SJM Stock Jumps 15% After Earnings, But Technical Hurdles Remain

Shares of The J.M. Smucker Co. (NYSE: SJM) surged approximately 15% following the company's fiscal fourth-quarter and full-year 2026 earnings release. The owner of well-known brands including Folgers, Dunkin' packaged coffee, Jif peanut butter, Uncrustables sandwiches, and Milk-Bone delivered a solid quarter despite continued pressure from inflation, tariffs, and evolving consumer spending patterns.

Strong Fourth-Quarter Performance

The company reported fourth-quarter net sales of $2.3 billion, representing a 6% year-over-year increase, driven primarily by pricing actions across its coffee and sweet baked goods. Comparable net sales also rose 6%. This growth was heavily price-driven, with net price realization boosting sales by 10%, helping offset a 4% decline in volume/mix.

Gross profit increased 5% to $862.1 million, although gross margin slipped modestly to 38.0% from 38.4% last year as commodity inflation and tariff-related costs continued to pressure profitability.

Operating income reached $444.5 million compared to a loss-impacted result in the prior year, benefiting from the absence of large impairment charges, the increase in gross profit, and a decrease in selling, distribution, and administrative ("SD&A") expenses.

Adjusted earnings per share climbed 20% year-over-year to $2.77, while GAAP diluted earnings per share reached $3.64, a sharp turnaround from the prior-year loss. Net income totaled $388.1 million, compared with a loss of $729 million a year earlier.

Among business segments, U.S. Retail Coffee remained the largest contributor, with sales rising 12% to $830.6 million due to stronger pricing across brands including Folgers and Dunkin'. Meanwhile, the company continued to benefit from demand growth for Uncrustables sandwiches, which supported the Frozen Handheld and Spreads segment and Away From Home business. U.S. Retail Pet Foods delivered higher profitability despite modest volume pressure.

Fiscal 2026 Results Reveal Both Strengths and Weaknesses

Although investors focused on the strong fourth quarter, the full-year results reveal a more mixed performance.

Fiscal 2026 net sales increased 4% to $9.1 billion, while adjusted sales excluding divestitures and foreign currency effects increased 5%.

However, profitability weakened considerably during the year.

Gross profit declined 10% to $3.04 billion, while gross margin fell sharply from 38.8% to 33.5%. On a GAAP basis, operating income totaled just $360.2 million, while interest expense reached $381.2 million. As a result, the company reported a net loss of $138.7 million, or a loss of $1.30 per diluted share.

Adjusted net income was $977.8 million, and adjusted earnings per share reached $9.15. Even so, adjusted EPS declined 10% from the prior year.

Cash Flow Improvement and Debt Reduction

Quarterly operating cash flow increased to $579.2 million from $393.9 million in the prior year, while free cash flow rose to $483.9 million. For fiscal 2026, free cash flow improved to $1.2 billion, compared with $816.6 million in the prior year. Return of cash to shareholders through dividends was $464.7 million for the fiscal year. At the end of the year, cash and cash equivalents totaled $59 million.

The company continued deleveraging efforts, paying down $720 million in debt during fiscal 2026 and ending the year with total net debt of approximately $6.9 billion.

Fiscal 2027 Outlook Signals Earnings Growth Despite Sales Pressure

Management’s fiscal 2027 guidance paints a mixed but encouraging picture. While the company expects net sales to decline 3% to 4%, primarily due to lower net price realization and softer volume/mix, earnings are projected to improve.

Adjusted earnings per share is projected between $9.75 and $10.25, representing growth of 7% to 12% compared with fiscal 2026. Management also expects adjusted gross margin of roughly 38%, supported by pricing discipline, cost controls, and portfolio optimization.

