Salesforce Record Q4: Scaling the "Agentic Enterprise"

Salesforce (NYSE: CRM) has closed fiscal 2026 with record results, reinforcing its position as the world’s leading AI-powered CRM platform. With accelerating adoption of Agentforce and Data 360, expanding earnings, and strong shareholder returns, fundamental momentum remains constructive.

Q4 FY26: Solid Revenue Growth, Mixed Margin Dynamics

In the fourth quarter of FY26, Salesforce generated $11.2 billion in revenue, up 12% year-over-year from $9.99 billion. Subscription and support revenue rose 13% to $10.7 billion, while professional services declined modestly by 3.0%.

Gross profit reached $8.69 billion, resulting in a 77.6% gross margin, slightly down from 77.8% a year ago. The minor compression reflects higher subscription-related costs growing faster than revenue.

Operating income came in at $1.87 billion, with GAAP operating margin at 16.7%, down from 18.2% last year as operating expenses rose 14.6% year-over-year, driven by continued investment in sales, marketing, and R&D.

However, net income increased 13.8% to $1.94 billion, outpacing revenue growth. A significant contributor was the sharp rise in gains on strategic investments, which climbed to $811 million versus $96 million in the prior year period.

On a non-GAAP basis, Q4 operating income reached $3.84 billion, translating to a 34.2% operating margin, up from 33.1% a year ago. Non-GAAP diluted EPS increased to $3.81 from $2.78.

FY26: Expanding Margins and Accelerating Profitability

For the full fiscal year, revenue rose 10% to $41.5 billion, with subscription and support revenue growing 10.4% and accounting for 95% of total revenue.

Gross profit increased to $32.26 billion, and gross margin improved to 77.7%, up 50 basis points year-over-year.

Operating income reached $8.33 billion, lifting GAAP operating margin to 20.1%, compared to 19.0% in FY25. On a non-GAAP basis, operating margin expanded to 34.1%, reflecting disciplined cost control despite ongoing AI and platform investments.

Net income climbed 20.3% to $7.46 billion. The expansion was supported by operating leverage and a notable swing in strategic investment results—from a $121 million loss last year to a $1.02 billion gain in FY26.

Non-GAAP net income reached $11.97 billion, with non-GAAP diluted EPS rising to $12.52 from $10.20.

Backlog Strength and Agentforce Scaling

Salesforce reported current remaining performance obligation of $35.1 billion, up 16% year-over-year (13% in constant currency), including 4pts contribution from Informatica. Remaining performance obligation reached $72.4 billion, rising 14% annually.

Salesforce introduced Agentic Work Units (AWUs) as a standardized metric to quantify AI-driven task completion. To date, 2.4 billion AWUs have been delivered across Agentforce and Slack, growing 57% quarter-over-quarter.

The platform has processed more than 19 trillion tokens to date, up 5x year-over-year.

Over 60% of Q4 bookings in Agentforce and Data 360 came from existing customer expansion.

Agentforce and Data 360 annual recurring revenue now exceeds $2.9 billion, up over 200% year-over-year. Within that: Informatica Cloud ARR of $1.1 billion and Agentforce ARR of $800 million, up 169% year-over-year.

Salesforce has closed more than 29,000 Agentforce deals since launch, increasing 50% quarter-over-quarter.

In FY26 alone, Data 360 ingested 112 trillion records (+114% YoY), including 53 trillion via Zero Copy (+310% YoY), and processed 18 terabytes of unstructured data.

Collectively, Salesforce industry businesses finished the year at $6.6 billion ARR, up nearly 20% year-over-year.

Cash Flow Strength and Capital Returns

Cash generation remained strong. Operating cash flow increased 15% to $15.0 billion, while free cash flow rose 16% to $14.4 billion. Salesforce returned $14.3 billion to shareholders through $12.7 billion in share repurchases and $1.6 billion in dividends. The board also authorized a new $50 billion share repurchase program and raised the quarterly dividend 5.8% year-over-year to $0.44 per share.

Fiscal 2027 Outlook

For FY27, Salesforce guides:

-

Revenue: $45.8B–$46.2B (10%–11% growth).

-

GAAP operating margin: 20.9%.

-

Non-GAAP operating margin: 34.3%.

-

GAAP diluted net income per share: $7.85 - $7.93.

-

Non-GAAP diluted net income per share: $13.11 - $13.19.

-

Operating cash flow growth: Approximately 9%–10%.

-

Non-GAAP Capital expenditures: Approximately 1.5% of revenue.

