Walmart Stock Slides After Earnings Despite Strong Revenue and eCommerce Growth

Walmart Inc. (NASDAQ: WMT) published its first-quarter financial results for fiscal year 2027, delivering a stellar performance that highlighted top-line momentum, digital expansion, and solid gains in its high-margin advertising segments. Despite these robust fundamental achievements, WMT shares tumbled by 7.3% following the announcement.

Strong Revenue Growth Highlights Walmart’s Resilience

Walmart reported first-quarter total revenue of $177.8 billion, representing a 7.3% increase year over year; excluding currency fluctuations, revenue growth came in at 5.9%. Net sales rose 7.1% to $175.7 billion, while membership and other income climbed 27.0% to $2.1 billion.

One of the strongest areas of performance remained eCommerce, where global sales surged 26%, driven by store-fulfilled pickup and delivery services as well as continued marketplace expansion. The company’s advertising business remained another major growth engine. Global advertising business jumped 37%, while Walmart U.S. advertising rose 36%. Membership fee revenue also increased 17.4% globally.

Another two of America's largest retailers, Home Depot and Target, also reported their quarterly earnings this week. More information to visit: Home Depot Holds Guidance Steady as Sales Rise, But Margins Face Pressure and Target Reports Strong Q1 Performance with Upgraded Full-Year Outlook.

Profitability Pressured by Higher Costs

On the profitability front, gross profit rose 7.4% to $42.6 billion, expanding gross profit as percentage of net sales by 6 bps to 24.26%. However, operating expenses on a reported basis deleveraged by 33 bps, primarily due to elevated depreciation expense tied to capital investments and inflating healthcare enrollment costs for U.S. associates. Operating income grew 5.0% to $7.5 billion, reflecting strong sales growth, higher gross margins including business mix benefits, global membership growth and other income benefits from miscellaneous items; partially offset by higher fuel costs and expense deleverage. Operating income as percentage of net sales declined to 4.27% from 4.35% in Q1 FY26.

Diluted earnings per share increased 19.6% year over year to $0.67, while adjusted EPS came in at $0.66, up 8.2%, excluding the impact, net of tax, from a net gain of $0.02 on equity and other investments and $0.01 from business reorganization charges.

Despite these cost pressures, management emphasized disciplined execution through automation, technology investments, and higher-margin business segments.

“Our results reflect our continued focus on delivering across the enterprise—better shopping experiences, a broader assortment, and faster delivery,” Walmart President and CEO John Furner said.

Segment Performance

Operationally, Walmart continued to show momentum across all major business units. Walmart U.S. comparable sales without fuel grew 4.1%, with transaction growth accelerating alongside stronger grocery demand. Sam’s Club U.S. delivered solid performance through higher transaction counts and growing membership revenue, while Walmart International benefited from broad-based sales strength and expanding digital penetration across global markets

Walmart’s Balance Sheet Remains Stable

Walmart ended the quarter with $10.7 billion in cash and cash equivalents and total debt of $58.1 billion.

The company generated $4.7 billion in operating cash flow, though free cash flow turned negative at $1.9 billion due to increased capital expenditures supporting Walmart’s omnichannel expansion strategy. Inventory was $62.6 billion, an increase of $5.1 billion, or 8.9% year over year, affected by the timing of receipts, strong unit demand in grocery for Walmart U.S., and fuel.

Shareholder returns remained a priority, as Walmart repurchased $2.1 billion worth of stock and paid $2.0 billion in dividends during the quarter. The company still has $28.2 billion remaining under its repurchase authorization

Outlook For Fiscal 2027 Remains Unchanged

For full-year FY27, the company maintained its prior full-year guidance, anticipating net sales growth of 3.5% to 4.5% in constant currency and adjusted EPS of $2.75 to $2.85.

Walmart also expects second-quarter net sales growth of 4% to 5% in constant currency, with adjusted operating income projected to rise between 7% and 10%. Adjusted EPS guidance for the quarter was set at $0.72 to $0.74.

