Palo Alto Networks: Strong Q2 Results with Aggressive Acquisitions

Palo Alto Networks (NASDAQ: PANW) continues to pivot aggressively toward a future defined by AI-native security and "platformization." However, despite reporting double-digit growth and a flurry of strategic acquisitions, the market’s immediate reaction has been one of caution. Following the release of its fiscal second quarter 2026 financial results, PANW shares slipped 6.9%.

Fiscal Q2 Performance: The Numbers

For the quarter ended January 31, 2026, Palo Alto Networks delivered a solid top-line performance. Revenue climbed 15% year-over-year to $2.6 billion, fueled by a 33% surge in Next-Generation Security (NGS) ARR, which now stands at $6.3 billion. The company’s Remaining Performance Obligation (RPO)—a key indicator of future revenue—jumped 23% to $16.0 billion.

On a profitability basis, the company maintained its streak of operational excellence. Non-GAAP operating margins remained above 30% for the third consecutive quarter. GAAP net income reached $432 million, or $0.61 per diluted share, compared with $267 million, or $0.38 per diluted share, in the same quarter last year, and non-GAAP diluted EPS reached $1.03, beating the prior year's $0.81. The company continues to benefit from strong subscription and support revenue, which forms the majority of total revenue and provides high visibility and margin stability. CEO Nikesh Arora attributed this strength to the accelerating trend of "platformization," as customers are keen to both modernize and normalize their cybersecurity stack to defend against AI-driven threats.

Strategic Expansion: Identity, Observability and AI Endpoint Security

Recent acquisitions are central to Palo Alto’s long-term thesis.

The completed acquisition of CyberArk strengthens identity security across human, machine and agentic identities. Under the transaction terms, CyberArk shareholders receive $45 in cash plus 2.2005 PANW shares for each CyberArk ordinary share, introducing dilution but expanding the addressable market in privileged access and identity governance.

By closing the Chronosphere Acquisition on January 29 for $3.35 billion, Palo Alto Networks is merging observability with security. In the AI era, security is "blind" without the ability to monitor the massive data volumes. With this acquisition, Palo Alto Networks is redefining how organizations run at the speed of AI—by enabling customers to gain deep, real-time visibility into their applications, infrastructure, and AI systems—while maintaining strict control over data cost and value.

Additionally, the announced acquisition of Koi positions Palo Alto at the frontier of Agentic Endpoint Security — a category targeting risks created by AI agents operating with privileged access across enterprise systems.

Guidance for Q3 and full-year FY2026

Management has provided a detailed roadmap for the remainder of fiscal 2026, highlighting significant growth in recurring revenue offset by short-term integration pressures.

For Fiscal Third Quarter 2026:

-

Revenue & Growth: Total revenue is expected between $2.941 billion and $2.945 billion (28%–29% growth).

-

Next-Generation Security ARR: Targeted at $7.94 billion to $7.96 billion, representing a massive 56% year-over-year jump.

-

Earnings Dip: Diluted non-GAAP EPS is projected at $0.78 to $0.80, using 812 million to 817 million shares outstanding, compared with $0.80 in Q3 FY2025. This is a notable step down from the $1.03 achieved in Q2 FY2026.

For Full Fiscal Year 2026:

-

Total revenue guidance now sits at $11.28 billion to $11.31 billion (22%–23% growth).

-

Next-Generation Security ARR is expected to reach up to $8.62 billion (53%–54% growth).

-

Diluted non-GAAP net income per share in the range of $3.65 to $3.70, using 768 million to 773 million shares outstanding, with an adjusted free cash flow margin of 37%. Non-GAAP operating margin is targeted at 28.5% to 29.0%. This follows a Q1 report where management initially targeted a slightly higher non-GAAP EPS of $3.80 to $3.90, using 710 million to 716 million shares outstanding, a higher free cash flow margin of 38%–39%, and non-GAAP operating margin of 29.5% to 30.0%.

