Wells Fargo Sees Economic Resilience and Sustained Growth Momentum Amid Market Volatility

Wells Fargo (NYSE: WFC) delivered a solid start to 2026, with first-quarter results reflecting steady balance sheet growth, improved operating leverage, and continued capital returns, even as margin pressure and higher credit provisioning remain areas to monitor.

Earnings Momentum Builds on Broad-Based Growth

The bank reported net income of $5.3 billion, translating to $1.60 per diluted share, up 15% year over year. A modest $135 million tax benefit contributed $0.04 per share to earnings, but underlying performance remained strong even excluding this item. Revenue climbed 6% year over year to $21.4 billion, supported by balanced growth across both net interest income and noninterest income. This performance reflects a bank that is benefiting from prior strategic investments while maintaining cost discipline. Despite a modest 3% rise in noninterest expenses, operating leverage improved, reinforcing profitability gains.

Balance Sheet and Capital

The balance sheet tells a compelling story of expansion. Average loans increased 10% year-over-year to $996 billion, while deposits grew 6% to $1.4 trillion. Growth was particularly strong in Corporate and Investment Banking, where loans surged 23%, alongside continued momentum in Wealth and Investment Management, which saw client assets rise 11% to $2.2 trillion. This broad-based expansion suggests that both consumer and institutional demand remain resilient despite a more volatile macro environment.

Return on equity (ROE) improved to 12.2%, while return on average tangible common equity (ROTCE) rose to 14.5%. However, efficiency ratio declined from 69% to 67%.

Credit quality remains stable but is trending slightly higher in absolute terms. Provision for credit losses increased 22% to $1.1 billion, primarily reflecting higher commercial and industrial and auto loan balances. Net charge-offs held steady at 0.45% of average loans.

Capital returns remain robust. The company repurchased $4.0 billion of stock during the quarter and returned a total of $5.4 billion to shareholders while maintaining a Common Equity Tier 1 (CET1) ratio of 10.3%. Although this is down from 11.1% a year ago.

Segment Performance Highlights a Diversified Engine

Segment performance was broadly constructive. Consumer Banking and Lending posted a 7% revenue increase, driven by stronger deposit and loan balances, alongside improved fee income. Commercial Banking also delivered 7% growth, with a notable 28% increase in net income supported by higher noninterest income and lower expenses. Corporate and Investment Banking saw mixed results, with strong Markets revenue offset by weaker commercial real estate activity, leading to a slight decline in net income. Wealth and Investment Management stood out with 14% revenue growth and a 34% increase in net income, supported by higher deposit and loan balances and asset-based fees. Corporate segment reported revenue of negative $232 million, primarily driven by lower net interest income and lower lease income related to the sale of the railcar leasing business.

Outlook: Stability with External Uncertainty

From a strategic standpoint, management highlighted continued momentum across credit cards, auto lending, investment banking, and wealth management. Client engagement trends and pipeline strength suggest ongoing business expansion, even as macro uncertainty and commodity-driven inflation risks—particularly from higher oil prices—linger in the background. Management reaffirmed its 2026 net interest income guidance of around $50 billion and expects noninterest expense to be approximately $55.7 billion.

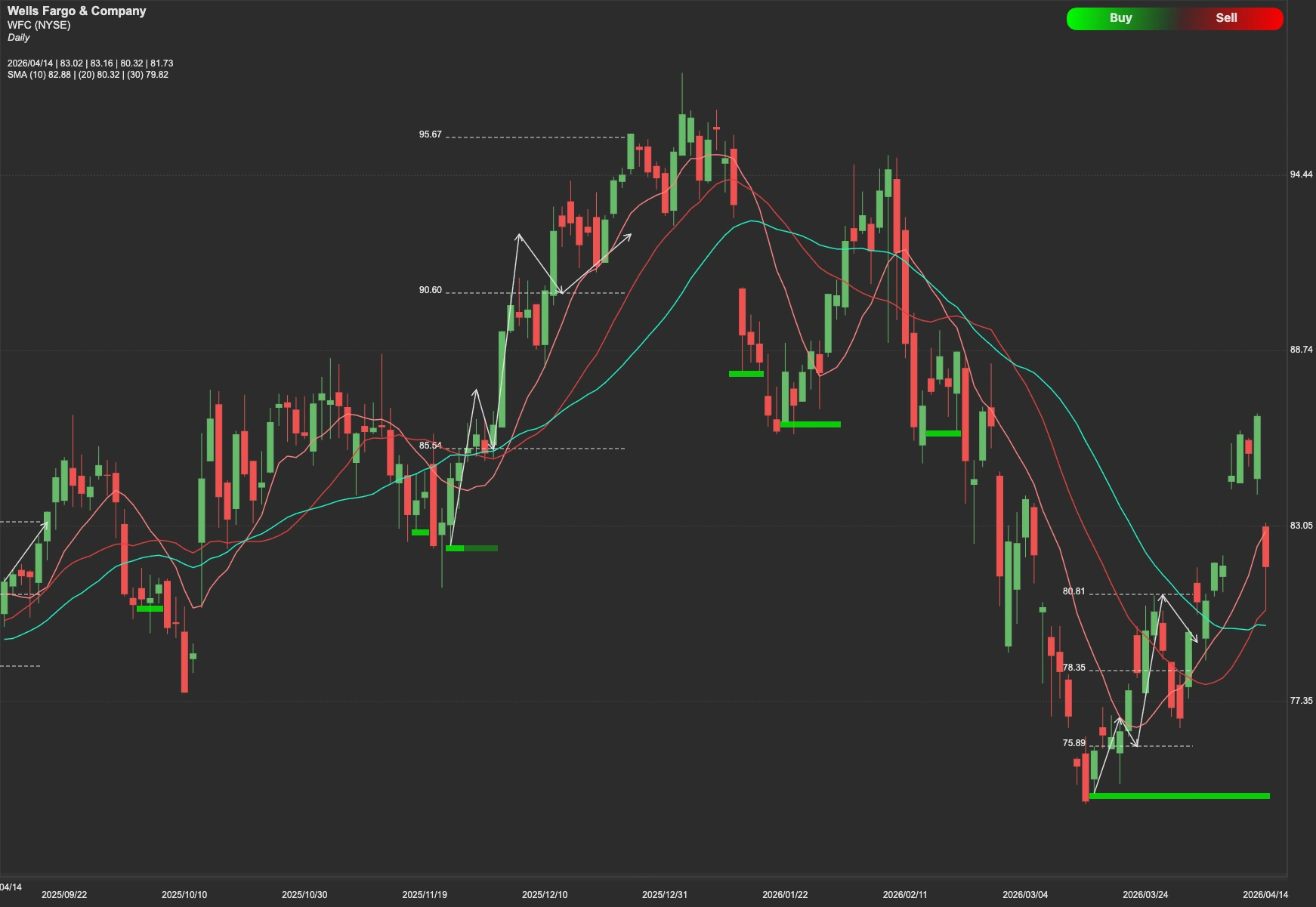

Technical Analysis

From a technical perspective, the stock is currently testing a major resistance level at $93. Should WFC manage a clean breakout and close decisively above $93, the technical path clears significantly. The next psychological and structural goal for the bulls is the $100 mark. Given the $4 billion in share repurchases this quarter and the bank's significant excess capital, the internal buying pressure remains high.

Conversely, if the $93 resistance proves too formidable for the current market volume, we may see a period of consolidation or a retracement. Traders should look for initial support at $73. In a broader market correction or a shift in the economic outlook (such as the "impact of higher oil prices" noted by Scharf), a deeper support level sits at $66.