Rivian Stock Analysis: Positive Gross Profit and AI Ambitions

Rivian Automotive, Inc. (NASDAQ: RIVN) recently delivered its Q3 2025 financial results, marking a watershed moment in its journey toward profitability. The report, released November 4, 2025, detailed significant operational breakthroughs, highlighted by the company’s first-ever quarter with positive consolidated gross profit.

Financial Turnaround and Revenue Drivers

Rivian reported total consolidated revenues of $1,558 million for the quarter, marking a substantial 78% year-over-year increase from $874 million in Q3 2024. This growth was driven by two key segments:

Automotive Revenue: Increased 47% to $1,142 million, boosted by a high-delivery quarter (13,201 vehicles) and increased average selling prices.

Software and Services Revenue: Soared 324% to $416 million. This explosive growth was primarily attributed to the software and electrical architecture joint venture created with Volkswagen Group, which contributed approximately $214 million in revenue.

Crucially, the company flipped its consolidated gross profit from a $(392) million loss in Q3 2024 to a $24 million profit in Q3 2025. This achievement was fueled by the $154 million gross profit from Software and Services, even as the Automotive segment’s gross loss improved by $249 million year-over-year to $(130) million.

Despite the operational improvements, the company posted a net loss of $(1,166) million, slightly higher than the prior year, influenced by an increase in R&D and SG&A expenses, and a notable $(191) million other expense related to the settlement of pending securities class action litigation.

Liquidity and Outlook

Rivian ended the quarter with $7.1 billion in cash and short-term investments, and total liquidity of $7.7 billion. The company reaffirmed its 2025 guidance, expecting adjusted EBITDA losses between $(2.0) billion and $(2.25) billion and capital expenditures of $1.8 billion–1.9 billion.

Strategic Progress: R2 and Autonomy

Rivian's strategic outlook focuses heavily on the future, primarily the R2 SUV and advanced technology. The R2 remains on track for deliveries in the first half of 2026. Operational readiness is advancing rapidly at the Normal, Illinois facility, including the completion of an upgraded paint shop which increases annual capacity up to 215,000 units.

Key R2 innovations highlighted include:

A clean-sheet battery pack design using the new 4695 cell-to-pack structure to minimize mass.

The Energy Management Control Module, which features a bidirectional on-board charger enabling vehicle-to-home power supply capability.

Furthermore, the company is intensifying its focus on AI, scheduling an Autonomy & AI Day on December 11, 2025, to share details on its AI-centric, end-to-end platform. This focus is also reflected in the new company, Mind Robotics, launched in November to focus on the advancement of industrial AI to reshape how physical world businesses operate and leverage Rivian operations data as the foundation for a robotics data flywheel.

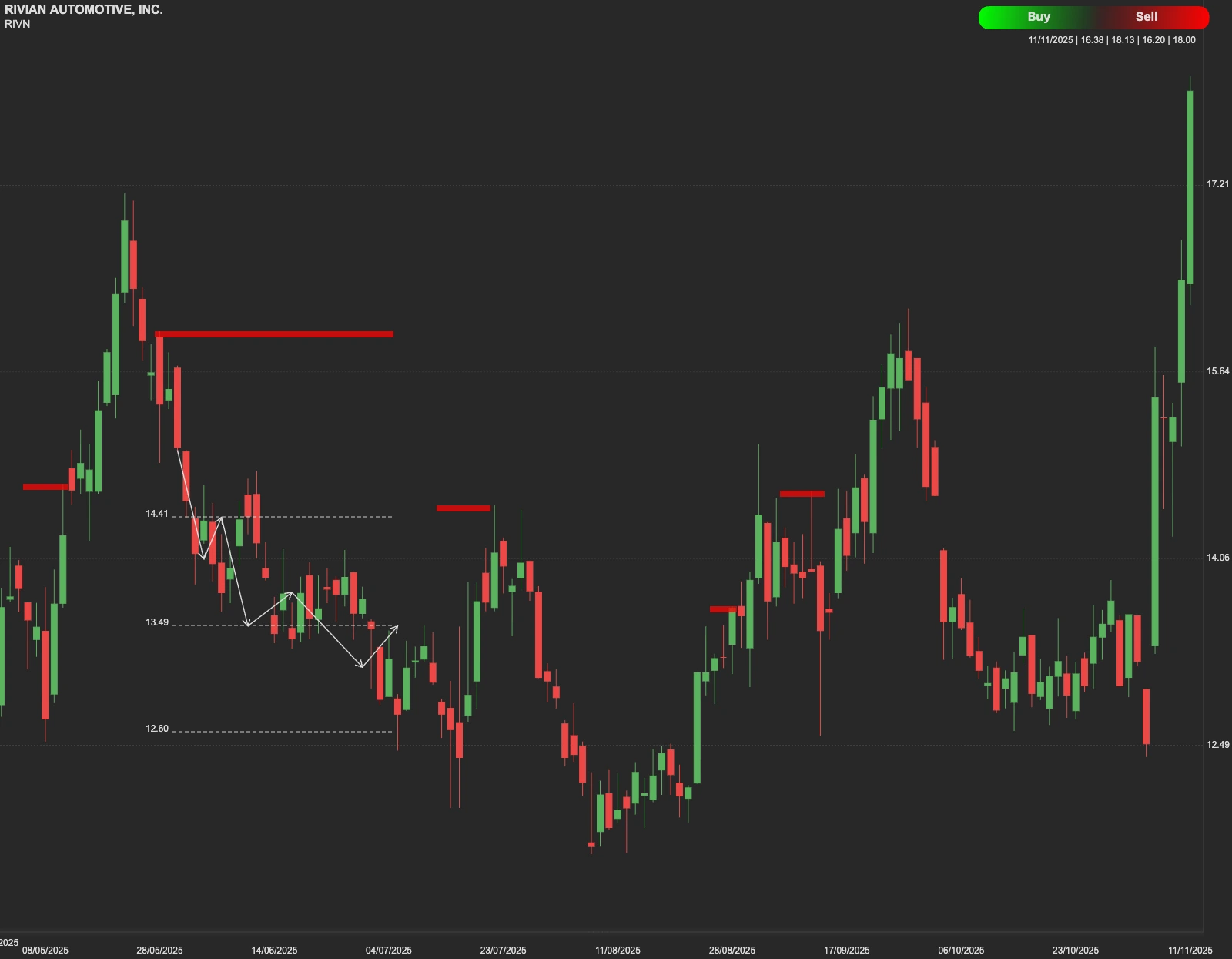

Stock Technical Outlook

While Rivian’s fundamentals are improving, its stock continues to face key technical challenges for the short term. The immediate resistance level is at $23—if the price breaks above this point, it could attempt to reach $28. However, failure to break resistance may lead the stock to retest its support at $13, with a further, more critical support lying near $9.

Conclusion

Rivian’s Q3 results show meaningful progress toward profitability and operational maturity, with solid revenue growth, improved margins, and expanding software capabilities. However, despite the recent stock surge of 44% since November 4, 2025, following the release of its third-quarter financial results, long-term direction remains uncertain as the company continues to burn cash and expects adjusted EBITDA losses between $(2.0) billion and $(2.25) billion.