Tesla Stock Analysis: Margin Strength Meets Heavy Investment

Tesla’s (NASDAQ: TSLA) first-quarter 2026 results present a mixed but strategically coherent picture: solid top-line growth and margin expansion, offset by softer delivery momentum and a sharp increase in capital intensity. For investors, the key question is whether near-term pressure is justified by long-term AI, autonomy, and energy upside.

Revenue Growth and Margin Expansion

Revenue growth remained solid, with total revenue reaching $22.4 billion, up 16% year over year. This expansion was primarily supported by higher vehicle deliveries (358,023 vehicle deliveries for Q1, which was lower than the prior quarter and up 6% from a year earlier), improved average selling prices, and higher automotive ancillary sales. Services and other revenue stood out as a key growth engine, rising 42% year over year, while automotive revenue increased 16%. In contrast, the energy generation and storage segment declined 12%, acting as a partial offset to overall growth. Foreign exchange tailwinds also contributed meaningfully, adding approximately $0.9 billion to revenue.

Gross profit surged 50% year over year to $4.7 billion, with GAAP gross margin expanding to 21.1%, a significant increase of 478 basis points. Operating expenses were $3.8 billion, up 37% compared to $2.8 billion in Q1 2025. Operating income climbed 136% to $0.9 billion, with an operating margin of 4.2%, up 214 basis points year over year. Adjusted EBITDA rose 30% to $3.7 billion, with margin improving to 16.4%. Net income reached $0.5 billion on a GAAP basis and $1.5 billion on a non-GAAP basis, highlighting the growing divergence between reported and adjusted earnings as stock-based compensation and other exclusions remain material.

The underlying drivers of this profitability expansion were multifaceted. Higher vehicle pricing and improved product mix contributed positively, alongside growth in FSD sales and subscriptions. Lower material costs also helped reduce the average cost per vehicle. Additionally, certain one-time benefits related to tariffs and warranties provided a temporary uplift. However, these gains were partially offset by rising operating expenses, particularly in artificial intelligence development, research and development initiatives, and stock-based compensation linked to executive incentives.

Operational Summary

Operationally, in Q1 2026, Tesla produced 408,386 vehicles, up 13% from a year earlier, and delivered 358,023 units, up 6% year over year, both lower than the prior quarter, with Model 3 and Model Y continuing to dominate the product mix. Energy storage deployments declined 15% year-over-year and 38% quarter-over-quarter to 8.8 GWh.

Cash Flow and Balance Sheet

Cash generation remained healthy in the quarter, with operating cash flow reaching $3.9 billion and free cash flow totaling $1.4 billion. Tesla ended the quarter with $44.7 billion in cash, cash equivalents and short-term investments, reflecting a sequential increase of $0.7 billion. This improvement was supported not only by free cash flow but also by $1.2 billion in financing inflows, although partially offset by a $2.0 billion equity investment in SpaceX.

The company’s capital allocation strategy is becoming increasingly aggressive. Capital expenditures surged 67% year over year to $2.49 billion, and management has guided to more than $25 billion in total capex for 2026. This level of investment reflects Tesla’s ambition to scale its AI infrastructure, expand battery and materials production, and build out capabilities in robotics and semiconductor manufacturing.

Strategic Direction: AI + Robotaxi Pivot

Tesla is clearly evolving from a pure EV manufacturer into a platform company centered on AI, autonomy, and energy ecosystems. Key developments:

-

Launch of unsupervised Robotaxi rides in Dallas and Houston in April

-

In Q1, paid Robotaxi miles nearly doubled sequentially

-

Expansion of FSD (Supervised) globally (e.g., Netherlands approval)

-

Began ramping lithium, cathode and LFP production

-

Preparation for Cybercab, Tesla Semi, and Megapack 3 production

-

Early-stage scaling of Optimus humanoid robots

-

Cortex 2 is now online and has started running training workloads; custom silicon development with Dojo 3 is in an effort to reduce the cost of training over time

-

In a landmark partnership with SpaceX, Tesla is building a "Research Fab" at Giga Texas to manufacture next-generation AI5 inference processors, aiming to build the largest chip fab ever conceived

