Synopsys Delivers Strong Q2 Results as AI-Driven Demand Fuels Growth

Synopsys, Inc. (Nasdaq: SNPS) has delivered a highly consequential second-quarter report for fiscal year 2026. Against a backdrop of explosive demand for artificial intelligence (AI), complex semiconductor design, and structural industry shifts, the silicon-to-systems leader posted quarterly revenue that outpaced prior guidance.

Revenue Surge and Segment Divergence

For the quarter ended April 30, 2026, Synopsys reported revenue of $2.276 billion, comfortably above prior guidance and sharply higher from $1.604 billion in the same period last year. CEO Sassine Ghazi emphasized that AI is expanding semiconductor demand while simultaneously increasing architectural diversity and engineering complexity. As a result, customers are relying more heavily on Synopsys' software, IP, and engineering solutions to accelerate development cycles and manage increasingly sophisticated chip designs.

This growth was primarily driven by the Design Automation segment.

Design Automation: This segment remains the company's powerhouse, accounting for 80.0% of total revenue. It brought in $1.822 billion in Q2 FY2026, a substantial leap from $1.122 billion in the prior year's quarter. Adjusted operating margin in this segment expanded to 43.3%.

Design IP: Contributing 20.0% of total revenue, this segment reported softer trends, with revenue declining to $454.2 million from $482.0 million, and adjusted operating margin compressing to 24.4% from 31.2%.

The GAAP vs. Non-GAAP Disconnect

Despite the robust top-line growth, reported profitability came under pressure due to acquisition-related expenses and restructuring costs. GAAP operating income declined to $120.4 million, down from $376.4 million a year earlier, while operating margin narrowed significantly to 5.3% from 23.5%. Net income also fell sharply to $17.1 million, or $0.09 per diluted share, compared with $349.2 million, or $2.24 per diluted share, in the prior-year quarter.

On a non-GAAP basis, Synopsys demonstrated meaningful margin expansion and disciplined execution. Non-GAAP operating income climbed to $899.7 million from $609.3 million last year, while non-GAAP operating margin improved to 39.5%, up from 38.0%. Non-GAAP net income was $643.7 million, compared to $572.7 million in Q2 FY2025. Non-GAAP earnings per diluted share came in at $3.35, comfortably ahead of guidance, although slightly lower than $3.67 a year ago.

Balance Sheet Strength and Debt Profile

Synopsys generated a healthy operating cash flow of $629 million during the quarter, with capital expenditures of only $54 million (yielding approximately $575 million in free cash flow). The company closed the quarter with cash, cash equivalents and short-term investments of $2.484 billion, and outstanding debt of $10.036 billion.

Raised Full-Year Outlook

Looking ahead, management raised its full-year outlook. Revenue guidance increased to a midpoint of $9.665 billion, up from the prior midpoint of $9.61 billion. The increase reflects stronger core business performance and a favorable accounting impact related to Ansys channel partners, partially offset by the planned divestiture of the Processor IP Solutions business. The company also lifted its full-year non-GAAP EPS guidance to a midpoint of $14.76 while maintaining expectations for GAAP EPS between $2.49 and $2.91, operating cash flow of approximately $2.3 billion, and free cash flow of $2.0 billion.

For the third quarter of fiscal 2026, Synopsys expects revenue in the range of $2.41 billion to $2.46 billion. The company forecasts GAAP EPS of $0.84 to $0.98 and non-GAAP EPS of $3.63 to $3.69, alongside non-GAAP expenses between $1.44 billion and $1.47 billion.

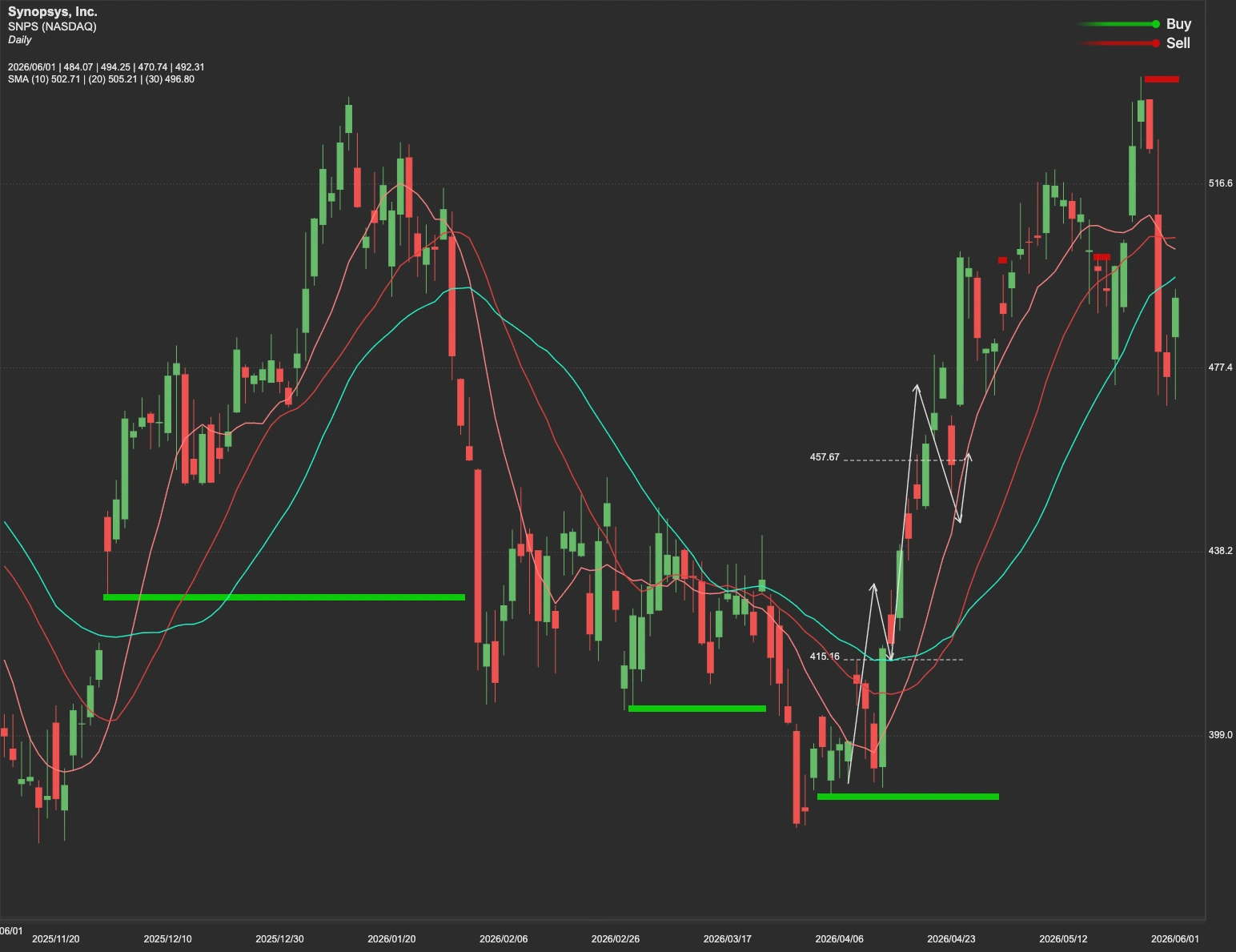

SNPS Stock Technical Analysis

From a technical perspective, $539 remains the critical resistance level for SNPS stock. A decisive breakout and sustained move above this threshold could open the path toward the next upside target near $587. However, failure to hold above resistance may trigger a retracement toward the $454 support zone. If selling pressure intensifies, investors may watch the broader $422–$394 range as a stronger support area.