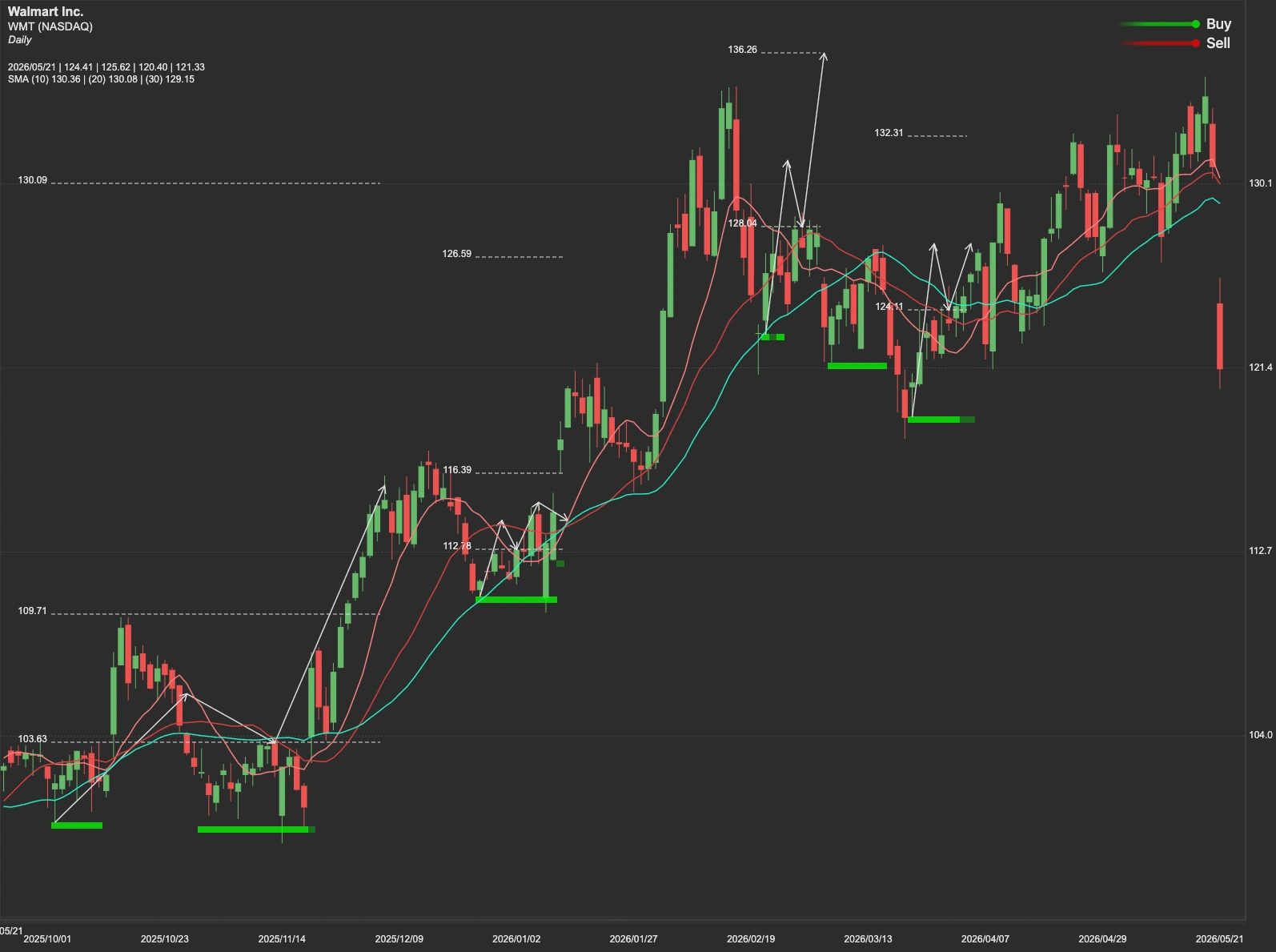

WMT Stock Technical Analysis

The immediate resistance level stands near $135. A sustained move above this threshold could restore bullish momentum and potentially open the path toward the next upside target at $144.

However, if WMT fails to reclaim and hold above $135, downside pressure may continue. In that scenario, traders may watch for support near $111, while a deeper correction could bring the stock toward a secondary support zone around $97.