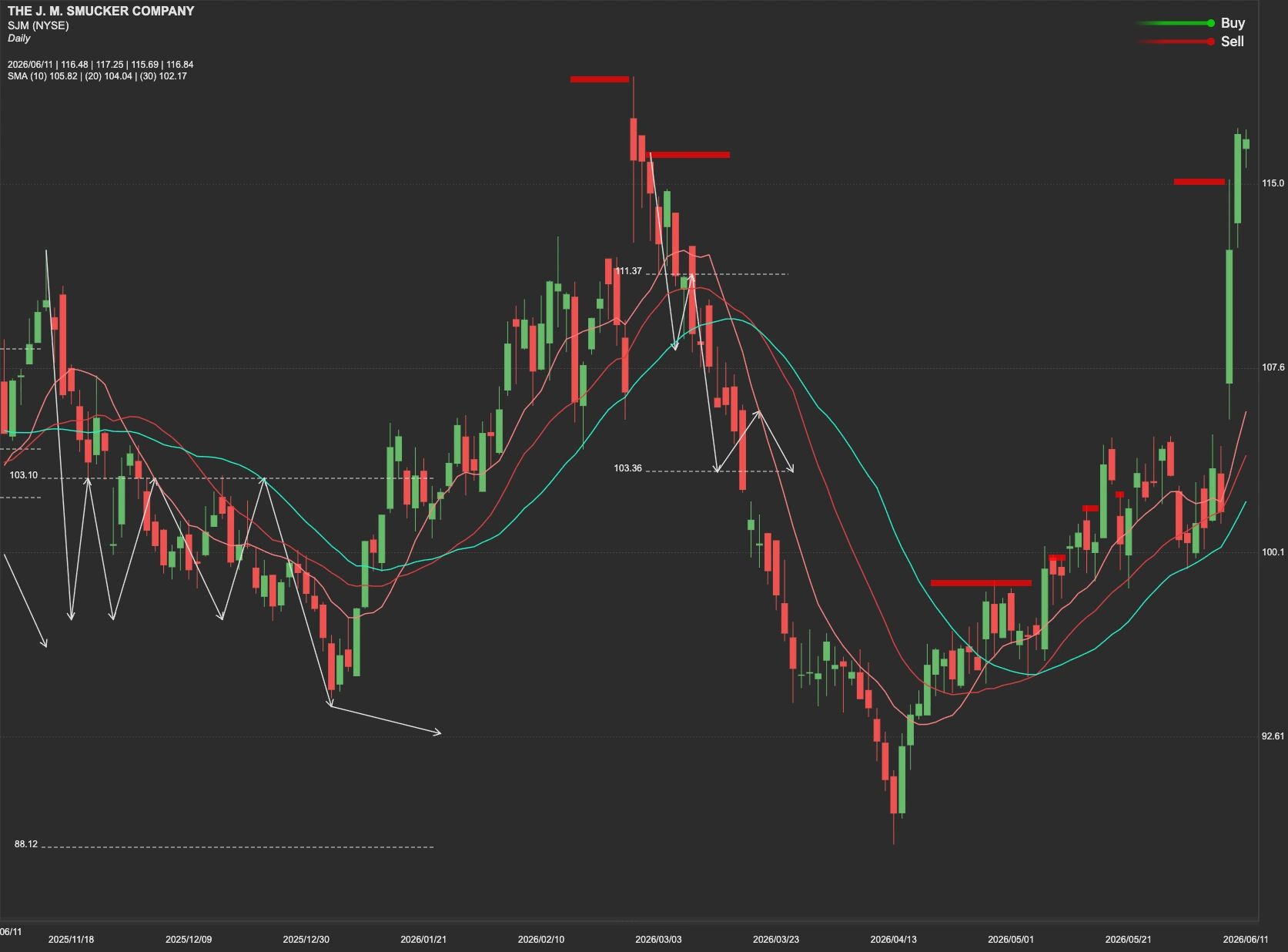

SJM Stock Technical Analysis

From a technical perspective, SJM stock is approaching an important inflection point following the post-earnings rally. Currently the key resistance level stands at $124. A decisive move and sustained close above this level could confirm stronger bullish momentum and potentially pave the way for the next major resistance zone near $148.

However, if the stock fails to establish support above $124, downside pressure may emerge. In that scenario, SJM could revisit support near $103. If selling pressure intensifies, a deeper retracement toward the broader support range between $89 and $81 may come into focus.