RPM Stock Analysis: Record Sales, But Margin Pressure

RPM International (NYSE: RPM) delivered mixed fiscal 2026 second-quarter results, pairing record revenue with declining earnings as softer construction demand, higher costs, and integration inefficiencies weighed on margins. While near-term pressure remains evident, management’s newly announced $100 million SG&A optimization plan could mark a turning point for profitability.

Fundamental Performance: Growth vs. Headwinds

RPM posted record Q2 sales of $1.91 billion, up 3.5% year over year, driven largely by acquisitions and demand for high-performance building solutions. Sales included a 0.5% organic decline, 3.4% growth from acquisitions, and a 0.6% benefit from foreign currency translation. However, underlying momentum weakened as the quarter progressed. Organic sales declined 0.5%, reflecting soft DIY demand and longer construction project lead times amid a prolonged government shutdown.

Net income fell 12% to $161.2 million, while adjusted diluted EPS declined 13.7% to $1.20, missing the prior-year record. Adjusted EBIT dropped 11.2% to $226.6 million as growth investments, reduced fixed-cost absorption from lower volumes and temporary inefficiencies from plant and warehouse facility consolidations more than offset MAP 2025 operational improvements.

Segment Performance

Construction Products Group (CPG): Sales rose 2.4% to a record level, supported by roofing solutions for high-performance buildings. However, adjusted EBIT declined nearly 11% due to weaker disaster restoration activity and higher costs.

Performance Coatings Group (PCG): The most stable segment, with sales up 4.4% and adjusted EBIT essentially flat, as pricing and volume gains were offset by growth investments and unfavorable mix.

Consumer Group: Revenue increased 4.1% on acquisitions and pricing, but organic sales fell sharply. Adjusted EBIT declined 6.2% amid softer DIY demand, plant consolidation impacts, and distribution center startup costs.

Cost Optimization

Facing a slower demand environment, RPM is accelerating SG&A-focused optimization actions expected to deliver approximately $100 million in annual savings once fully implemented. Management expects $5 million of benefits in the third quarter of fiscal 2026, $20 million in the fourth quarter of fiscal 2026, and an incremental $75 million in fiscal 2027.

If executed effectively, these actions could materially improve margins and help RPM better leverage its scale once demand stabilizes, especially given the company’s strong cash generation.

Balance Sheet and Cash Flow

Operating cash flow remained a bright spot, totaling $583.2 million in the first half of fiscal 2026, the second-highest level in company history. However, total debt rose to $2.52 billion, reflecting acquisition activity, while liquidity declined to $1.10 billion.

Outlook: Cautious Optimism Amid Uncertainty

Management expects mid-single-digit sales growth in both the third and fourth quarters, with adjusted EBIT improving mid- to high-single digits in Q3 and low- to high-single digits in Q4. While visibility remains limited, RPM anticipates benefits from deferred construction projects and cost-saving initiatives as the year progresses.

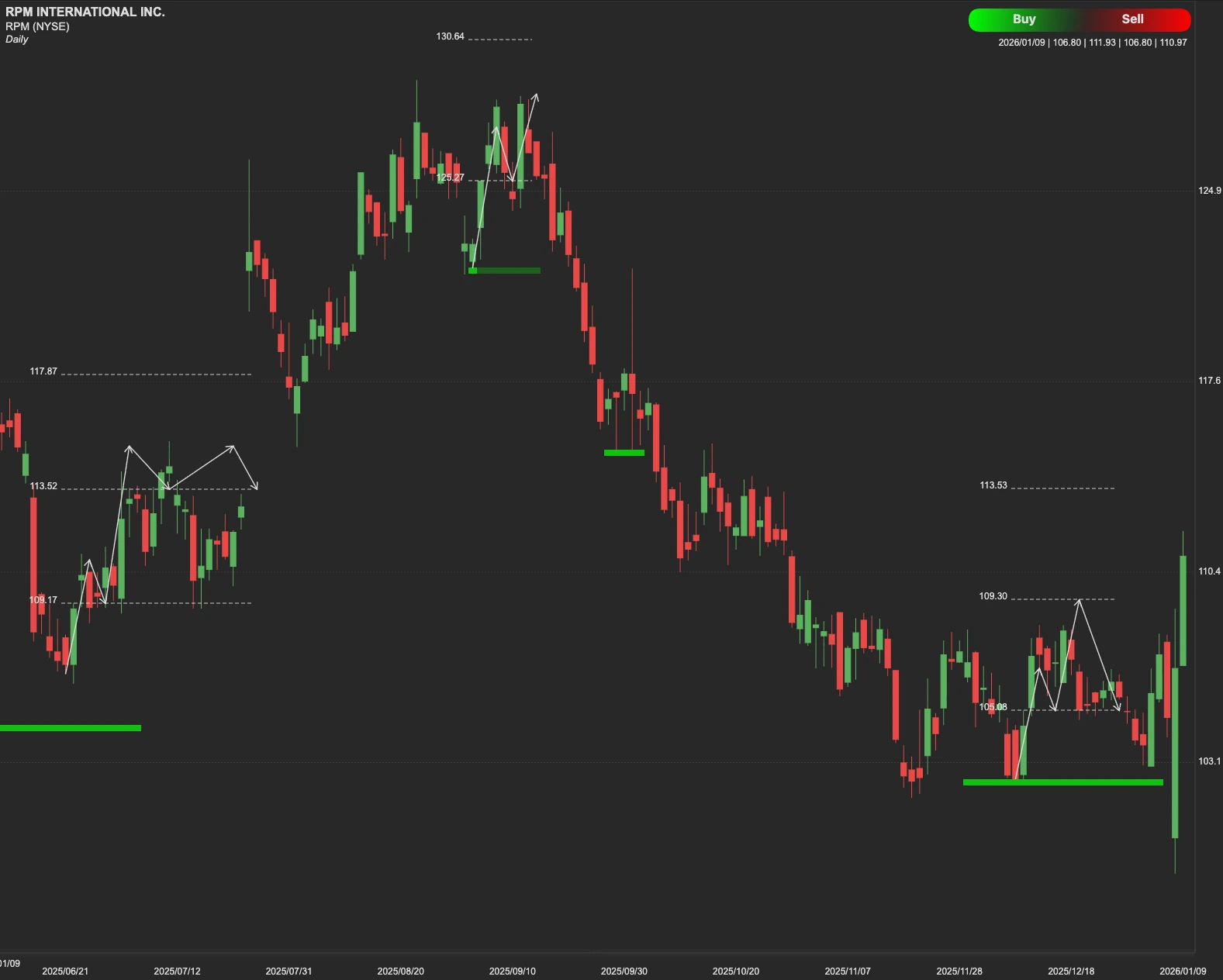

RPM Stock Technical Analysis

From a technical perspective, RPM stock is approaching a critical resistance level at $128. A sustained break and hold above $128 could open the door for a move toward the $139 level. Failure to clear resistance may lead the stock to retest support near $95. A breach of $95 would likely lead to a test of the $85 zone, which serves as a major long-term accumulation area.