporarily shut down new production.

Warner Bros. Acquisition: Strategic Upside vs Market Anxiety

The market’s primary concern lies not with Netflix’s core business, but with the Warner Bros. acquisition, now structured as an all-cash transaction.

Strategically, the deal offers:

-

A world-class IP and film/TV library

-

HBO Max, enabling more personalized and flexible subscription options

-

Expanded global production and content depth

-

Grow investment in original content over the long-term

However, near-term investor hesitation reflects increased leverage via bridge financing and the temporary pause in share buybacks to accumulate cash to help fund the pending acquisition of Warner Bros. Netflix ended Q4 with $14.5 billion in gross debt and $9.0 billion in cash and cash equivalents. Netflix has stated its intent to reduce bridge facilities commitments through a combination of future bond offerings and cash from the balance sheet. The company remains committed to maintaining an investment-grade rating.

Outlook

Looking ahead, Netflix forecasts 2026 revenue of $50.7–$51.7 billion, representing 12%–14% year-over-year growth, with operating margin expanding further to 31.5% despite approximately $275M of acquisition-related expenses. Free cash flow is expected to rise to approximately $11 billion.

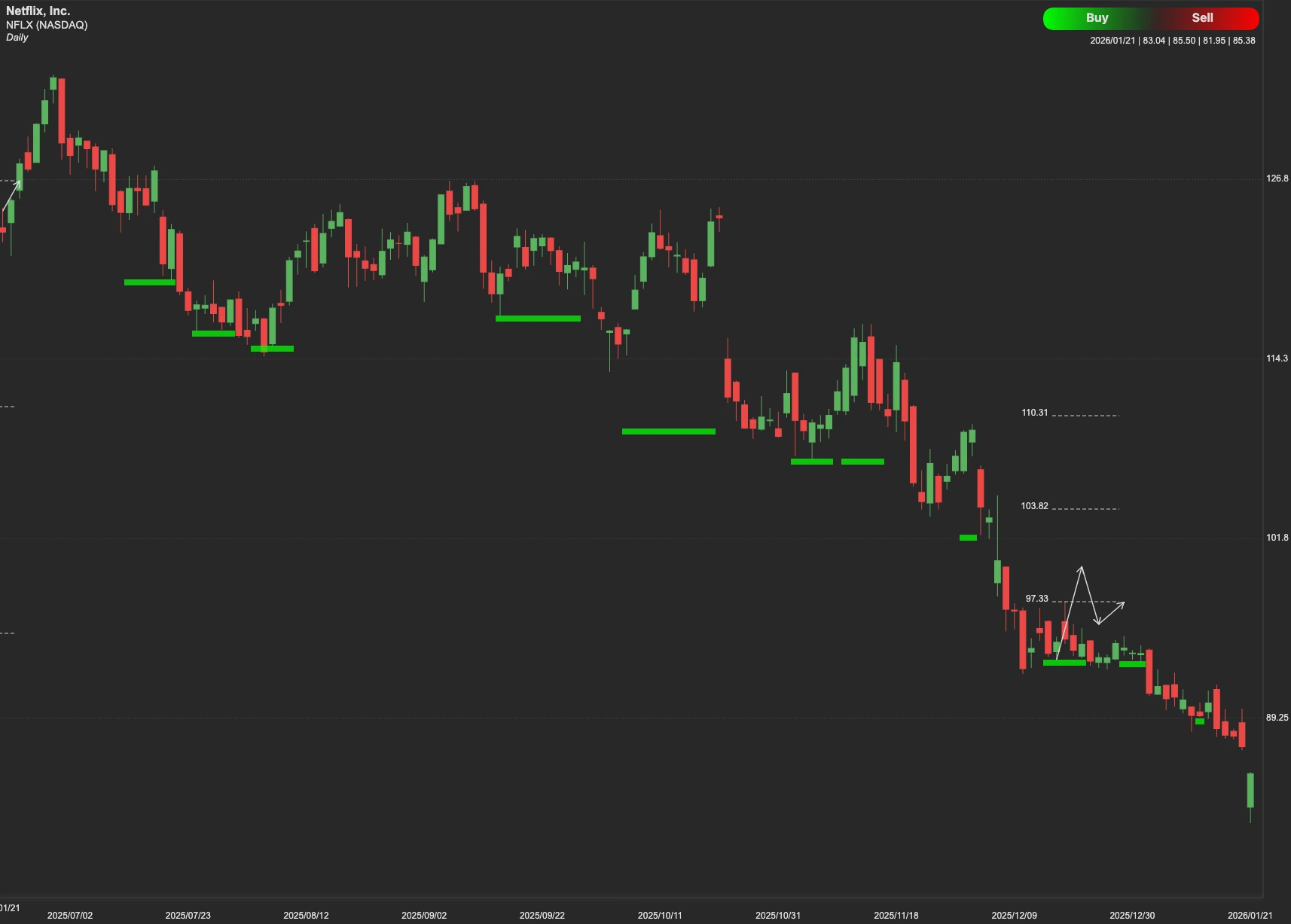

NFLX Technical Analysis

From a technical perspective, Netflix shares remain under technical pressure following the post-acquisition sell-off. The initial resistance stands at $106. A sustained move above this level would be the first signal of improving short-term momentum. The secondary resistance is located at $116, representing a more meaningful technical ceiling. A confirmed breakout above $116 would likely shift market sentiment and open the door to a move toward $131, the next upside objective.

Conversely, if the stock fails to hold current levels, defensive support at $76 serves as the primary floor. A deeper correction to $60 could occur if macroeconomic headwinds or acquisition-related uncertainty persists.