NVIDIA Stock Analysis: AI Demand Continues to Drive Record Revenue

NVIDIA (NASDAQ: NVDA) recently delivered another exceptional quarter ended April 26, 2026, reinforcing its position as the clear leader of the AI infrastructure revolution. Fiscal first-quarter 2027 results exceeded expectations, with record revenue, accelerating data center demand, and stronger shareholder returns.

Record Financial Performance

NVIDIA reported first-quarter fiscal 2027 revenue of $81.6 billion, representing 85% year-over-year growth and 20% sequential growth, another record for the company.

The biggest growth driver remained the Data Center business, where revenue surged to $75.2 billion, up 92% from the same quarter last year. Demand was fueled by the rapid deployment of Blackwell 300 products and continued adoption of InfiniBand, Spectrum-X™ Ethernet, and NVLink™ solutions.

Importantly, management noted that approximately half of Data Center revenue now comes from a continued diversification of customers, including AI Clouds, industrial, enterprise, and sovereign customers. No shipments of Data Center Hopper products to China occurred during the quarter, compared with $4.6 billion in the first quarter of fiscal year 2026.

Meanwhile, Edge Computing generated $6.4 billion in revenue, growing 29% year over year, supported by strong Blackwell workstation demand despite softer consumer PC demand.

Profitability Remains Outstanding

GAAP gross margin remained exceptionally high at 74.9%, while operating income was $53.5 billion, an increase of 147% from a year ago. Operating expenses for the first quarter were up 52% from a year ago. These increases were driven by higher compensation and benefits expense due to employee growth and compensation increases, compute and infrastructure costs, and engineering development materials for new product developments.

GAAP net income reached an impressive $58.3 billion, more than tripling from the previous year, while diluted GAAP earnings per share climbed to $2.39, up 214% from the same period last year.

On a non-GAAP basis, gross margin was 75%, while earnings reached $1.87 per diluted share, up 140% year over year.

Massive Cash Generation and Shareholder Returns

Operating cash flow reached $50.3 billion during the quarter, while cash, cash equivalents, and marketable debt securities totaled $50.3 billion.

Management returned approximately $20 billion through share repurchases and dividends during the quarter. As of the end of the first quarter, the company had $38.5 billion remaining under its share repurchase authorization. In addition, the board approved an additional $80 billion share repurchase authorization with no expiration date. NVIDIA raised its quarterly dividend from $0.01 per share to $0.25 per share, signaling management's confidence in the company's long-term cash generation.

AI Growth Story Continues

CEO Jensen Huang described the current AI buildout as the largest infrastructure expansion in human history, and NVIDIA's product roadmap supports that ambitious vision.

During the quarter, NVIDIA introduced the Vera Rubin platform, announced new AI networking technologies, expanded enterprise AI software offerings, strengthened partnerships with major cloud providers, and continued pushing into robotics, autonomous driving, telecommunications, industrial automation, and edge AI.

The company also reorganized its reporting structure into two primary platforms—Data Center and Edge Computing—reflecting where management expects future growth to be concentrated.

Guidance Signals Continued Momentum

Management guided fiscal second-quarter revenue to $91 billion, plus or minus 2%, despite assuming zero Data Center compute revenue from China.

Gross margins are expected to remain exceptionally strong at 74.9%, plus or minus 50 basis points, while operating expenses are expected to be approximately $8.5 billion.

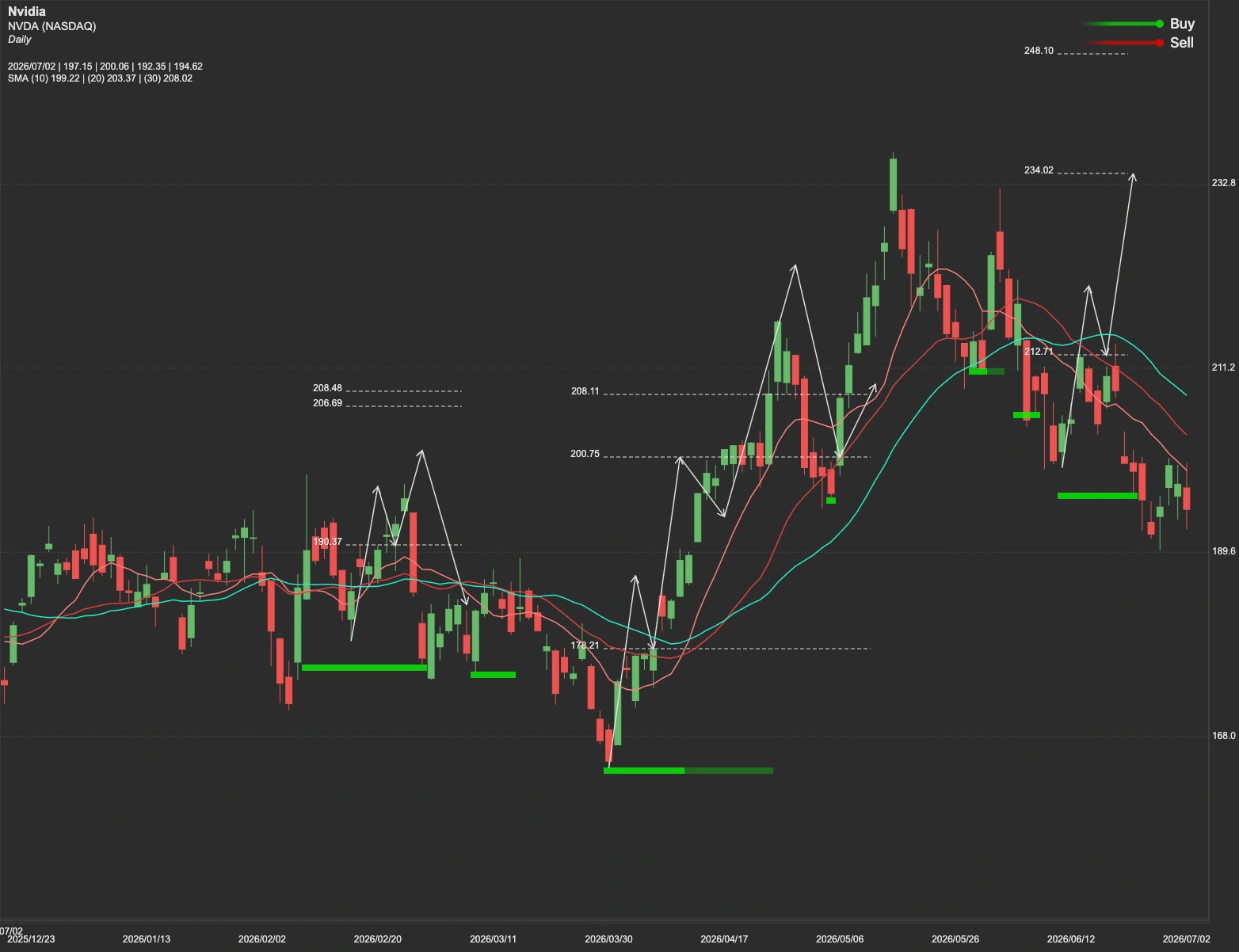

NVDA Stock Technical Analysis

From a technical perspective, NVDA remains firmly in an established uptrend. The key level investors are watching is $231, which currently serves as a major resistance area. A decisive breakout and sustained move above this level could open the door toward the next upside target around $250.

However, if the stock is unable to overcome the $231 resistance, a period of consolidation or pullback becomes increasingly likely. In that scenario, the first major support sits near $188, where buyers may attempt to defend the prevailing uptrend. Should selling pressure intensify, the next important demand zone lies between $167 and $163.