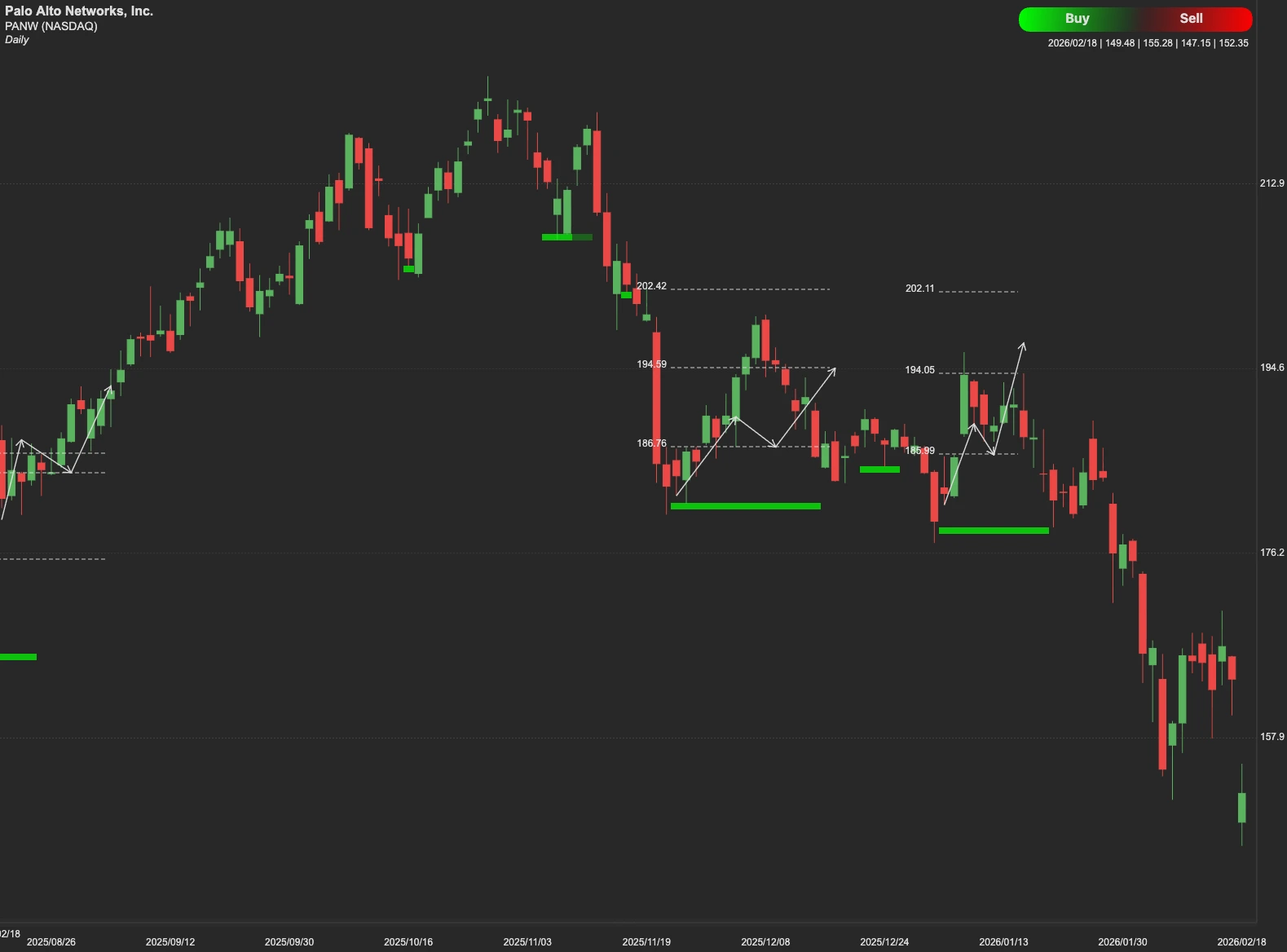

Technical Outlook: Key Levels to Watch

Despite the strategic wins, the 6.9% post-earnings drop has placed the stock in a delicate position technically. Investors are currently weighing the "integration value" of these recent deals against the immediate costs and execution risks. The immediate battleground for the stock is the $179 resistance level. For a sustained upward trend to be confirmed, the stock must not only reclaim $179 but also clear the secondary hurdle at $195. Breaking through $195 would signal a renewed bullish phase and market confidence in the post-merger integration.

However, if the stock fails to gain momentum and breaks lower, the first major line of defense is the support at $123. In a broader market correction, shares could seek a deeper floor at the $100 mark.