Wells Fargo Stock Analysis: Asset Cap Removal Fuels Growth Momentum

Wells Fargo & Company (NYSE:WFC) closed out 2025 with a solid fourth-quarter performance, underscored by improving profitability, disciplined cost control, and renewed growth momentum following the removal of the Federal Reserve’s long-standing asset cap.

Fundamental Strength

For the fourth quarter of 2025, Wells Fargo reported net income of $5.4 billion, or $1.62 per diluted share, up from $1.43 a year earlier. Excluding a $612 million severance-related notable item, adjusted earnings rose to $1.76 per share, highlighting the bank’s underlying earnings power. Total revenue increased 4% year over year to $21.3 billion, driven by higher net interest income and solid fee growth across wealth and investment management and card businesses. Net interest income climbed 4%, supported by loan growth, and noninterest income increased 5%. The Provision for Credit Losses was $1.04 billion, included a slight increase in the allowance reflecting higher commercial and industrial, auto, and credit card loan balances, largely offset by a lower allowance for commercial real estate loans. Net charge-offs decreased 13% year-over-year to $1.03 billion, net loan charge-offs as a % of average total loans (annualized) was 0.43%.

For the year ended December 31, 2025, Wells Fargo reported net income of $21.3 billion, up from $19.7 billion in 2024, representing an increase of approximately 8% year over year. Diluted earnings per share rose 16.5% to $6.26. Total revenue increased 2% to $83.7 billion, supported primarily by stronger noninterest income, which grew 4.6% to $36.2 billion. Net interest income edged down slightly to $47.5 billion, compared with $47.7 billion in 2024. The bank achieved its 15% ROTCE target for 2025 and has set a new medium-term goal of 17–18%.

Efficiency and Capital Strength

Wells Fargo’s efficiency ratio improved to 64% in the quarter, down from 68% a year ago, reflecting the payoff from multi-year expense discipline. Management highlighted that Wells Fargo has successfully balanced short-term performance with long-term investment. Over the past five years, the bank achieved $15 billion in gross expense reductions, allowing it to fund increased investments in infrastructure and business growth while still reducing its total expense base.

Capital returns remained robust. In the fourth quarter alone, Wells Fargo repurchased $5.0 billion of common stock, bringing full-year shareholder returns to $23 billion, including a 13% dividend increase. Maintained a strong Common Equity Tier 1 (CET1) ratio of 10.6% in Q4.

Segment Breakdown in Q4

Consumer Banking and Lending (CBL): Revenue rose 7% to $9.6 billion. While Home Lending struggled (down 6%), Credit Card revenue grew 7% on higher loan balances and higher card fees.

Commercial Banking (CB): Experienced a 3% revenue decline to $3.1 billion, largely due to the impact of lower interest rates and a $8 billion loan and $6 billion deposit transfer to the Consumer segment.

Corporate & Investment Banking (CIB): Remained stable at $4.6 billion. A 7% jump in Markets revenue (equities, commodities, and structured products) offset a 4% decline in Investment Banking revenue and a 3% decline in Commercial Real Estate.

Wealth & Investment Management (WIM): A standout performer with revenue up 10% to $4.4 billion, fueled by a 16% surge in net interest income and a 9% growth on higher asset-based fees.

Outlook: Positioned for 2026 With Fewer Constraints

With the asset cap lifted and consent orders terminated, Wells Fargo enters 2026 with greater strategic flexibility and the ability to grow its balance sheet more freely. Management expressed confidence that the bank is now competing on a more level playing field and can allocate additional resources toward growth initiatives across its core businesses.

Management guided 2026 net interest income (excluding Markets) to around $48 billion, supported by mid-single-digit loan and deposit growth, continued fixed asset repricing, and expectations for two to three Fed rate cuts.