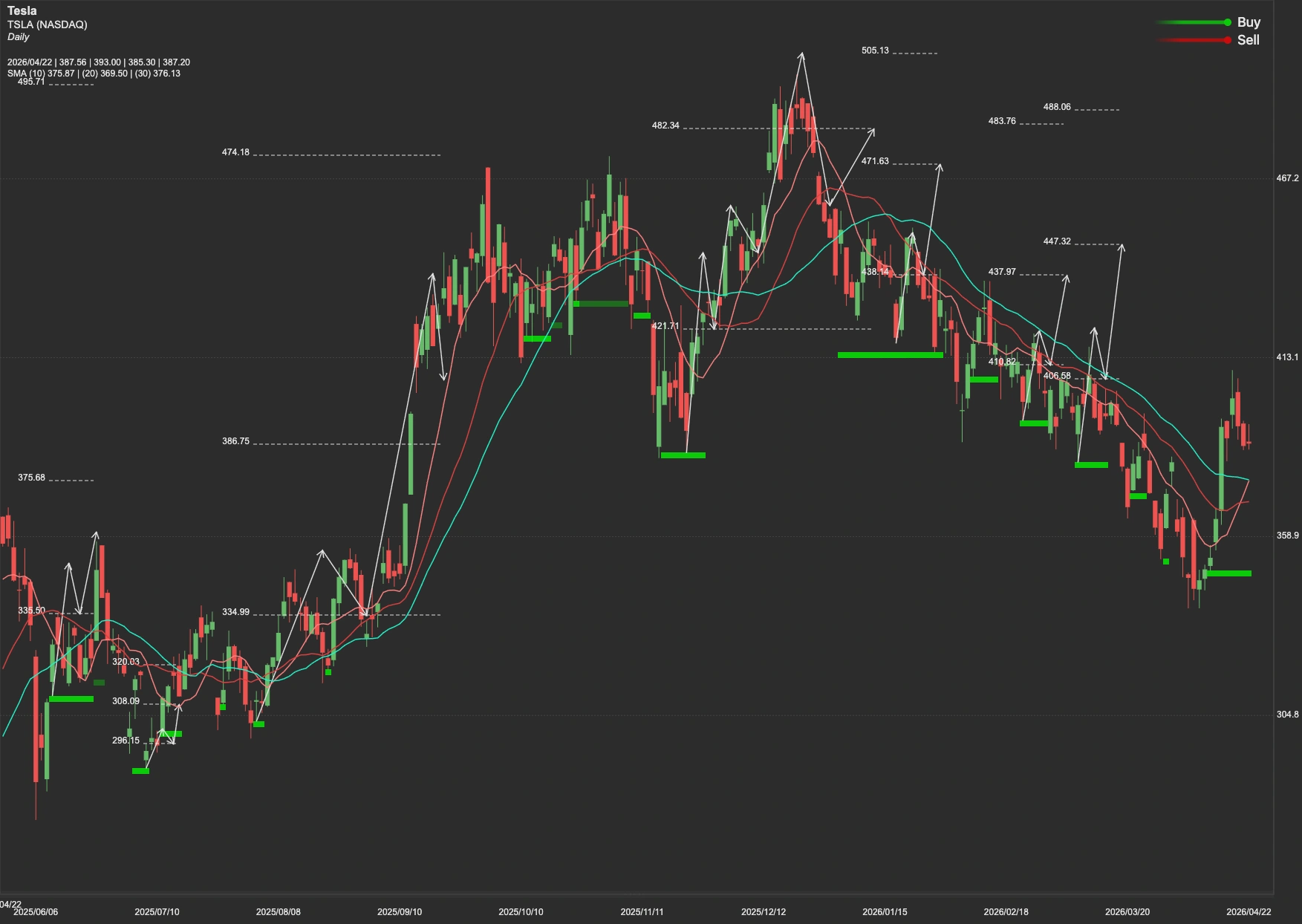

Technical Outlook

TSLA's technical trajectory is currently caught between the "bright future" of its mission and the near-term capital intensity of its transition. Management identified affordability and utility as key competitive advantages—positioning Tesla to gain share in 2026 as gas-powered alternatives suffer from energy supply chain fragility.

Currently, TSLA stock is facing a key resistance level at $419. A sustained breakout above this level would likely confirm bullish momentum, opening the path toward $458 as the next upside target. Conversely, failure to break above this threshold could result in a pullback toward the $350 support level, with a deeper downside scenario potentially testing $317-$298.