Management expects organic revenue re-acceleration in the second half of FY27.

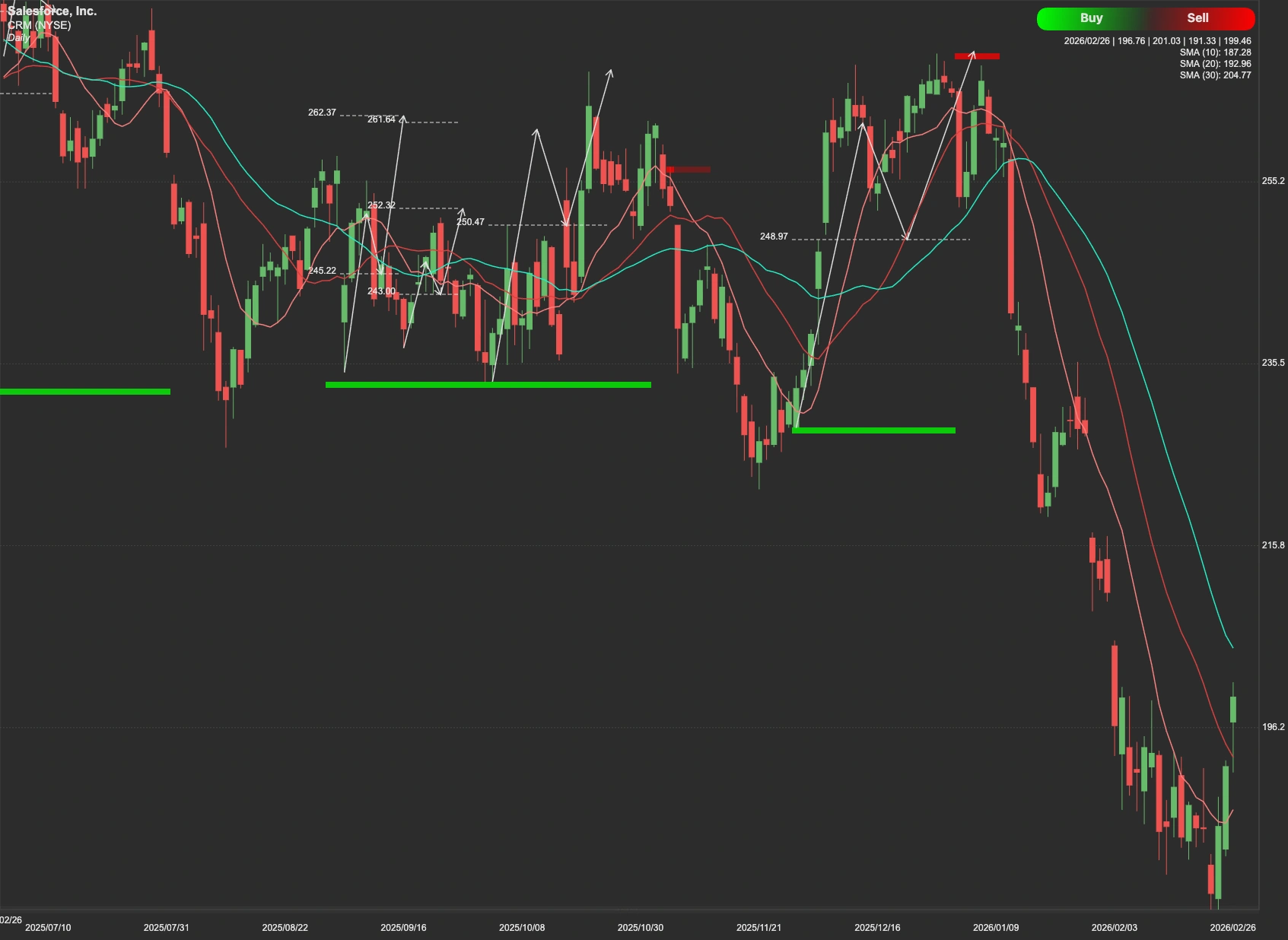

Technical Outlook

Despite the fundamental strength, CRM is currently navigating a complex technical landscape. For the bulls to take full control, the stock must clear specific supply zones. The immediate focus is the $236 resistance level. If CRM can decisively close and hold above $236, it clears the path for a move toward the next major objective at $271. Breaking these levels would confirm a sustained upward trend.

However, without a breakout, consolidation or retracement toward lower support levels remains possible. If the stock loses momentum, investors should look for initial support at $185. In a more significant market correction, a deeper support zone exists between $173 and $160.