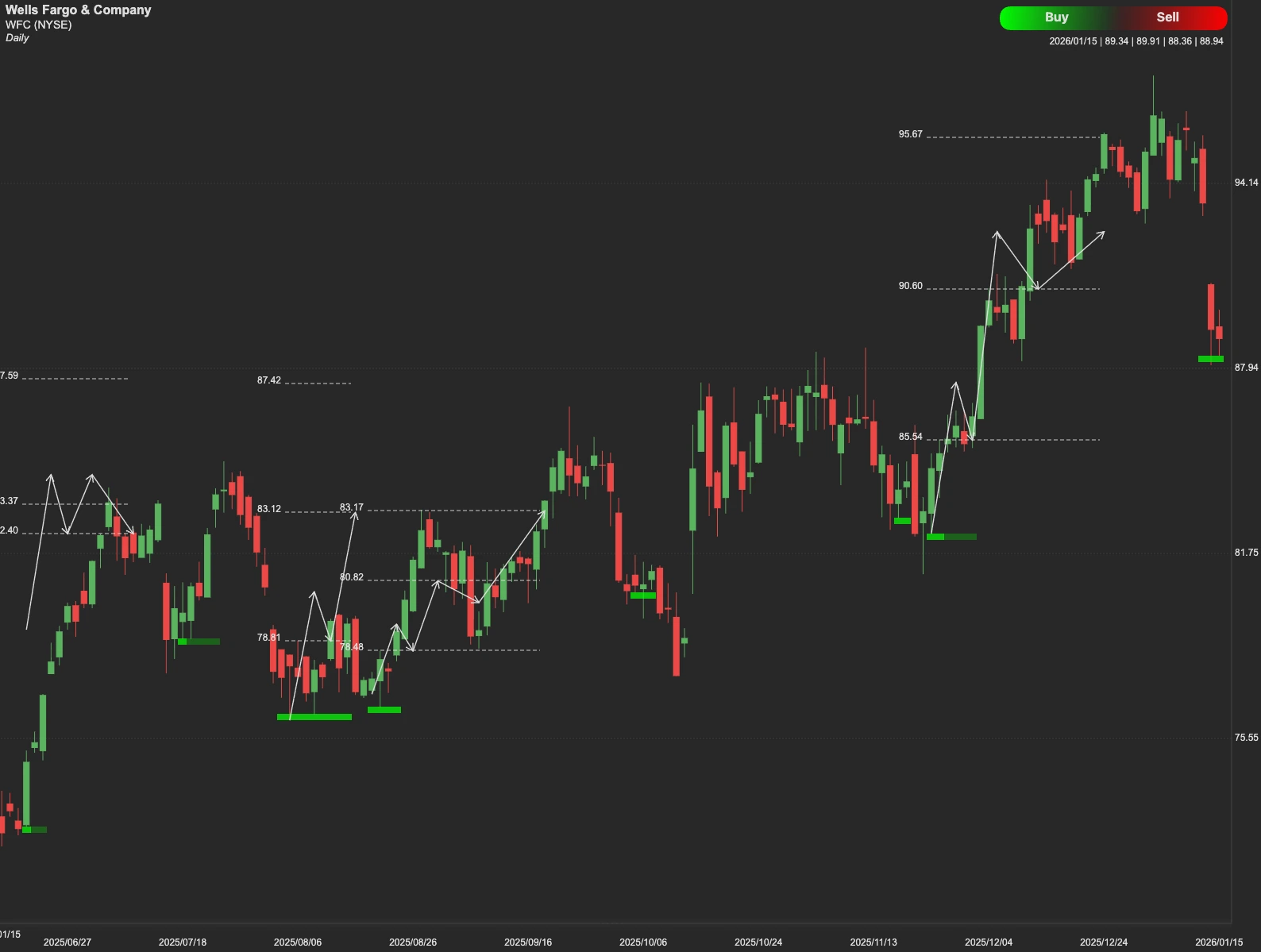

Technical Outlook

From a technical perspective, $98 is the key resistance level for WFC shares. If WFC holds above $98, it would confirm a breakout, opening the door toward the $110 target.

Failure to sustain above $98 could trigger a pullback toward initial support at $80. A deeper correction may see the stock test the $74–$70 support zone.