Vail Resorts Faces Weather-Driven Headwinds, but Long-Term Growth Story Remains Intact

Shares of Vail Resorts (NYSE: MTN) remain under pressure after the company reported weaker third-quarter fiscal 2026 results, as one of the most challenging winter seasons in recent history weighed heavily on visitation across its key mountain destinations.

Q3 FY26 Financial Performance

For the third quarter ended April 30, 2026, Vail Resorts reported resort net revenue of $1.205 billion, down 7.0% year-over-year, as unfavorable weather conditions weighed heavily on visitation and spending from both local and destination guests, particularly at the Rockies and Tahoe resorts. Despite visitation declining 15%, total lift revenue fell only 5%, primarily as a result of 2025/2026 North American Pass Sales increasing 3% heading into the season.

Profitability also softened during the quarter. Income from operations declined to $494.1 million from $577.8 million a year earlier, while resort reported EBITDA fell 9.5% to $586.4 million. Net income attributable to the company decreased to $314.4 million, compared with $389.7 million in the prior-year quarter, translating to diluted earnings per share of $8.81 versus $10.46 a year ago.

Strong Balance Sheet Supports Continued Investment

Despite a difficult operating environment, Vail Resorts maintains a solid liquidity position. At the end of the quarter, the company held approximately $1.1 billion of total liquidity, including $371.4 million in cash and cash equivalents.

Total debt stood at $3.02 billion, resulting in net debt of approximately $2.65 billion.

The company also reaffirmed its commitment to shareholder returns, declaring a quarterly dividend of $2.22 per share payable on July 9, 2026. Additionally, Vail plans to invest between $234 million and $239 million during calendar year 2026.

Early Pass Sales Show Mixed Signals

Through May 26, 2026, pass product units sold for the upcoming 2026/2027 North American ski season declined approximately 10%, while sales dollars fell about 5% compared with the same period last year. The decline in performance-to-date reflects softer demand following one of the worst snowfall years in history in the western U.S.

However, there were encouraging signs beneath the headline numbers. The company's new Young Adult pass products are outperforming other age groups, while Unlimited pass products continue to demonstrate stronger demand than frequency-based offerings.

CEO Rob Katz also emphasized that historical U.S. ski market data indicates that visitation typically fully recovers following a season with poor conditions if the subsequent season has normal conditions. As a result, management believes there remains potential for stronger pass sales later in the year and a recovery in lift ticket demand during the 2026-27 season.

Meanwhile, Epic Australia Pass sales continue to perform strongly, with units sold increasing 26% and sales dollars rising 31% compared with the prior year.

Guidance Cut Reflects Difficult Winter Conditions

Due to the historically challenging weather conditions in the western U.S. that persisted through the third quarter, which negatively impacted demand, the company lowered its full-year fiscal 2026 outlook.

The company now expects fiscal 2026 net income attributable to Vail Resorts between $128 million and $162 million, while resort reported EBITDA is projected to range from $735 million to $755 million.

Management highlighted continued progress in guest experience initiatives, technology investments, operational improvements, and cost-efficiency programs. The company's resource efficiency transformation plan is expected to generate $106 million in annualized cost efficiencies, representing a $6 million increase above the original two-year plan.

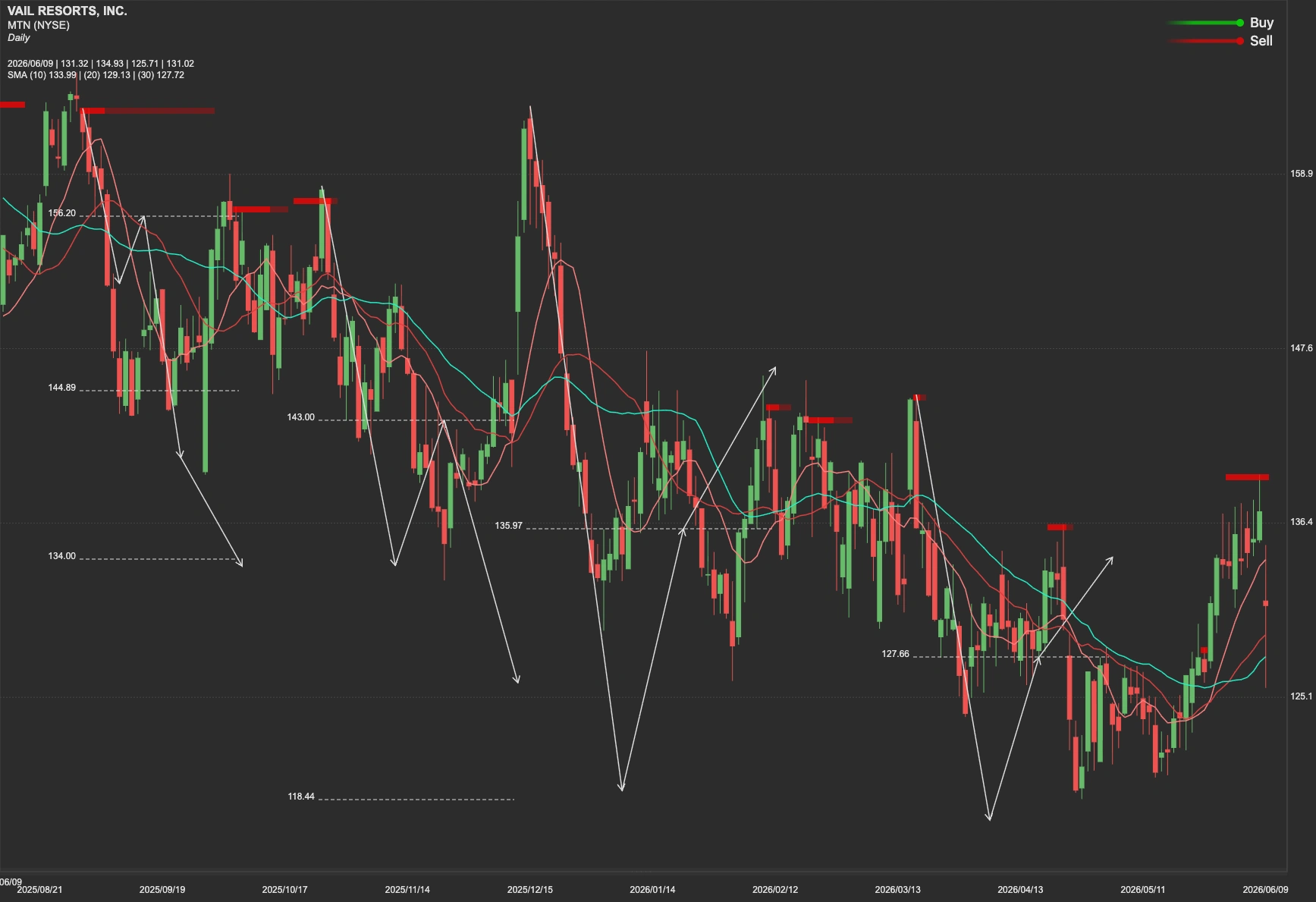

MTN Stock Technical Analysis

From a technical perspective, MTN stock faces an important near-term test around the $156 resistance level. A decisive move above that threshold could strengthen bullish momentum and open the path toward the next key resistance area near $183. Over the longer term, the stock continues to face a major resistance zone around $223.